Can the World Economic Forum be any less useful or relevant?

Most people in business and politics have heard of the World Economic Forum (WEF), best known for holding its annual meeting for the world’s glitterati every January in Davos, Switzerland.

Beyond that international confab, WEF provides a set of “Transformation Maps” on its website which are described as “a constantly refreshed repository of knowledge about global issues, from climate change to the future of work.”

“Transformation Maps are the World Economic Forum’s dynamic knowledge tool,” the website declares. “They help users to explore and make sense of the complex and interlinked forces that are transforming economies, industries and global issues.”

The maps present insights written by so-called experts along with machine-curated content. Together, “the information allows users to visualise and understand more than 250 topics and the connections and inter-dependencies between them, helping in turn to support more informed decision-making by leaders.”

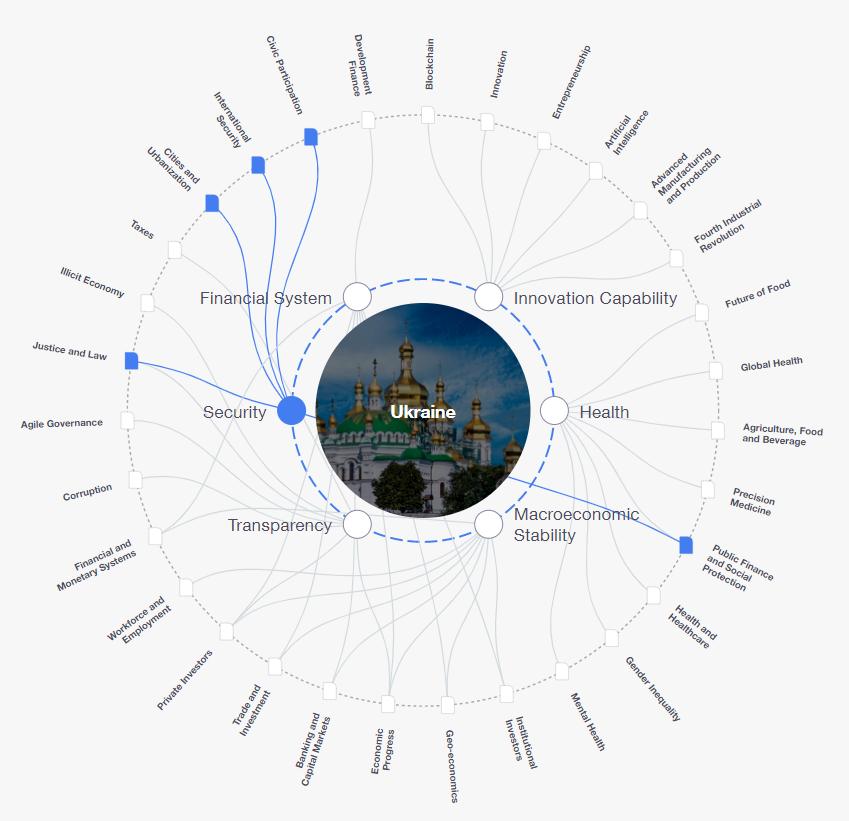

That page displays 293 different topics. Scrolling down a good ways finally brings up “Ukraine” … and here’s what is displayed after clicking on the “Security” issue:

Explaining how the chart was developed, the website reports:

“This Transformation Map explores key issues for Ukraine based on its rankings in the most recent edition of the World Economic forum’s Global Competitiveness Index.”

For the record, those six “key issues” are Financial System, Innovation Capability, Health, Macroeconomic Stability, Transparency and Security.

The Security issue then links to five other topics (Public Finance and Social Protection, Justice and Law, Cities and Urbanization, International Security and Civic Participation).

Curious to see what content would be displayed, I clicked the International Security topic, which causes the International Security Transformation Map to appear. Only then did I finally learn that:

“The return of great power competition has been accompanied by the outbreak in Ukraine of Europe’s largest ground war since World War II.”

I must admit that I am quite impressed with how these Transformation Maps have helped me to visualize and understand the connections and inter-dependencies between Ukraine and International Security … and it is now completely clear to me how these tools support more informed decision-making by leaders. [Feel free to insert snark emoji here.]

Millions of Americans age 20 to 24 fall into the NEET category: “Not in Employment, Education or Training.”

The COVID-19 pandemic has exposed some interesting fault-lines in the socio-economic fabric of the United States. One of these relates to young adults — those between the ages of 20 and 25. What we find paints a potentially disturbing picture of an economic and employment situation that may not be easily fixable.

