Now that we’re down the road a good ways with the COVID-19 pandemic, it’s interesting and perhaps instructive to make a comparison between the current pandemic, and the 1918 H1N1 (influenza) pandemic, colloquially known as the “Spanish Flu,” that happened a little over a century ago.

There is no firm consensus on when the 1918 H1N1 pandemic actually began, but according to the U.S. Center for Disease Control and Prevention, it was first identified in U.S. military personnel in the spring of 1918 and ran its course for at least 44 weeks until May 1919, killing approximately 675,000 people in the United States.

In as much as the U.S. population was about 100 million at that time, the 1918 H1N1 pandemic’s death rate was about 6.4 per thousand people (0.6% of the population).

By contrast, the COVID-19 pandemic has been underway for 89 weeks (and counting) in the U.S., killing about 783,000 people here so far. The U.S. population had grown to about 330 million by 2020, so the COVID-19 death rate thus far is about 2.4 per thousand people (0.2% of the population).

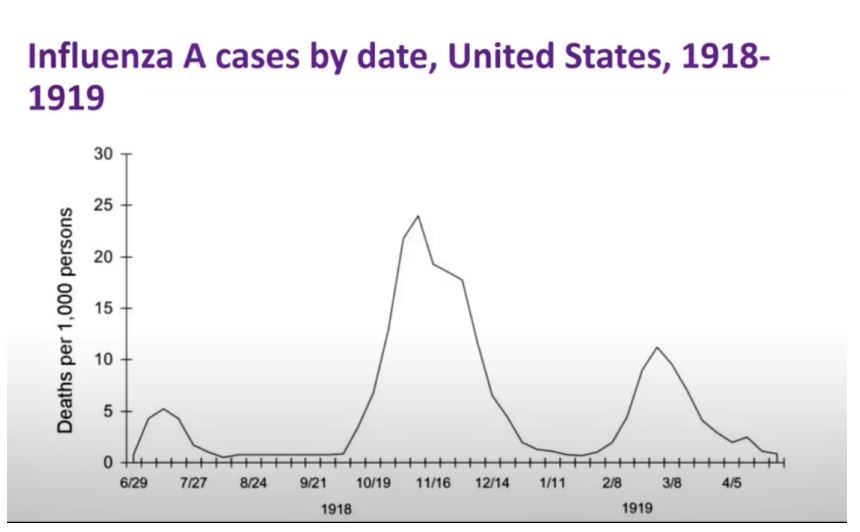

University of California – San Francisco epidemiologist George Rutherford has compiled a summary chart for the 1918 H1N1 pandemic in the U.S. According to the data, Spanish Flu’s first wave occurred in July 1918, followed by a second and far deadlier wave between October and December 1918 – and then a third less-deadly wave in February and March 1919, as depicted in Dr. Rutherford’s chart. At the peak of the second wave in November 1918, the U.S. experienced 24 deaths per thousand population per week.

