Can the World Economic Forum be any less useful or relevant?

Most people in business and politics have heard of the World Economic Forum (WEF), best known for holding its annual meeting for the world’s glitterati every January in Davos, Switzerland.

Beyond that international confab, WEF provides a set of “Transformation Maps” on its website which are described as “a constantly refreshed repository of knowledge about global issues, from climate change to the future of work.”

“Transformation Maps are the World Economic Forum’s dynamic knowledge tool,” the website declares. “They help users to explore and make sense of the complex and interlinked forces that are transforming economies, industries and global issues.”

The maps present insights written by so-called experts along with machine-curated content. Together, “the information allows users to visualise and understand more than 250 topics and the connections and inter-dependencies between them, helping in turn to support more informed decision-making by leaders.”

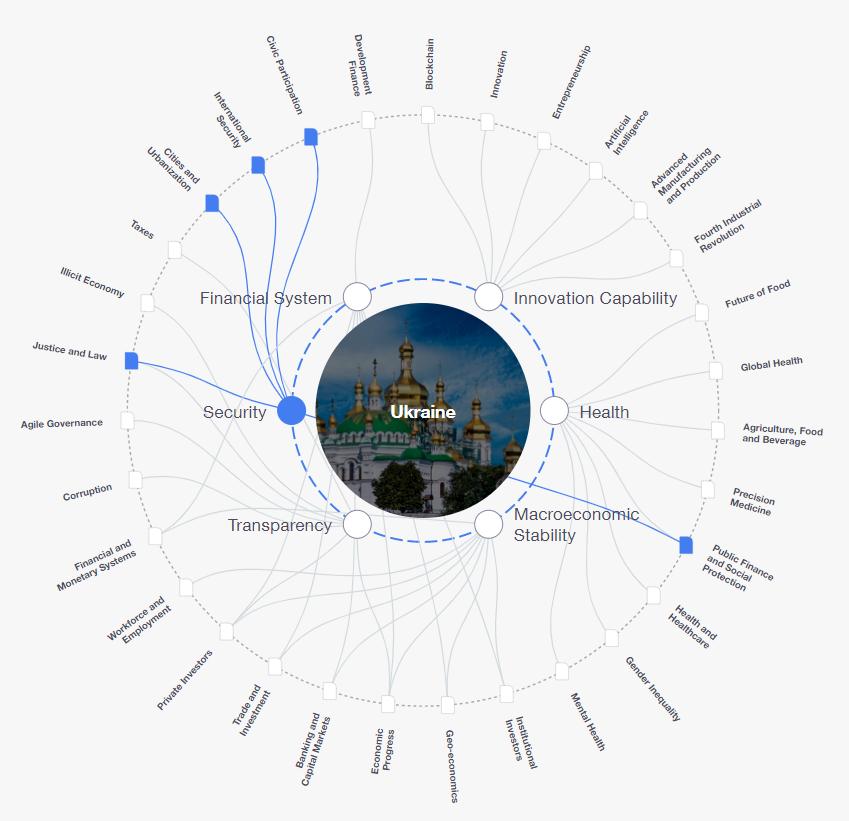

That page displays 293 different topics. Scrolling down a good ways finally brings up “Ukraine” … and here’s what is displayed after clicking on the “Security” issue:

Explaining how the chart was developed, the website reports:

“This Transformation Map explores key issues for Ukraine based on its rankings in the most recent edition of the World Economic forum’s Global Competitiveness Index.”

For the record, those six “key issues” are Financial System, Innovation Capability, Health, Macroeconomic Stability, Transparency and Security.

The Security issue then links to five other topics (Public Finance and Social Protection, Justice and Law, Cities and Urbanization, International Security and Civic Participation).

Curious to see what content would be displayed, I clicked the International Security topic, which causes the International Security Transformation Map to appear. Only then did I finally learn that:

“The return of great power competition has been accompanied by the outbreak in Ukraine of Europe’s largest ground war since World War II.”

I must admit that I am quite impressed with how these Transformation Maps have helped me to visualize and understand the connections and inter-dependencies between Ukraine and International Security … and it is now completely clear to me how these tools support more informed decision-making by leaders. [Feel free to insert snark emoji here.]

Researchers from the Harvard and Tilburg Business Schools think they’ve found a method to do just that.

