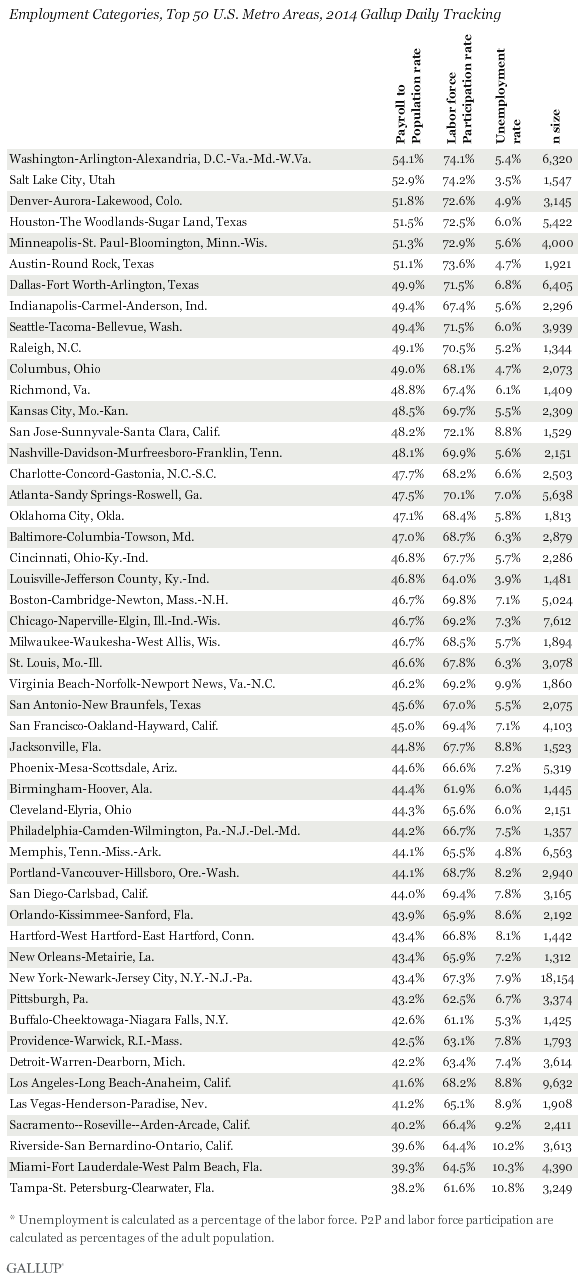

If you’ve taken a look at September’s U.S. unemployment figure – 3.5% — you’re seeing the lowest level of unemployment in over 50 years. And for particular subgroups of the population, they’re enjoying their lowest employment percentages ever — at least since records have been kept.

It’s definitely something to cheer about. But at the same time, it’s become increasingly evident that wage growth isn’t happening in tandem with lower unemployment. And that includes industrial wages as well.

In fact, September results show the first dip in wages – albeit slight – in the past two years.

What gives?

According to Zheng Liu and Sylvain Leduc, two economics researchers at the Federal Reserve Bank of San Francisco, the cause of stagnating wages in an otherwise robust economy can be laid at the doorstep of automation.

According to Liu and Leduc, as certain tasks move more toward automation, employees are losing bargaining power within their organizations. When people fear that they could lose their jobs to a robot or a machine, there’s a hesitation to ask for higher wages as that might hasten the eventuality.

The net result is a widening gap between productivity and pay.

But does this situation apply across all of industry? Perhaps not. Last year, manufacturing expert and Forbes magazine contributing writer Jim Vinoski noted that “huge swaths of industry remain decidedly low-tech and heavily manual.”

The reason? Complexity, volume and margins are often barriers to the implementation of automation in many applications. Just because something can be automated doesn’t mean that there’s a compelling economic argument to do so – particularly if the production volumes aren’t in the league of “mass manufacturing.”

Jobs in engineering and R&D are even less likely to become automated. After all, probably the single most important attribute of employees in these positions is the ability to “think outside the box” – something artificial intelligence hasn’t come anywhere close to replicating (at least not yet).

What are your thoughts about automation and how it will affect employment and wage growth? Please share your perspectives with other readers.