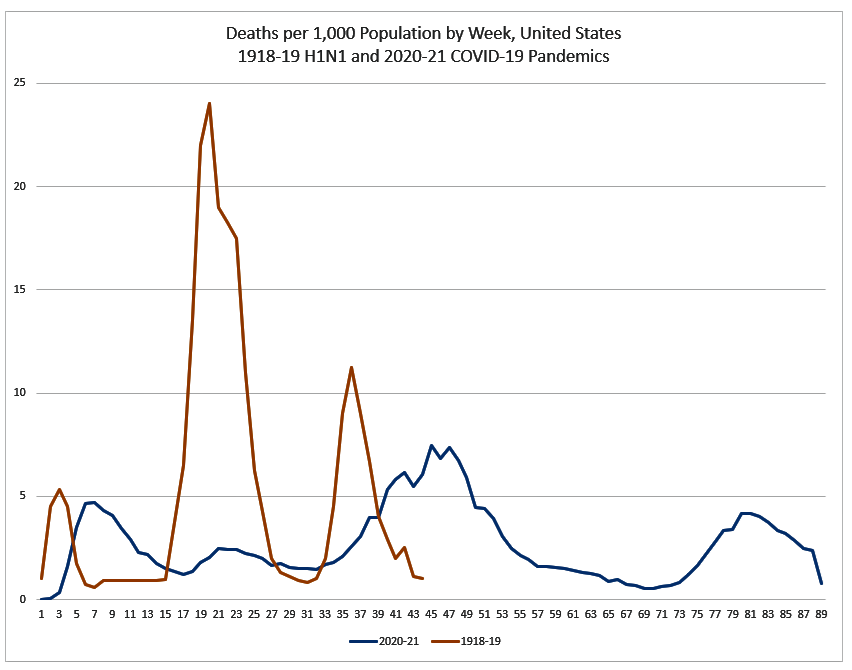

It’s interesting to see how this historical data compares to the COVID-19 pandemic, which began in the U.S. with a first wave between March and June 2020, followed by a smaller wave between July and September 2020. The largest and deadliest wave occurred between October 2020 and March 2021, when the weekly death rate peaked at 7 per thousand population. The fourth and most recent wave began in August 2021 until the present. You can view the weekly deaths per thousand population for both pandemics on this chart:

What’s clear is that, so far, the COVID-19 pandemic has lasted twice as long, while being one-third as deadly as the 1918 H1N1 pandemic.

This leads to an interesting insight. On the economic front, with comparatively little government regulation or monetary relief to citizens, the business cycle back in the early part of the 20th century tended to be shorter but much more volatile than it is today, exhibiting higher highs followed by lower lows.

Similarly, the degree of government regulation and involvement in matters of public health, including strong support for the rapid development of new vaccines, has been much greater during the COVID-19 pandemic than it ever was during the 1918 H1N1 pandemic.

It would seem that increased government involvement during economic and public health crises tends to moderate the ill effects — but at the cost of prolonging the misery.

The question is whether this connection is causation or coincidence. Please share your own thoughts in the comment section below.

(h/t Nelson Nones for researching and plotting the comparative stats.)

Researchers from the Harvard and Tilburg Business Schools think they’ve found a method to do just that.

One of the research techniques that has sprung up in the era of online engagement and interactivity is “mining” reader comments — then analyzing the granular data to discern their wider implications for companies and brands.

One way this happens is by analyzing the words that employees use to describe their own companies on review sites. Doing so can provide clues as to what’s going on inside these companies that others can’t discovers based on forward-facing reporting about the organizations in the business or news press.

Underscoring this point, a study conducted jointly by researchers at Harvard Business School and the Tilburg School of Economics and Management in The Netherlands has found that such information extracted from employee-review websites like Glassdoor.com is helpful in being able to predict potential misconduct beyond other observable factors such as a firm’s financial performance and industry risk analysis.

The correlating factors revolve around employee observations concerning the environments in which they work – factors like:

Company culture

Company operations

Control practices

Performance pressures

Negative or critical comments made within these broad categories contribute to weighing the risk for corporate misconduct. Business management professor Dennis Campbell of the Harvard Business School notes that the “tone at the bottom” revealed by such comments can be a good early-warning signal of potential misconduct.

“Our theory is that what leads people to commit misconduct is actually the environment they are in,” adds Ruidi Shang, the Tilburg professor heading up the research team.

The Harvard/Tilburg study sifted through information from anonymous reviews of publicly traded U.S. companies that had been posted on Glassdoor.com over a nine-year period between 2008 and 2017. Focusing on nearly 1,500 companies that had been the subject of ten or more review entries each over the period, by comparing keywords in the comments to actual corporate misconduct cases brought against public U.S. firms over the same period, direct correlations were found between the statements and the companies that were later found guilty of misconduct.