A recently issued economic report published by the Center for Economic and Policy Research (CEPR) focuses on the so-called “NEET rate“– young Americans who are not employed, not in school, and not in training.

As of the First Quarter of 2021, the NEET category represented nearly 4 million Americans between the ages of 20 and 24. This eye-popping statistic goes well beyond the particular circumstances of the pandemic and may turn out to be an economically devastating trend with a myriad of adverse ripple effects related to it.

Look at any business newspaper or website these days and you’ll see reports regularly about worker shortages across many sectors — including unfilled jobs at the lower end of the pay scale which offer employment opportunities that fit well with the capabilities of lower skilled workers newly coming into the workplace.

At this moment, pretty much anyone who is willing to look around can easily find employment, schooling, or training of various kinds. But for millions of Americans in the 20-24 age cohort, the job opportunities appear to be falling on deaf ears. Bloomberg/Quint‘s reaction to the CEPT study certainly hits home:

“Inactive youth is a worrying sign for the future of the [U.S.] economy, as they don’t gain critical job skills to help realize their future earnings potential. Further, high NEET rates may foster environments that are fertile for social unrest.”

… Daily urban strife in Portland, Minneapolis and Seattle, anyone?

It doesn’t much help that younger Americans appear to be less enamored with the basic economic foundations of the country than are their older compatriots. A recent poll by Axios/Momentive has found that while nearly 60% of Americans hold positive views of capitalism, those sentiments are share by a only little more than 40% of those in the 18-24 age category.

Moreover, more than 50% of the younger group view socialism positively compared to only around 40% of all Americans that feel the same way.

The coronavirus pandemic may have laid bare these trends, but it would be foolish to think that the issues weren’t percolating well before the first U.S. businesses began to lock down in March 2020.

And more fundamentally, one could question just how much government can do to reverse the trend; perhaps the best thing to do is to stop “helping” so much … ?

More information about the CEPR report can be viewed here. What are your thoughts on this issue? Please share your views with other readers here.

Responses from two people in particular are worth highlighting for the “countervailing views” that they espouse. I think both have merit.

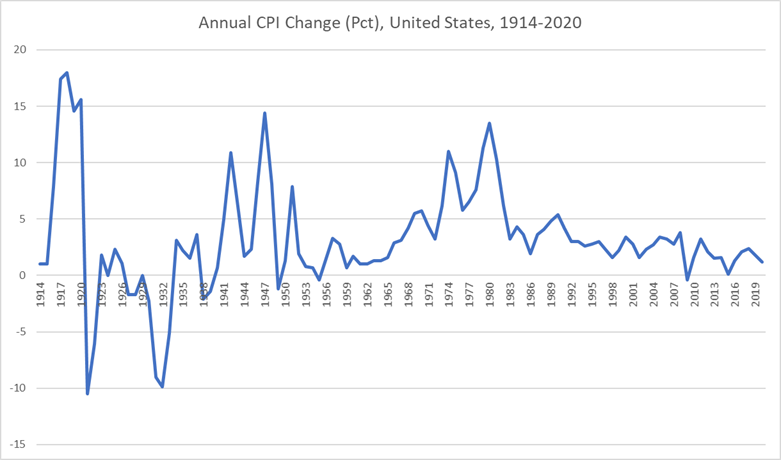

The first response came from my brother, Nelson Nones, who has lived and worked outside the United States for decades. His perspectives are interesting because, while fully understanding domestic events and policies, he also brings an international orientation to the discussion due to his own personal circumstances. Nelson is looking to history for his perspectives on the inflation issue, offering these comments:

The chart below shows annual U.S. CPI percentage change for the past 106 years:

Projecting the latest (April 2021) Consumer Price Index forward to an entire year suggests that the U.S. will experience a 3.1% inflation rate in 2021. That would be higher than in any year since 2011, which was a bounce-back year following the Great Recession. Otherwise, the generic inflation trend has been consistently down since 1982 (nearly 40 years).

If the historical trends are any guide, and if we are indeed entering a persistent inflationary phase, it would take another decade before inflation growth approaches the levels seen during the 1970s.

But I think the likeliest scenario is experiencing a sharp uptick this year due to pent-up demand following the COVID-19 pandemic that will causie spot shortages, followed by resumption of a downward trend over the following ten years or so.