One of the research techniques that has sprung up in the era of online engagement and interactivity is “mining” reader comments — then analyzing the granular data to discern their wider implications for companies and brands.

One way this happens is by analyzing the words that employees use to describe their own companies on review sites. Doing so can provide clues as to what’s going on inside these companies that others can’t discovers based on forward-facing reporting about the organizations in the business or news press.

Underscoring this point, a study conducted jointly by researchers at Harvard Business School and the Tilburg School of Economics and Management in The Netherlands has found that such information extracted from employee-review websites like Glassdoor.com is helpful in being able to predict potential misconduct beyond other observable factors such as a firm’s financial performance and industry risk analysis.

The correlating factors revolve around employee observations concerning the environments in which they work – factors like:

Company culture

Company operations

Control practices

Performance pressures

Negative or critical comments made within these broad categories contribute to weighing the risk for corporate misconduct. Business management professor Dennis Campbell of the Harvard Business School notes that the “tone at the bottom” revealed by such comments can be a good early-warning signal of potential misconduct.

“Our theory is that what leads people to commit misconduct is actually the environment they are in,” adds Ruidi Shang, the Tilburg professor heading up the research team.

The Harvard/Tilburg study sifted through information from anonymous reviews of publicly traded U.S. companies that had been posted on Glassdoor.com over a nine-year period between 2008 and 2017. Focusing on nearly 1,500 companies that had been the subject of ten or more review entries each over the period, by comparing keywords in the comments to actual corporate misconduct cases brought against public U.S. firms over the same period, direct correlations were found between the statements and the companies that were later found guilty of misconduct.

The researchers discovered that certain terms and phrases used by employees in their comments correlate highly to misconduct cases – terms like bureaucracy, compliance, favoritism, harassment, hostile and strict. Such terms came up disproportionately more frequently in the discussions and comments.

Of course, such analyses are rough measures at best. Because the researchers drew comparisons between the comments and the corporate misconduct based only on cases that the U.S. government pursued, the methodology would have missed misconduct wasn’t known (or pursued) by the government. But as for providing “directional indicators,” the methodology seems to be a valid approach. I think we could see it being employed by Wall Street analysts as part of efforts to predict threats to future financial performance – and other potential problems — based on what the granular data reveals.

More details on the study and its findings can be read in this report.

This summer’s natural disasters have been par for the course. Just like clockwork, we’ve had wildfires, tropical storms and flooding — with likely more such events happening between now and the end of the season.

And even as these events occur with numbing regularity, it seems that year after year we hear the same stories of people being caught up in nature’s wake. No matter how much effort officials put into evacuation planning and alerts, not everyone hears the message — or “gets it” if they do hear it.

Some states such as Florida and California have worked to build programs that provide explicit guidelines for local officials to follow during evacuations. For example, California’s guidance urges communities to rely on the federal warning system so that alerts can reach the greatest number of people most quickly — usually through cellphone alerts. Local officials are routinely reminded that “incomplete or imperfect information is not a valid reason to delay or avoid issuing a warning.” When time is of the essence, the “20-80 rule” of information is better than an “80-20” ratio.

The problem is, research shows that many people aren’t inclined to act on these alerts. Typically only about half of those located in mandatory evacuation zones actually leave before hurricanes hit. For wildfires the percentage of people who comply is higher, but still far too many ignore the orders

Why do people stay rather than leave? Research finds a variety of factors at play, including:

Health problems or disability issues that make it difficult for some people to evacuate

Lack of transportation

Skepticism about the level of danger

Concern about leaving property unattended

The inability to accommodate pets, livestock or animals such as horses

Wildfires make for particularly challenging situations because they can quickly shift direction with very little warning. Rural and remote towns with fewer resources and fewer roads face particular challenges. Often the main evaluation routes are narrow, two-lane thoroughfares that can’t handle the sudden influx of traffic when thousands are being directed to leave the vicinity.

Flash floods can also hit without warning, but with hurricanes it’s often easier to plan for evacuations because typically there are several days’ warning before exit routes will need to shut down.

Florida has experimented with various tactics to improve evacuations by opening emergency shoulders to highway traffic, adding emergency roadside services on major evacuation routes, and posting more cameras and message signs to alert drivers to changing traffic conditions and other developments.