The researchers discovered that certain terms and phrases used by employees in their comments correlate highly to misconduct cases – terms like bureaucracy, compliance, favoritism, harassment, hostile and strict. Such terms came up disproportionately more frequently in the discussions and comments.

Of course, such analyses are rough measures at best. Because the researchers drew comparisons between the comments and the corporate misconduct based only on cases that the U.S. government pursued, the methodology would have missed misconduct wasn’t known (or pursued) by the government. But as for providing “directional indicators,” the methodology seems to be a valid approach. I think we could see it being employed by Wall Street analysts as part of efforts to predict threats to future financial performance – and other potential problems — based on what the granular data reveals.

More details on the study and its findings can be read in this report.

Looking around most every community, it doesn’t take long to realize just how many businesses are looking to hire workers. “Help Wanted” signs are everywhere, and various signing incentives are being offered to entice new employees as never before.

But in many cases the offers of employment are falling on pretty deaf ears. A recent survey of workers conducted by the Indeed employment website reveals that although many people are ostensibly in the market for new jobs, oftentimes the sense of urgency about landing a position simply isn’t there.

The Indeed survey was administered to ~5,000 Americans age 18 to 64 during the summer of 2021. The sample encompassed individuals in and out of the labor force.

The results of the survey revealed that many of the unemployed respondents don’t feel that they need to land a job right away — but they do express an interest in returning to work at some future point. The three main factors that appear to be holding people back from returning to work are these:

Concerns about the COVID-19 virus and its variants

Financial cushions, including employed spouses and the continued availability of enhanced unemployment insurance benefits

Care responsibilities at home — particularly involving school-age children

The net effect is that while many employers are making a major push to hire workers in order to take advantage of the reopened economy, many would-be employees simply don’t feel the same sense of urgency.

With the continuing questions surrounding the spread of Delta and other variants of COVID, what was once considered the near-certainty of a “return to normalcy” in the latter part of 2021 hasn’t quite turned out that way.

At this point, it would seem that the employment dynamics aren’t going to change dramatically until the unemployment compensation safety net reverts to its pre-pandemic structure … kids are back in school without the risk of future quarantines or class closures … and no new variants emerge that cause the number of COVID cases to spike again.

Considering what the past 18 months have been like, getting these three factors to neatly align may be a tall order.

For detailed survey results, you can access the Indeed research via this link.

Nearly everyone dislikes “office politics.” But does day-to-day employee gossip rise to that level? And have we lost something actually beneficial in the wake of remote work limiting our in-person interactions?

Ever since we were children, most of us have been conditioned to regard gossiping as a negative trait that any caring person should avoid doing.

At its core, the definition of the term is “people speaking evaluatively about someone who isn’t there.” But gossip can also relate to talking about rumors and conjecture regarding topics that go beyond just people.

Historically, gossip or the rumor mill in the office often served as a means by which anodyne-sounding corporate announcements would be subjected to a healthy degree of “whispered conversation and conjecture.” Or, as one DC-area employee put it in a recent Wall Street Journal article, ”You hear the surface story, and then you learn what the real story was – and that’s the gossip.”

In the months since mandatory office workplace lockdowns have been imposed, the gossip mill has fallen on hard times. Instead of serendipitous conversations happening in the lunchroom, in hallways or following group meetings, many workers are spending their days with just one person – themselves. Or they might be interfacing via Zoom meetings with the same handful of people from their core work team, where it’s always the same information being recycled among the same group of people.

Even for employees who have returned to working at their corporate offices, hybrid schedules often mean that there are far fewer daily interactions happening with other employees.

On one level, the reduction in gossiping may be reducing workplace “drama” and helping people focus better on their actual work tasks. Although the evidence is murky, productivity studies do appear to show an uptick in employee productivity since the onset of the COVID-19 pandemic.

On the other hand, in a recent survey of ~500 employees and business owners conducted by international legal consulting firm Seyfarth Shaw, the item that respondents missed the most after a year of remote working was “in-person and grown-up workplace conversations.”