That’s similar to the pattern you can observe in the chart [above] during the years following the end of World War II, which had also created massive pent-up consumer demand.

Consider that the coronavirus pandemic hasn’t really altered the underlying economic fundamentals. The past 40 years has witnessed an explosion of manufacturing capacity in China and other developing countries, and that hasn’t gone away. Meanwhile, dependency on oil — a key driver of inflation in the 1970s — has shrunk due to improved energy efficiency and aggressive exploitation of renewable energy resources, which for all practical purposes are in infinite supply.

Another factor, which doesn’t get as much attention as it probably should, is declining birth rates and aging of the population on a global scale, leading to a slower rate of population growth in the future that may constrain demand for consumer products in comparison to the past century. Let’s face it — we old farts just don’t consume as much as growing families do!

So yes, we should keep an eye on inflation — but I don’t think we’re in for a repeat performance of the horrible 1970s.

Echoing Nelson’s thoughts are the perspectives of another business veteran — an editor and publisher who has been intimately involved in the commercial/B-to-B field for decades. Here is what he wrote to me:

I don’t want to get into a public debate with the inflationistas because I will never convince them that this is likely not a replay of the 1970s and early 80s inflationary period pre-[Paul] Volcker. (Speaking personally, I didn’t own a house until I was 42 for the very reasons you cited in your blog post, and I was just a lowly editor back then.)

What we’re seeing today is simply the price shock of suddenly soaring demand, aggravated in the case of some commodities such as steel by Trump-era tariffs.

All commodities are tied to the price of crude oil, the most volatile of all commodities, which is long-denominated in U.S. dollars. WTI crude pricing is now at around $63 per bbl. — about where it was in early 2020 before the pandemic hit. It went negative for a time during the worst period of the crash in worldwide demand that was brought about by the pandemic. Tanks couldn’t be found into which to put the excess crude coming out of the ground from U.S. fracking. Traders freaked out, as they sometimes do.

So naturally, the percentage changes today look jaw-dropping. I can go through all the other commodities mentioned in your post and provide simple explanations as to why each is currently on the rise. Logistical bottlenecks are a big problem with everything — but as with oil, most of the issue is the sudden surge in demand as the pandemic winds down even as production and logistics aren’t yet prepared to fulfill the need.

In other words, the situation has very little to do with government spending — especially since most of the infrastructure money isn’t even allocated, let alone spent. Also, the Biden administration has yet to raise a single tax. It can’t. Only the House Ways and Means Committee can initiate tax changes, and those must then go through the Senate to become law. Senate Minority Leader McConnell and his allies have made sure nothing has gotten through.

Of course, it never hurts to keep an eye on things — especially with structural inflation as you noted in your article. But it’s important to look also at other, broader data. The Producer Price Index in April did reflect the increase in commodities prices, but the Consumer Price Index, even though it had a month of robust increases, remains below 3% annualized. And the Personal Consumption Expenditure Price Index, which is what the Fed pays attention to the most, is still tracking under 2% on an annualized basis. (A little inflation can be a good thing, actually.)

On the income side, average wage rates aren’t rising; they’re more likely to be falling in the future as low-wage service workers, including those in foodservice, re-enter the market.

So in my view the things people see with inflation are most likely short-term issues. Let’s look at it again in six months to a year. I’d also suggest that people read economist Paul Krugman’s columns in the New York Times for a bit of perspective that’s counter to the views of the inflationistas, if only for balance. The monetarists have been wrong since Volcker squeezed out the inflationary spiral. It was painful, though — so we’ll want to keep an eye on things.

Considering the views put forward above, I think it’s fair to conclude that “the jury’s out” on whether we’re actually entering a prolonged inflationary period. If you have additional thoughts or perspectives to share on either side of the issue, I’m sure other readers would be interested to hear them. Feel free to leave a comment below.

The rise in lumber prices has received a certain degree of coverage in the news in recent weeks and months. For anyone who used the “pandemic period” to engage in home remodeling or renovation projects – perhaps moving away from “open concept everything” to reintroduce the designated spaces of yesteryear – the eye-popping price of lumber has come as something of a shock.

As for explaining the sharp increase, it’s logical to think that prices are directly correlated to the increased demand for the product. But this explanation is incomplete; the steep price rise in a wide range of commodities well beyond just lumber tells us that inflation isn’t relegated to just a few high-demand product categories. It’s the closest thing to “across the board” that we’ve seen in over 40 years — and the issue seemed to come out of nowhere.