Sending a single unambiguous message from local officials is the best policy regarding evacuations. Offering “options” can create confusion and lead people to pick the option that appeals most to them personally — which might not be the safest one. Whatever the communication, it must be definitive and precise. Otherwise, the whole evacuation effort can go sidewise.

Fort McMurray Fire (2016)

Lest anyone become complacent about the dangers that natural disasters can pose, watch this terrifying “you are there” dash cam footage of a resident of Fort McMurray attempting to escape the wildfires that engulfed a portion of that Canadian city in 2016. There’s no news anchor voiceover … no ominous music in the background to add “drama” … just the gripping footage as documented by the camera. Viewing it once a year is enough to become “scared straight” about natural disasters, all over again.

Remote work has turned each new hire into a national competition.

Historically, one of the challenges faced by smaller urban markets was their ability to hang on to talent. Younger workers often found it more financially lucrative following their education to relocate to major metropolitan areas in order to snag higher paying positions with the companies based there.

In time, however, the high cost of living in the large metro markets, coupled with the desire to ditch the unbearable congestion in those areas, led to the formation of new businesses outside the major tech centers that found it easier to compete with the major urban areas for talent.

Established companies found the same dynamics at work, too. The rise of markets like Charlotte, Salt Lake City, Pittsburgh and Boise underscored that the spread of the “new economy” had migrated to places beyond the traditional hubs of Boston, Washington, New York City, San Francisco/Silicon Valley, Los Angeles and others.

Then the COVID pandemic came along. Suddenly, it didn’t matter where employees lived as companies quickly figured out ways to have, in some cases, nearly their entire workforce working remotely.

It didn’t take long for employees in some of the market hardest-hit by COVID to flee to far-flung regions. New York City residents moved to the Hudson River Valley, South Florida and other locations. For California residents it was off to Nevada, Montana or Idaho. Boston-based workers decamped for Vermont or Maine.

It soon became apparent that for many tech jobs, the need to be clustered together in offices simply wasn’t that critical. And in an ironic twist, smaller-city startups and other firms are now starting to feel the effects of the establishment biggies poaching their own employees.

It’s particularly ironic; whereas before, companies that couldn’t compete with Silicon Valley heavyweights on salary could offer a whole lot of lifestyle to even the playing field. Now they’re finding that “work from anywhere” policies have nullified whatever advantages they had.

Those big-city salaries can be used to purchase a lot of house in whatever kind of environment desired — even if it’s a lakeside cabin in the middle of nowhere.

It also means that, all of a sudden, everyone’s competing with companies all over the country for talent — and hanging on to the existing talent is that much more difficult. When people are being offered 20% higher salary with no requirement to relocate, that’s a proposition many people are going to consider.

Another interesting consequence is that tech labor force is probably geographically more evenly distributed than it’s ever been — and the workers residing outside the traditional tech hubs are benefiting accordingly — At least in the short-term.

In the longer term, companies based in the smaller markets hope that they’ll have access to those same new tech migrants if work-from-home policies change yet again. But that’s a big “if” …

Millions of Americans age 20 to 24 fall into the NEET category: “Not in Employment, Education or Training.”

The COVID-19 pandemic has exposed some interesting fault-lines in the socio-economic fabric of the United States. One of these relates to young adults — those between the ages of 20 and 25. What we find paints a potentially disturbing picture of an economic and employment situation that may not be easily fixable.

A recently issued economic report published by the Center for Economic and Policy Research (CEPR) focuses on the so-called “NEET rate“– young Americans who are not employed, not in school, and not in training.

As of the First Quarter of 2021, the NEET category represented nearly 4 million Americans between the ages of 20 and 24. This eye-popping statistic goes well beyond the particular circumstances of the pandemic and may turn out to be an economically devastating trend with a myriad of adverse ripple effects related to it.

Look at any business newspaper or website these days and you’ll see reports regularly about worker shortages across many sectors — including unfilled jobs at the lower end of the pay scale which offer employment opportunities that fit well with the capabilities of lower skilled workers newly coming into the workplace.