For senior leadership, office gossip has been one way to rely on a kind of “early-warning system” about corporate initiatives or directives. In every office there seem to be a few people who have the pulse of the organization – it might be an executive assistant or some other staff support functionary – who other people feel comfortable confiding in and who in turn can communicate “the upshot” to the top brass. While difficult to quantify, that sort of dynamic really counts for something.

Of course, human nature being what it is, office gossip is never going to go away completely. But Skype or Zoom calls feel forced, and typing out thoughts or conjecture on IMs or e-mails is borderline-weird and feels inherently risky.

On balance, do you welcome the decline of face-to-face “gossip conversations” with colleagues — or do you suspect that a useful guerilla communications conduit has been lost? Please share your perspectives with other readers.

Just before the first lockdowns began in April 2020, fewer than 10% of the U.S. labor force worked remotely full-time. But barely a month later, around half of the labor was working remotely. And now, even after the slow easing of workplace restrictions that began to take effect in the summer of 2020, most of the workers who were working remotely have continued to do so.

The longer-term forecast is that perhaps 25% of the labor force will continue to work fully remote, even after life returns to “normal” in the post-COVID era.

For clues as to why the “new normal” will be so different from the “old” one, we can start with worker productivity data. Stanford University economist Nicholas Bloom has studied such productivity trends in the wake of the coronavirus and finds evidence that the productivity boost from remote work could be as high as 2.5%.

Sure, there may be more instances of personal work being done on company time, but counterbalancing that is the decline of commuting time, as well as the end of time-suck distractions that characterized daily life at the office.

As Florida and Ozimek explain further in their WSJ article:

“Major companies … have already announced that employees working from home may continue to do so permanently. They have embraced remote work not only because it saves them money on office space, but because it gives them greater access to talent, since they don’t have to relocate new hires.”

The shift to remote working severs the traditional connection between where people live and where they work. The impact of that change promises to be significant for quite a few cities, towns and regions. For smaller urban areas especially, they can now build their local economies based on remote workers and thus compete more easily against the big-city, high-tech coastal business centers that have dominated the employment landscape for so long.

Whereas metro areas like Boston, San Francisco, Washington DC and New York had become prohibitively expensive from a cost-of-living standpoint, today smaller metro areas such as Austin, Charlotte, Nashville and Denver are able to use their more attractive cost-of-living characteristics to attract newly mobile professionals who wish to keep more of their hard-earned incomes.

For smaller urban areas and regions such as Tulsa, OK, Bozeman, MT, Door County, WI and the Hudson Valley of New York it’s a similar scenario, as they become magnets for newly mobile workers whose work relies on digital tools, not physical location.

Pew Research has found that the number of people moving spiked in the months following the onset of the coronavirus pandemic – who suddenly were relocating at double the pre-pandemic rate. As for the reasons why, more than half of newly remote workers who are looking to relocate say that they would like a significantly less expensive house. The locational choices they have are far more numerous than before, because they can select a place that best meets their own personal or family needs without worrying about how much they can earn in the local business market.

For many cities and regions, economic development initiatives are likely to morph from luring companies with special tax incentives or other financial perks, and more towards luring a workforce through civic services and amenities: better schools, safer streets, and more parks and green spaces.

There’s no question that the “big city” will continue to hold attraction for certain segments of the populace. Younger workers without children will be drawn to the excitement and edginess of urban living without having to regard for things like quality schools. Those with a love for the arts will continue to value the kind of convenient access to museums, theatres and the symphony that only a large city can provide. And sports fanatics will never want to be too far away from attending the games of their favorite teams.

But for families with children, or for people who wish to have a less “city” environment, their options are broader than ever before. Those people will likely be attracted to small cities, high-end suburbs, exurban environments or rural regions that offer attractive amenities including recreation.