Price inflation has been such a non-factor for so many decades, most consumers don’t even have personal memories of it. But those of us “of a certain age” remember well how difficult it was to navigate an “inflation-everywhere” environment where annual salary increases could never keep pace with rising prices.

It was difficult on people with fixed incomes, of course, but perhaps worse for young consumers who found that struggling to save for a down payment on a house purchase was a losing proposition as the gap widened rather than narrowed year over year. Living like a monk while scrimping and saving for a house gets old when you realize that your efforts aren’t getting you anywhere near where you’re attempting to go …

As for the situation now, the inflation warning signs are all around us if we dare to look. According to a report published in the May 21, 2021 issue of The Wall Street Journal, lumber may exhibit the most visible spike in prices, but consider what futures prices are showing for a whole range of commodities when compared to just one year ago:

Gold: +7%

Platinum: +29%

Wheat: +31%

Cotton: +40%

Coffee: +42%

Sugar: +52%

Silver: +56%

Natural gas: +65%

Soybeans: +81%

Crude oil: +85%

Cooper: +86%

Gasoline: +96%

Corn: +108%

Lumber: +278%

It doesn’t take a degree in economics to know that these sorts of trends are pretty alarming. Whenever it has an opportunity to take hold, inflation is one of the most insidious of economic problems – and one that’s extremely difficult to reverse. Inflation is also very debilitating for the personal budgets of the large majority of consumers, and it causes the most harm to those on the lower rungs of the economic ladder.

The next few months will tell us if this particular inflation is going to be a temporary phenomenon or not. How much of the commodity price increases are attributable to transitory events that will ease as the world’s economies move further from lockdown?

But if this inflation turns out to be something more structural or more directly correlated to the massive increase in government spending paid for by the expanded money supply, expect the economic (and political) climate to begin to look vastly different in the coming months.

Inflation will be uncharted territory for most people. But a few of us veterans will be around to provide context and counsel — and perhaps engage in a bit of “Sister Toldja” commentary while we’re at it …

As the United States emerges from the COVID crisis, the shape of the American economy is coming into clearer view. Part of that picture is the growing realization that lockdown policies, vaccination rollouts and government stimulus actions have created imbalances in many sectors — imbalances that will time to return to equilibrium.

Everyone knows the business sectors that have been hammered “thanks” to COVID: hospitality and foodservice, travel and tourism, the performing arts, sports and recreation, commercial real estate.

At the same time, other corners of the economy have blossomed — home remodeling, consumer electronics … and the public sector. This last one isn’t a function of any kind of increased demand, but rather pandemic-long guaranteed continuing income to workers on the public payroll.

As we emerge, factories and the building trades are finding it difficult to ramp up their operations to meet growing demand, hampered in part by supply chain issues and shortages of raw materials and parts sourced from offshore suppliers. As of now, most economists believe that such shortages won’t turn out to be long-term problems — but we shall see over time if this is actually the case.

Another imbalance is what’s been happening to the labor force. Government stimulus checks and unemployment benefits have been sufficiently robust so as to depress the number of workers seeking a return to employment in certain sectors — particularly in the service industries. As just one example, restaurants everywhere are finding it more than a little difficult to staff their reopened locations.

The latest forecasts are for the U.S. economy to grow at a blistering pace during the balance of 2021 — perhaps as high as an 8% or 9% seasonally adjusted rate of growth. That would be historic. But not everyone is going to benefit.

In a recent Wall Street Journal article, David Lefkowitz of UBS Global Wealth Management points out that “the very sudden stop to the economy and then the very quick restart has created a lot of havoc — a lot of businesses have gotten caught flat-footed.” But beyond this is the very real likelihood that inflation will emerge as a key factor in the economy, for the first time in more than 40 years.

Viewed holistically, the situation in which we find ourselves is one where many new and unusual “ingredients” have gone into the economy over the past year, resulting in an economic brew that is just as unusual — and perhaps even unique in our history.

An artificially depressed economy due to government fiat … followed by massive economic stimulus paid for by expanding the money supply … coupled with sudden demand propelling certain industries over others due to government-driven dictates: for sure it’s a new mix of factors. Considering this, I’m not at all sure that very many people inside or outside of government have a clear handle on what the next 18 months will actually bring.

But that doesn’t mean we can’t speculate about it, right? In the comment section below, please share your perspectives on what’s in store for the U.S. economy. I’m sure others will be interested in reading your thoughts.