At this moment, pretty much anyone who is willing to look around can easily find employment, schooling, or training of various kinds. But for millions of Americans in the 20-24 age cohort, the job opportunities appear to be falling on deaf ears. Bloomberg/Quint‘s reaction to the CEPT study certainly hits home:

“Inactive youth is a worrying sign for the future of the [U.S.] economy, as they don’t gain critical job skills to help realize their future earnings potential. Further, high NEET rates may foster environments that are fertile for social unrest.”

… Daily urban strife in Portland, Minneapolis and Seattle, anyone?

It doesn’t much help that younger Americans appear to be less enamored with the basic economic foundations of the country than are their older compatriots. A recent poll by Axios/Momentive has found that while nearly 60% of Americans hold positive views of capitalism, those sentiments are share by a only little more than 40% of those in the 18-24 age category.

Moreover, more than 50% of the younger group view socialism positively compared to only around 40% of all Americans that feel the same way.

The coronavirus pandemic may have laid bare these trends, but it would be foolish to think that the issues weren’t percolating well before the first U.S. businesses began to lock down in March 2020.

And more fundamentally, one could question just how much government can do to reverse the trend; perhaps the best thing to do is to stop “helping” so much … ?

More information about the CEPR report can be viewed here. What are your thoughts on this issue? Please share your views with other readers here.

The first-ever in-flight magazine has now become the latest one to fold. American Airlines debuted its seatback publication back in 1966, establishing a precedent that would soon be followed by all the other U.S.-based passenger airlines as well as many foreign carriers.

The American Way (later shortened to American Way) started out as a slender booklet of fewer than 25 pages that focused on educational and safety information about American Airlines, its equipment and staff. Initially an annual publication, American Way soon became a monthly magazine.

Its early success was due to the captive audience that were airline passengers “back in the day.” Unless you brought your own book or periodicals on board, the in-flight magazine was a welcome way to pass the time in lieu of conversing with your seatmates or simply dozing.

As all other American passenger carriers launched their own in-flight magazines, many of them grew to more than 100 pages in length. In their heyday, it’s very likely that the readership levels of these publications outstripped those of many consumer magazine titles.

But as with so much else that’s happened in publishing, they were destined to become a casualty of changing consumer behaviors. Interest in leafing through in-flight magazines dropped off when travelers started uploading books, movies and TV shows onto their electronic devices – or tapping into the airlines’ own electronic entertainment options. And when that happened, advertiser interest – the lifeblood of any commercial publication – fell off as well.

… and the last issue (June 2021).

American Way’s last issue is this month. Proud to the last, its cover story is about “America’s hippest LGBTQ neighborhoods.” But after June, the magazine will join the in-flight publications that were dropped by Delta and Southwest Airlines during the COVID-19 pandemic and won’t be returning.

To be sure, several of them continue to hang on. United Airlines’ Hemispheres magazine is due back on planes in July, and Virgin Atlantic has plans to relaunch its magazine Vera in September. But these would seem to be in the minority as the other in-flight magazines have disappeared into the ether.

Will they be missed? Travel analyst Henry Harteveldt doesn’t seem to think so, stating recently to USA Today:

“I don’t think frequent travelers – or infrequent travelers – will notice or really care to any great degree if the magazine[s] disappear. Certainly, nobody ever chose an airline because of the in-flight magazine.”

I’m in agreement with Mr. Harteveldt on this. But how about you? Will you be missing in-flight magazines at all?

Responses from two people in particular are worth highlighting for the “countervailing views” that they espouse. I think both have merit.

The first response came from my brother, Nelson Nones, who has lived and worked outside the United States for decades. His perspectives are interesting because, while fully understanding domestic events and policies, he also brings an international orientation to the discussion due to his own personal circumstances. Nelson is looking to history for his perspectives on the inflation issue, offering these comments:

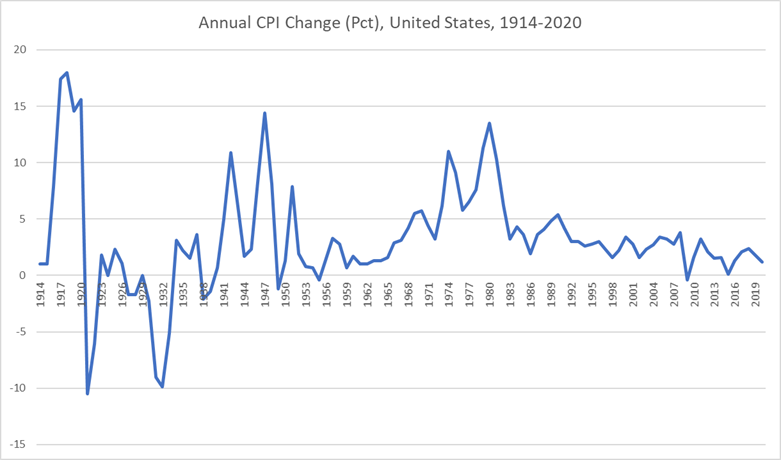

The chart below shows annual U.S. CPI percentage change for the past 106 years:

Projecting the latest (April 2021) Consumer Price Index forward to an entire year suggests that the U.S. will experience a 3.1% inflation rate in 2021. That would be higher than in any year since 2011, which was a bounce-back year following the Great Recession. Otherwise, the generic inflation trend has been consistently down since 1982 (nearly 40 years).

If the historical trends are any guide, and if we are indeed entering a persistent inflationary phase, it would take another decade before inflation growth approaches the levels seen during the 1970s.

But I think the likeliest scenario is experiencing a sharp uptick this year due to pent-up demand following the COVID-19 pandemic that will causie spot shortages, followed by resumption of a downward trend over the following ten years or so.

That’s similar to the pattern you can observe in the chart [above] during the years following the end of World War II, which had also created massive pent-up consumer demand.

Consider that the coronavirus pandemic hasn’t really altered the underlying economic fundamentals. The past 40 years has witnessed an explosion of manufacturing capacity in China and other developing countries, and that hasn’t gone away. Meanwhile, dependency on oil — a key driver of inflation in the 1970s — has shrunk due to improved energy efficiency and aggressive exploitation of renewable energy resources, which for all practical purposes are in infinite supply.

Another factor, which doesn’t get as much attention as it probably should, is declining birth rates and aging of the population on a global scale, leading to a slower rate of population growth in the future that may constrain demand for consumer products in comparison to the past century. Let’s face it — we old farts just don’t consume as much as growing families do!

So yes, we should keep an eye on inflation — but I don’t think we’re in for a repeat performance of the horrible 1970s.

Echoing Nelson’s thoughts are the perspectives of another business veteran — an editor and publisher who has been intimately involved in the commercial/B-to-B field for decades. Here is what he wrote to me:

I don’t want to get into a public debate with the inflationistas because I will never convince them that this is likely not a replay of the 1970s and early 80s inflationary period pre-[Paul] Volcker. (Speaking personally, I didn’t own a house until I was 42 for the very reasons you cited in your blog post, and I was just a lowly editor back then.)

What we’re seeing today is simply the price shock of suddenly soaring demand, aggravated in the case of some commodities such as steel by Trump-era tariffs.

All commodities are tied to the price of crude oil, the most volatile of all commodities, which is long-denominated in U.S. dollars. WTI crude pricing is now at around $63 per bbl. — about where it was in early 2020 before the pandemic hit. It went negative for a time during the worst period of the crash in worldwide demand that was brought about by the pandemic. Tanks couldn’t be found into which to put the excess crude coming out of the ground from U.S. fracking. Traders freaked out, as they sometimes do.

So naturally, the percentage changes today look jaw-dropping. I can go through all the other commodities mentioned in your post and provide simple explanations as to why each is currently on the rise. Logistical bottlenecks are a big problem with everything — but as with oil, most of the issue is the sudden surge in demand as the pandemic winds down even as production and logistics aren’t yet prepared to fulfill the need.

In other words, the situation has very little to do with government spending — especially since most of the infrastructure money isn’t even allocated, let alone spent. Also, the Biden administration has yet to raise a single tax. It can’t. Only the House Ways and Means Committee can initiate tax changes, and those must then go through the Senate to become law. Senate Minority Leader McConnell and his allies have made sure nothing has gotten through.

Of course, it never hurts to keep an eye on things — especially with structural inflation as you noted in your article. But it’s important to look also at other, broader data. The Producer Price Index in April did reflect the increase in commodities prices, but the Consumer Price Index, even though it had a month of robust increases, remains below 3% annualized. And the Personal Consumption Expenditure Price Index, which is what the Fed pays attention to the most, is still tracking under 2% on an annualized basis. (A little inflation can be a good thing, actually.)