Getting the short end of the stick will be older suburbs or other run-of-the-mill localities with little to offer but tract housing – or anything else that’s even remotely “unique.”

They’re interesting future prospects we’re looking at – and on balance probably a good one for the country and our society as it’s enabling us to smooth out some of the stark regional disparities that had developed over the past several decades.

What are your thoughts on these trends? Please share your perspectives with other readers.

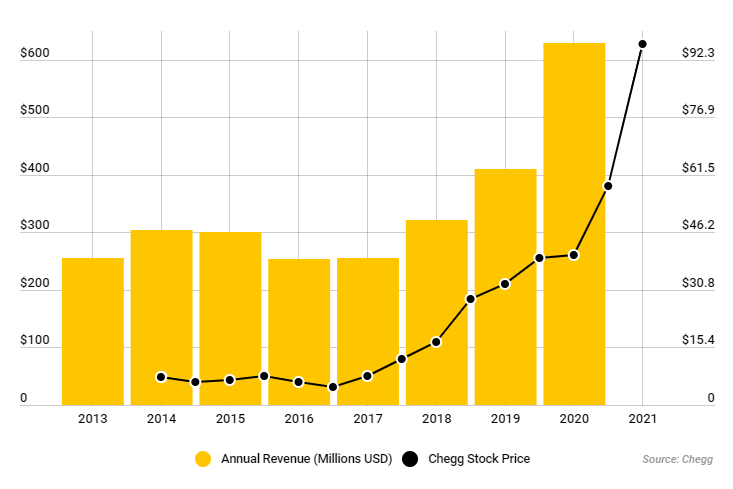

This past week, Forbes magazine published a feature article authored by its senior education editor, Susan Adams, concerning a $12 billion company that’s benefited mightily from the distance learning measures hastily put in place for secondary and college-level students in the wave of the coronavirus pandemic lockdowns.

The company in question is Chegg, an education technology firm which offers a $14.95 monthly subscription that provides a lifeline for students who are looking for answers to exam questions.

Headquartered in California, Chegg actually looks more like a company based in India, where it accesses a stable of more than 70,000 people with advanced science, math, engineering and IT degrees. These freelancers are available online continuously, supplying subscribers from around the world with step-by-step answers to their test-related questions. And the answers are typically provided in a matter of mere minutes.

Reportedly, Chegg’s database contains answers on some 46 million textbook and exam question topics, and it’s the driving force behind the company’s Chegg Study subscription service.

Of course everyone knows where the real action is …

Chegg Study is also the main revenue stream of the company — by far. Other services such as resources for improving writing and math skills as well as bibliography-creation software seem more like window-dressing.

It brings to mind certain video shops of yesteryear which would display a small selection of benign movie “standards” for sale at the front of the premises, fig-leafing the store’s true purpose.

The Forbes article interviewed more than 50 college students who are subscribers to Chegg Study. The students interviewed represent a cross-section of institutions ranging from small state schools to top private universities.

Nearly every one of the students interviewed admitted that they use Chegg Study to cheat on tests.

To view Chegg’s financial numbers is to notice a direct correlation between the onset of the COVID-19 pandemic — when education went virtual practically overnight — and a spike in revenue growth at the company. Quarterly revenues over 2019 have leapt 70% or more, and Chegg’s shares are up nearly 350% since the education lockdowns began in mid-March.

The company is now valued at a cool $12 billion.

Corporate spokespeople deny that Chegg is taking advantage of the current situation to juice its sales and profits. Company president Dan Rosensweig contends that Chegg is the equivalent of an “asynchronous, always-on tutor,” ready to help students with detailed answers to problems.

On-demand education, if you will. Or a student version of the GE Answer Center.

But the “new reality” of virtual education and Chegg’s role within it brings up a number of concerns. As cheating becomes easier to do and hence more prevalent (human nature being what it is), what happens to the value of a high school or college degree? Can degree credentials mean as much as they did before?