One of the many ripple-effects of the COVID-19 pandemic is the effect it’s had on the demand for commercial office space.

In a word, it’s been pretty devastating.

The numbers are stark. According to an estimate published by Dallas-based commercial real estate services and investment firm CBRE Group, Inc., as of the end of 2020, nearly 140 million sq. ft. of office space was available for sublease across America.

That’s a 40% jump from the previous year. Not only that, it’s the highest sublease availability figure since 2003, which means the situation is worse than even during the Great Recession of 2008.

Of course, it isn’t surprising to expect that more sublet space would become available during periods of economic downturn, when many businesses naturally look for ways to cut costs. But those dynamics typically reverse when the economy picks up again. This time around, it’s very possible – even probable – that the changes are permanent.

The reason? Many companies that reduced their office space footprint in 2020 didn’t doing so because they we’re suffering financially. It was because of government-mandated lockdowns. And now they’re expecting many of those employees to continue working from home, either part-time or full-time, after the pandemic subsides.

Employee surveys have shown that many workers prefer to work from home where they can avoid the hassle and expense of daily commuting. It’s understandable that they don’t want that to change back again. In many business sectors which don’t actually need their workforce be onsite to produce revenue, companies are simply ratifying a reality that’s already happened. Accordingly, they’ve changed their expectations about employee attendance at the office going forward.

Commercial landlords are now feeling the long-term effects of this shift in thinking. Rents for prime office space fell an average of 13% across the United States over the past year. In places like New York and San Francisco the drop has been even steeper — as much as a 20% contraction.

For many of the lessees, it’s less onerous to sublease space to others rather than attempt to undertake the messy business of renegotiating long-term lease contracts with landlords. Still, there’s pain involved; sublease space historically comes with a significant discount — around 25% — but with the amount of sublet space that’s been coming onstream, those discounts may well go even deeper due to the lack of demand.

The cumulative effect of these leasing dynamics is to put even more downward pressure on broader rental rates, as the deeply discounted space that’s available to sublet puts more pressure on the price of “regular” office space. It’s a classic downward spiral.

Is there a natural bottom? Most likely, yes. But we haven’t reached it yet, and it’ll be interesting to see when — and at what level — things finally even out. In the meantime, it isn’t a very pretty picture.

What are you witnessing with regards to office space dynamics within your own firm, or other companies in your business community? Please share your thoughts below.

If you’ve taken a look at September’s U.S. unemployment figure – 3.5% — you’re seeing the lowest level of unemployment in over 50 years. And for particular subgroups of the population, they’re enjoying their lowest employment percentages ever — at least since records have been kept.

It’s definitely something to cheer about. But at the same time, it’s become increasingly evident that wage growth isn’t happening in tandem with lower unemployment. And that includes industrial wages as well.

In fact, September results show the first dip in wages – albeit slight – in the past two years.

According to Liu and Leduc, as certain tasks move more toward automation, employees are losing bargaining power within their organizations. When people fear that they could lose their jobs to a robot or a machine, there’s a hesitation to ask for higher wages as that might hasten the eventuality.

The net result is a widening gap between productivity and pay.

But does this situation apply across all of industry? Perhaps not. Last year, manufacturing expert and Forbes magazine contributing writer Jim Vinoski noted that “huge swaths of industry remain decidedly low-tech and heavily manual.”

The reason? Complexity, volume and margins are often barriers to the implementation of automation in many applications. Just because something can be automated doesn’t mean that there’s a compelling economic argument to do so – particularly if the production volumes aren’t in the league of “mass manufacturing.”

Jobs in engineering and R&D are even less likely to become automated. After all, probably the single most important attribute of employees in these positions is the ability to “think outside the box” – something artificial intelligence hasn’t come anywhere close to replicating (at least not yet).

What are your thoughts about automation and how it will affect employment and wage growth? Please share your perspectives with other readers.

Astonishingly tone-deaf and factually questionable: “China is going to eat our lunch? Come on, man … they can’t even figure out how to deal with the fact that they have this great division between the China Sea and the mountains … in the west. They can’t figure out how they’re going to deal with the corruption that exists within the system. I mean, you know, they’re not bad folks, folks. But guess what? They’re not competition for us.” (Former Vice President Joe Biden, May 1, 2019)

In recent months, we’ve been hearing a wide range of views about China’s economic and political aspirations and their potential implications for the United States.