On the income side, average wage rates aren’t rising; they’re more likely to be falling in the future as low-wage service workers, including those in foodservice, re-enter the market.

So in my view the things people see with inflation are most likely short-term issues. Let’s look at it again in six months to a year. I’d also suggest that people read economist Paul Krugman’s columns in the New York Times for a bit of perspective that’s counter to the views of the inflationistas, if only for balance. The monetarists have been wrong since Volcker squeezed out the inflationary spiral. It was painful, though — so we’ll want to keep an eye on things.

Considering the views put forward above, I think it’s fair to conclude that “the jury’s out” on whether we’re actually entering a prolonged inflationary period. If you have additional thoughts or perspectives to share on either side of the issue, I’m sure other readers would be interested to hear them. Feel free to leave a comment below.

The rise in lumber prices has received a certain degree of coverage in the news in recent weeks and months. For anyone who used the “pandemic period” to engage in home remodeling or renovation projects – perhaps moving away from “open concept everything” to reintroduce the designated spaces of yesteryear – the eye-popping price of lumber has come as something of a shock.

As for explaining the sharp increase, it’s logical to think that prices are directly correlated to the increased demand for the product. But this explanation is incomplete; the steep price rise in a wide range of commodities well beyond just lumber tells us that inflation isn’t relegated to just a few high-demand product categories. It’s the closest thing to “across the board” that we’ve seen in over 40 years — and the issue seemed to come out of nowhere.

Price inflation has been such a non-factor for so many decades, most consumers don’t even have personal memories of it. But those of us “of a certain age” remember well how difficult it was to navigate an “inflation-everywhere” environment where annual salary increases could never keep pace with rising prices.

It was difficult on people with fixed incomes, of course, but perhaps worse for young consumers who found that struggling to save for a down payment on a house purchase was a losing proposition as the gap widened rather than narrowed year over year. Living like a monk while scrimping and saving for a house gets old when you realize that your efforts aren’t getting you anywhere near where you’re attempting to go …

As for the situation now, the inflation warning signs are all around us if we dare to look. According to a report published in the May 21, 2021 issue of The Wall Street Journal, lumber may exhibit the most visible spike in prices, but consider what futures prices are showing for a whole range of commodities when compared to just one year ago:

Gold: +7%

Platinum: +29%

Wheat: +31%

Cotton: +40%

Coffee: +42%

Sugar: +52%

Silver: +56%

Natural gas: +65%

Soybeans: +81%

Crude oil: +85%

Cooper: +86%

Gasoline: +96%

Corn: +108%

Lumber: +278%

It doesn’t take a degree in economics to know that these sorts of trends are pretty alarming. Whenever it has an opportunity to take hold, inflation is one of the most insidious of economic problems – and one that’s extremely difficult to reverse. Inflation is also very debilitating for the personal budgets of the large majority of consumers, and it causes the most harm to those on the lower rungs of the economic ladder.

The next few months will tell us if this particular inflation is going to be a temporary phenomenon or not. How much of the commodity price increases are attributable to transitory events that will ease as the world’s economies move further from lockdown?

But if this inflation turns out to be something more structural or more directly correlated to the massive increase in government spending paid for by the expanded money supply, expect the economic (and political) climate to begin to look vastly different in the coming months.

Inflation will be uncharted territory for most people. But a few of us veterans will be around to provide context and counsel — and perhaps engage in a bit of “Sister Toldja” commentary while we’re at it …

Nearly everyone dislikes “office politics.” But does day-to-day employee gossip rise to that level? And have we lost something actually beneficial in the wake of remote work limiting our in-person interactions?

Ever since we were children, most of us have been conditioned to regard gossiping as a negative trait that any caring person should avoid doing.

At its core, the definition of the term is “people speaking evaluatively about someone who isn’t there.” But gossip can also relate to talking about rumors and conjecture regarding topics that go beyond just people.

Historically, gossip or the rumor mill in the office often served as a means by which anodyne-sounding corporate announcements would be subjected to a healthy degree of “whispered conversation and conjecture.” Or, as one DC-area employee put it in a recent Wall Street Journal article, ”You hear the surface story, and then you learn what the real story was – and that’s the gossip.”