It depends. For some jobs where the ability to find accurate information quickly is important, finding someone who mastered the function of “chegging” while as a student might actually be the better candidate for the position. On the other hand, if the position requires a person who will uphold the highest ethical standards at all times, that same candidate would be the wrong one for the job.

Ultimately, it’s the students themselves who will likely be the victims long-term, because if they “skated on through” during their school years and didn’t actually learn the material, that will soon become evident when they go into the workforce. “Find out now … or find out later,” one might say.

Looking at the other side of the coin, how can schools make sure that they’re monitoring and mitigating cheating effectively, such that employers can be confident of the comparative value of a degree from one school versus that of another?

There are a variety of “remote proctoring” surveillance tools like Examity and Honorlock that can lock students’ web browsers and observe them visually through their laptop cameras. While on paper these look like effective (albeit costly) ways to crack down on online cheating, the degree of their actual success is debatable.

Some respondents in the Forbes student interviews reported that they “chegg” their online tests regardless of whether or not they’re being proctored, citing the belief that if they aren’t using the school’s own Wi-Fi connection, it’s impossible to detect the cheating activity.

Furthermore, anecdotal reports from teachers in my home state of Maryland state that on test-taking days, often there are large spikes in the number of students who mysteriously run into “problems” with their Zoom connections – and hence are unable to be observed while taking their tests.

But the issue goes even further – to the very heart of the notion of virtual learning itself and whether distance learning is ill-serving young people. Some students have found it hugely challenging to be skillful learners in the “virtual” world. A business colleague of mine shared one such example with me:

“Someone who I respect greatly and consider to be an honorable man has accepted his son’s cheating, since he went from being an ‘A’-student to failing because he couldn’t handle online learning. He was a visual and auditory learner and without those two things, the information wouldn’t stick.

The student and his dad talked about the 12 consecutive chapters he was supposed to be reading. When the father was satisfied with his son’s understanding of the material, he allowed his son to do whatever was necessary to get through the tests.”

When the situation gets to the point that students’ own parents are going along with the cheating, it means that we have an issue that goes way beyond one particular company that’s taking advantage of the dislocations in the educational arena while laughing all the way to the bank. At its root, the problem is virtual learning and the way it’s being structured.

Of course, the coronavirus crisis built quickly and took many colleges and school systems by surprise — so the fact that jury-rigged ways to deal with the virtual learning have fallen well-short expectations is completely understandable. But the shortcomings have become so glaringly obvious so quickly, new creative thinking is obviously needed – and fast.

If you have thoughts or ideas about steps the educational field could be taking to solve this dilemma, please share them with other readers here.

Nearly every business or organization, regardless of thee industry segment in which it operates, has been at least somewhat impacted by the coronavirus pandemic.

Existential forces have been responsible for quite a few businesses having to reduce staff working hours, either as a mandatory or voluntary measure. In a world of tough choices, often that action was the most reasonable way to cut costs while preventing redundancies and furloughs.

Months into the pandemic and with more restrictions being put in place again for the foreseeable future at least, what began as a short-term fix to weather the economic pressures of the COVID-19 outbreak now has some employers rethinking the possibilities of how they can restructure jobs to “work” effectively outside of the traditional work-week model.

In doing so, employers are responding to a growing appetite for part-time and flexible working as people re-evaluate their own work/life balance situations.

The economic benefits of allowing a higher proportion of staff to choose reduced hours on a more permanent basis could be beneficial for companies already operating on historically thin margins. While it’s too early to see widespread policy changes happening, some companies are already actively planning to offer more part-time and flexible work to meet the desires of those who no longer wish to work a traditional 8-hour day/40-hour work week.

Among the numerous repercussions of the “coronavirus economy,” one may be the growing realization that office employees actually can take back some control of their time – that they can still do good work while structuring their work days, weeks or months differently.