Some of the opinions being expressed seem to be polar opposites — such as President Donald Trump’s pronouncements that the United States has been “ripped off” by China for decades. Contrast this with former Vice President Joe Biden’s dismissive contention that China represents no competition for the United States at all.

The column is titled Trump Is Waging (and Winning) a Peaceful World War III Against China. My curiosity aroused, I decided to get in touch with my brother, Nelson Nones, who has lived and worked in the Far East for the past 20+ years. Being an American “on the ground” in countries like China, Taiwan, South Korea, Thailand and Malaysia gives Nelson an interesting perspective from which to be a “reality check” on the views we’re hearing locally.

I sent Nelson a link to the Morris op-ed and asked for his reaction. Here is what he communicated back to me:

I think Dick Morris is correct to contend that the Chinese government’s long-term vision is bigger than just accumulating more wealth and power. In fact, I wrote about this topic in the book I co-authored with Janson Yap, when describing China’s “Belt and Road” initiatives as a geographic positioning threat to Singapore.

I wrote:

“As a land-based strategy, the SREB [Silk Road Economic Belt] promises greater long-term rewards for China than the MSR [Maritime Silk Road]; these would echo the impact of the completion of the first transcontinental railroad in 1869, which marked the beginning of the ascendancy of the U.S. to becoming one of the preeminent economic empires of all time.”

The context here is, if you look back through history, the world’s most dominant economic empires were either terrestrial or maritime — but not both — until the U.S. came along. As I further wrote in the book:

“After gaining control over both strategic land and maritime trade routes with the completion of the Panama Canal in 1913, America became the first land-based and maritime economic empire in history; its dominance has spanned over a century, from 1916 to the present. Uncoincidentally, the American economic empire began when the Panama Canal was completed, but the Panama Canal has arguably contributed far less to America’s GDP than the country’s investments in transcontinental rail and road transportation infrastructure.”

In short, I am absolutely sure China’s government aspires to overtake the U.S. as the world’s dominant terrestrial and maritime economic empire, and to hold that position for at least a century if not longer. But this would not be the first time in history that China has held such a position.

For the historical context, refer to: http://fortune.com/2014/10/05/most-powerful-economic-empires-of-all-time/. There you will see that the U.S. produced half the world’s economic output in circa 1950. China’s Song Dynasty was the world’s preeminent economic empire in circa 1200 AD, producing 25% to 30% of global output. Only the U.S. and the Roman Empire have ever matched or exceeded that marker.

I can tell you from my considerable experience on the ground in China that the strategic vision of its leaders is grounded in much more than just backward-looking grievance and necessity. Although the 19th Century Opium Wars (which were fought during the Qing Dynasty against the British Empire, and occurred during the period of the British Empire’s economic ascendancy) are often trotted out in China’s government-controlled English language dailies, the Chinese people I know have little or no knowledge of the Opium Wars or the colonial victimization China allegedly suffered a century and a half ago.

But they are acutely aware, and genuinely proud, of China’s emergence as a leading economic powerhouse; and this is how the Chinese government maintains its legitimacy.

China’s ambitions, in other words, have much more to do with reinstating its former glory (the Song Dynasty economic empire) than with righting wrongs (dominance by colonial powers), and are fundamental props for maintaining the Chinese Communist Party’s grip on power.

This view renders many of Dick Morris’ comments unnecessarily hyperbolic; for example “[China’s] goal is to reduce the rest of the world to colonial or dominion status, controlled politically, socially, intellectually, and economically by China. In turn, China is run by a handful of men in Beijing who need not pay the slightest attention to the views of those they govern or the nations they dominate.”

No, China’s goal is to become the world’s dominant economic empire but, just as the Americans before them, they don’t have to exert the same degree of control over the rest of the world as they do within their own territory to achieve this goal.

And no, they require constant support from the Chinese population to achieve this goal, even though they run an authoritarian state. Why else would they devote so many resources to the “Great Chinese Firewall” if there is no need to “pay the slightest attention to the views of those they govern”?

Yes, Trump’s trade war with China is important but his motive is to reverse the flow of jobs and capital out of the U.S. to China, which is not the same thing as launching an “economic World War III.” At a more practical and mundane level, it’s to fulfil a pile of campaign promises which Trump made when he was running for President, and to secure the loyalty of his base.

_______________________________

So there you have it: the perspectives of someone “on the scene” in the Far East — holding a view that is more nuanced than the hyperbole of the alarmists, but also clear-eyed and miles apart from the head-in-the-sand naiveté of other politicians like Joe Biden.