In the months since mandatory office workplace lockdowns have been imposed, the gossip mill has fallen on hard times. Instead of serendipitous conversations happening in the lunchroom, in hallways or following group meetings, many workers are spending their days with just one person – themselves. Or they might be interfacing via Zoom meetings with the same handful of people from their core work team, where it’s always the same information being recycled among the same group of people.

Even for employees who have returned to working at their corporate offices, hybrid schedules often mean that there are far fewer daily interactions happening with other employees.

On one level, the reduction in gossiping may be reducing workplace “drama” and helping people focus better on their actual work tasks. Although the evidence is murky, productivity studies do appear to show an uptick in employee productivity since the onset of the COVID-19 pandemic.

On the other hand, in a recent survey of ~500 employees and business owners conducted by international legal consulting firm Seyfarth Shaw, the item that respondents missed the most after a year of remote working was “in-person and grown-up workplace conversations.”

For senior leadership, office gossip has been one way to rely on a kind of “early-warning system” about corporate initiatives or directives. In every office there seem to be a few people who have the pulse of the organization – it might be an executive assistant or some other staff support functionary – who other people feel comfortable confiding in and who in turn can communicate “the upshot” to the top brass. While difficult to quantify, that sort of dynamic really counts for something.

Of course, human nature being what it is, office gossip is never going to go away completely. But Skype or Zoom calls feel forced, and typing out thoughts or conjecture on IMs or e-mails is borderline-weird and feels inherently risky.

On balance, do you welcome the decline of face-to-face “gossip conversations” with colleagues — or do you suspect that a useful guerilla communications conduit has been lost? Please share your perspectives with other readers.

It had to happen: New state laws are now classifying robots as humans – specifically when it comes to traffic laws.

With the proliferation of delivery robots in quite a few urban areas, the issue was bound to arise. Car and Driver magazine reports that the state of Pennsylvania now defines delivery robots as “pedestrians” under a newly implemented law.

More specifically, the Pennsylvania legislative measures stipulate that “autonomous delivery robots” can lawfully maneuver on sidewalks, roadways and pathways. They’re allowed to carry cargo loads as heavy as 550 lbs. at speeds up to 25 mph. on roadways. (On pedestrian pathways and sidewalks, their speeds are capped at 12 mph.)

Pennsylvania is just the latest state to pass new laws regulating autonomous driving and flying technologies. Indeed, there are now a dozen states that allow delivery robots access to roads as well as pedestrian pathways.

A gita and its owner out for a stroll.

The new laws raise some interesting questions. Undeniably, delivery robots are a popular option for businesses and logistics companies; in a relatively short period of time their deployment has evolved well-past that of being merely a “novelty factor.” “The sidewalk is the new hot debated space that the aerial drones were maybe three or five years ago,” reports Greg Lynn, CEO of Piaggio Fast Forward, a robotics design firm that offers a suitcase-sized robot called gita that follows its owner around.

But deploying robots onto street- and sidewalk-grids that were mapped out decades ago – when there were no expectations of the sci-fi scenarios of autonomous vehicles – can be quite problematic from a safety standpoint.

Of course, we’ve faced this issue before – and not so very long ago – with the emergence of the Segway “people mover.” Those contraptions have caused more than a few problems (accidents and injuries) in urban centers around the world, leading some European center-cities to effectively ban their use — such as in Budapest and Barcelona.

And in the city of San Francisco – no technology backwater – delivery robots have been prohibited from operating on most city streets. Municipal leaders have cited potential safety concerns. Moreover, the National Association of City Transportation Officials (NACTO) has gone on record stating that robots “should be severely restricted, if not banned outright.”

One thing’s for sure: With the fast-growing phenomenon of delivery robots and other autonomous vehicles, the whole notion of “sharing the road” has taken on an additional dimension.

Do you have any interesting reports to share from what you may have encountered in your own town or region? Please share your observations with other readers.

Most people in business and politics have heard of the World Economic Forum (WEF), best known for holding its annual meeting for the world’s glitterati every January in Davos, Switzerland.

Most people in business and politics have heard of the World Economic Forum (WEF), best known for holding its annual meeting for the world’s glitterati every January in Davos, Switzerland.