Any lingering stigma once associated with working fewer hours, working from home, or leaving the office early to pick up children has pretty much disappeared. Employees doing any of those things are no longer the exception – and hence there’s no longer the guilt associated with bending or breaking the rules of attendance at the office. And that’s before factoring in the economic attraction of saving thousands of dollars per year in commuting and other travel-related costs.

One chief marketing officer, Amanda Goetz of Teal Communications, goes so far so to declare that the 40-hour work week won’t exist in 10 years. “The way companies operate now, there’s no need to ‘own’ someone’s calendar as long as you know they have very clear metrics and can hit their goals,” this manager emphasizes.

What are your thoughts? How much will the recent changes be permanent going forward … or will we soon return to the paradigms of the pre-pandemic office world? Please share your perspectives with other readers here.

The Coronavirus pandemic has certainly made its mark on many markets and industries – some more than others, of course. But one consequence of the events of 2020 appears to cross all industry lines.

Because of the rapid adjustments organizations have been required to make in the way jobs are performed – borne out of necessity because of health fears, not to mention government edicts – workers have been forced to come up the digital learning curve in a big hurry in order to do their jobs properly.

This “digital upskilling” dynamic isn’t affecting only office workers. It’s happening across the board – in the private and public sector alike.

Simply put, digital upskilling isn’t a matter of choice. If workers want to remain relevant — and to keep their jobs — they’re having to ramp up their digital skill-sets without delay.

Moreover, the new skills aren’t limited to the efficient use of mobile devices, digital meeting/presentation functions, cloud applications and the like. According to LinkedIn’s recruitment data, highly in-demand skills over the past few months encompass wide-ranging and comprehensive knowledge sets such as data science, data storage, and tech support.

Not so long ago, there were “tech jobs” and “non-tech jobs.” Now there are just “jobs” – and nearly every one of them require the people doing them to possess a high comfort level with technology.

Will things revert back to older norms with the anticipated arrival of coronavirus vaccines in 2021? I think the chances of that are “less than zero.” But what are your thoughts? Please share your perspectives with other readers.

A new survey finds that nearly half of employees who are currently working from home want to keep it that way.

The forced shutdown of the American workplace began in mid-March. Only now, ten weeks later, are things beginning to open back up in a significant way.

But those ten weeks have revealed some interesting attitudinal changes on the part of many employees. Simply put, quite a few of them have concluded that they like working from home, and don’t much care to return to the “traditional” work routines.

It’s an interesting development that illustrates yet another manifestation of “the law of unintended consequences.” For decades, the opportunities to work from home seemed to be a realistic proposition for only a distinct minority of certain white-collar workers and top-level managers.

Reflecting this dynamic, prior to the Coronavirus outbreak just ~7% of the U.S. private sector workforce had access to a flexible workplace benefit, as reported in the 2019 National compensation Survey released by the Bureau of Labor Statistics.

Suddenly, working from home went from being a rarefied benefit to something quite routine in many work sectors.

In late April, The Grossman Group, a Chicago-based leadership and communications consulting firm, conducted an online survey of nearly 850 U.S. employees who are currently working from their homes. A cross-section of age, gender, geography, ethnicity and education levels were surveyed to ensure a reliable representation of the U.S. workforce.

The topline finding from the Grossman research is that nearly half of all workers surveyed (48%) reported that they would like to continue working from home after the COVID-19 pandemic passes.

The reasons for preferring work-from-home arrangements are varied. Certainly, the prospect of reduced commuting time is a major attraction, along with other work/life balance factors … and while some employees have found that setting up an office in their home isn’t a simple proposition, it’s also clear that many employees were able to adjust quickly during the early days of the workplace lockdown.

David Grossman, CEO of The Grossman Group, sees in the survey findings a clear message to employers: Worker preferences have evolved rapidly, necessitating a re-imagining of traditional ways of working. Grossman says:

“A great deal has changed in employees’ lives in a short time, and if we want them to be engaged and productive, we’re going to have to be willing to meet them where they are as much as possible … that’s a ‘win-win’ for companies and their people.”