Let’s also hope for a more meaningful and reality-based discourse on the topic of China in the coming months and years.

Over the past year, Americans have been fed a fairly steady stream of news about the People’s Republic of China – and most of it hasn’t been particularly positive.

While Russia may get the more fevered news headlines because of the various political investigations happening in Washington, the current U.S. presidential administration hasn’t shied away from criticizing China on a range woes – trade policy in particular most recently, but also diverse other issues like alleged unfair technology transfer policies, plus the building of man-made islands in the South China Sea thereby bringing Chinese military power closer to other countries in the Pacific Rim.

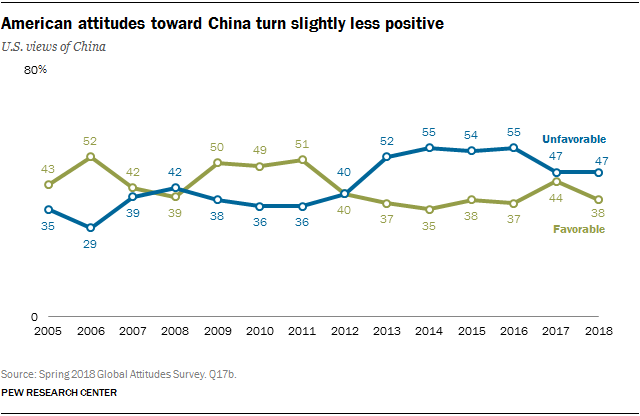

The drumbeat of criticism could be expected to affect popular opinion about China – and that appears to be the case based on a just-published report from the Pew Research Center.

The Pew report is based on a survey of 1,500 American adults age 18 and over, conducted during the spring of 2018. It’s a survey that’s been conducted annually since 2012 using the same set of questions (and going back annually to 2005 for a smaller group of the questions).

The newest study shows that the opinions Americans have about China have become somewhat less positive over the past year, after having nudged higher in 2017.

The topline finding is this: today, ~38% of Americans have a favorable opinion of China, which is a drop of six percentage points from Pew’s 2017 finding of ~44%. We are now flirting with the same favorability levels that Pew was finding during the 2013-2016 period [see the chart above].

Drilling down further, the most significant concerns pertain to China’s economic competition, not its military strength. In addition to trade and tariff concerns, another area of growing concern is about the threat of cyber-attacks from China.

There are also the perennial concerns about the amount of U.S. debt held by China, as well as job losses to China; this has been a leading issue in the Pew surveys dating back to 2012. But even though debt levels remain a top concern, its raw score has fallen pretty dramatically over the past six years.

On the other hand, a substantial and growing percentage of Americans expresses worries about the impact of China’s growth on the quality of the global environment.

Interestingly, the proportion of Americans who consider China’s military prowess to be a bigger threat compared to an economic threat has dropped by a statistically significant seven percentage points over the past year – from 36% to 29%. Perhaps unsurprisingly, younger Americans age 18-29 are far less prone to have concerns over China’s purported saber-rattling – differing significantly from how senior-age respondents feel on this topic.

Taken as a group, eight issues presented by Pew Research in its survey revealed the following ranking of factors, based on whether respondents consider them to be “a serious problem for the United States”:

Large U.S. debt held by China: ~62% of respondents consider a “serious problem”

Cyber-attacks launched from China: ~57%

Loss of jobs to China: ~52%

China’s impact on the global environment: ~49%

Human rights issues: ~49%

The U.S. trade deficit with China: ~46%

Chinese territorial disputes with neighboring countries: ~32%

Tensions between China and Taiwan: ~21%

Notice that the U.S. trade deficit isn’t near the top of the list … but Pew does find that it is rising as a concern.

If the current trajectory of tit-for-tat tariff impositions continues to occur, I suspect we’ll see the trade issue being viewed by the public as a more significant problem when Pew administers its next annual survey one year from now.

Furthermore, now that the United States has just concluded negotiations with Canada and Mexico on a “new NAFTA” agreement, coupled with recent trade agreements made with South Korea and the EU countries, it makes the administration’s target on China as “the last domino” just that much more significant.

More detailed findings from the Pew Research survey can be viewed here.

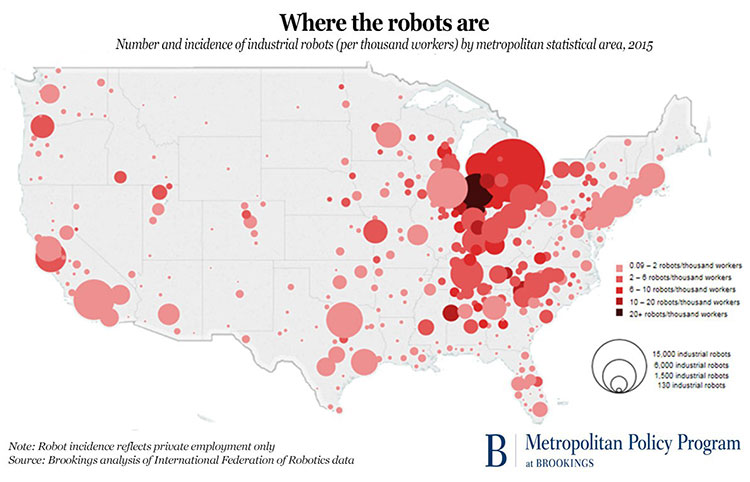

The Brookings Institution has just published a fascinating map that tells us a good deal about what is happening with American manufacturing today.

Headlined “Where the Robots Are,” the map graphically illustrates that as of 2015, nearly one-third of America’s 233,000+ industrial robots are being put to use in just three states:

Michigan: ~12% of all industrial robots working in the United States

Ohio: ~9%

Indiana: ~8%

It isn’t surprising that these three states correlate with the historic heart of the automotive industry in America.

Not coincidentally, those same states also registered a massive lurch towards the political part of the candidate in the 2016 U.S. presidential election who spoke most vociferously about the loss of American manufacturing jobs.

The Brookings map, which plots industrial robot density per 1,000 workers, shows that robots are being used throughout the country, but that the Great Lakes Region is home to the highest density of them.

Toledo, OH has the honor of being the “Top 100” metro area with the highest distribution of industrial robots: nine per 1,000 workers. To make it to the top of the list, Toledo’s robot volume jumped from around 700 units in 2010 to nearly 2,400 in 2015, representing an average increase of nearly 30% each year.

For the record, here are the Top 10 metropolitan markets among the 100 largest, ranked in terms of their industrial robot exposure. They’re mid-continent markets all:

Toledo, OH: 9.0 industrial robots per 1,000 workers

Detroit, MI: 8.5

Grand Rapids, MI: 6.3

Louisville, KY: 5.1

Nashville, TN: 4.8

Youngstown-Warren, OH: 4.5

Jackson, MS: 4.3

Greenville, SC: 4.2

Ogden, UT: 4.2

Knoxville, TN: 3.7

In terms of where industrial robots are very low to practically non-existent within the largest American metropolitan markets, look to the coasts:

Ft. Myers, FL: 0.2 industrial robots per 1,000 workers

Honolulu, HI: 0.2

Las Vegas, NV: 0.2

Washington, DC: 0.3

Jacksonville, FL: 0.4

Miami, FL: 0.4

Richmond, VA: 0.4

New Orleans, LA: 0.5

New York, NY: 0.5

Orlando, FL: 0.5

When one consider that the automotive industry is the biggest user of industrial robots – the International Federation of Robotics estimates that the industry accounts for nearly 40% of all industrial robots in use worldwide – it’s obvious how the Midwest region could end up being the epicenter of robotic manufacturing activity in the United States.

It should come as no surprise, either, that investments in robots are continuing to grow. The Boston Consulting Group has concluded that a robot typically costs only about one-third as much to “employ” as a human worker who is doing the same job tasks.

In another decade or so, the cost disparity will likely be much greater.

On the other hand, two MIT economists maintain that the impact of industrial robots on the volume of available jobs isn’t nearly as dire as many people might think. According to Daron Acemoglu and Pascual Restrepo:

“Indicators of automation (non-robot IT investment) are positively correlated or neutral with regard to employment. So even if robots displace some jobs in a given commuting zone, other automation (which presumably dwarfs robot automation in the scale of investment) creates many more jobs.”

What do you think? Are Messrs. Acemoglu and Restrepo on point here – or are they off by miles? Please share your thoughts with other readers.

Most people in business and politics have heard of the World Economic Forum (WEF), best known for holding its annual meeting for the world’s glitterati every January in Davos, Switzerland.

Most people in business and politics have heard of the World Economic Forum (WEF), best known for holding its annual meeting for the world’s glitterati every January in Davos, Switzerland.