He adds:

“Many employees have gotten a taste of working from home for the first time – and they like it.”

Interestingly, the Grossman Group survey found practically no generational differences in the attractiveness of a work-from-home option; whether you’re a Baby Boomer, a Gen X or Gen Z worker, the attitudes are nearly the same.

Of course, not every type of work is conducive to working remotely. Many jobs simply cannot be done without the benefit of a “destination workplace” where mission-critical machinery, equipment, laboratory and other facilities are accessed daily. But the COVID-19 lockdown experience has shown that employees can be productive no matter where they are, and a “one-size-fits-all” approach to the workplace likely won’t cut it in the future.

This might be a little difficult for some people to hear, but employers will have to set aside concerns about potential slackening employee motivation and productivity in a remote working environment, lest they lose their talent to other, more flexible employers who are figuring out ways to manage a remote workforce effectively over the long-term.

As David Grossman contends, “More flexibility adds value to the employee experience, builds engagement, and brings results.”

Additional findings from the Grossman Group research can be accessed here.

What are your thoughts on the topic, based on your own experiences and those of your co-workers over the past 10 weeks? Please share your opinions with other readers here.

One of the big repercussions of the Coronavirus scare has been to shift most companies into a world where significant numbers of their employees are working from home. Whereas working remotely might have been an occasional thing for many of these workers in the past, now it’s the daily reality.

What’s more, personal visits to customers and attendance at meetings or events have been severely curtailed.

This “new reality” may well be with us for the coming months – not merely weeks as some reporting has indicated. But more fundamentally, what does it mean for the long-term?

I think it’s very possible that we’re entering a new era of how companies work and interact with their customers that’s permanent more than it is temporary. The move towards working remotely had been advancing (slowly) over the years, but COVID-19 is the catalyst that will accelerate the trend.

Over the coming weeks, companies are going to become pretty adept at figuring out how to work successfully without the routine of in-person meetings. Moving even small meetings to virtual-only events is the short-term reality that’s going to turn into a long-term one.

When it comes to client service strategies, these new approaches will gain a secure foothold not just because they’re necessary in the current crisis, but because they’ll prove themselves to work well and to be more cost-efficient than the old ways of doing business. Along the same lines, professional conferences in every sector are being postponed or cancelled – or rolled into online-only events. This means that “big news” about product launches, market trends and data reporting are going to be communicated in ways that don’t involve a “big meeting.”

Social media and paid media will likely play larger roles in broadcasting the major announcements that are usually reserved for the year’s biggest meeting events. Harnessing techniques like animation, infographics and recorded presentations will happen much more than in the past, in order to turn information that used to be shared “in real life” into compelling and engaging web content.

The same dynamics are in play for formerly in-person sales visits. The “forced isolation” of social distancing will necessitate presentations and product demos being done via online meetings during the coming weeks and months. Once the COVID-19 pandemic subsides, in-person sales meetings at the customer’s place of business will return – but can we realistically expect that they will go back to the levels that they were before?

Likely not, as companies begin to realize that “we can do this” when it comes to conducting business effectively while communicating remotely. What may be lost in in-person meeting dynamics is more than made up for in the convenience and cost savings that “virtual” sales meetings can provide.

What do you think? Looking back, will we recognize the Coronavirus threat as the catalyst that changed the “business as usual” of how we conduct business meetings? Or will today’s “new normal” have returned to the “old normal” of life before the pandemic? Please share your thoughts with other readers here.

Now that we’re down the road a good ways with the COVID-19 pandemic, it’s interesting and perhaps instructive to make a comparison between the current pandemic, and the 1918 H1N1 (influenza) pandemic, colloquially known as the “Spanish Flu,” that happened a little over a century ago.

Now that we’re down the road a good ways with the COVID-19 pandemic, it’s interesting and perhaps instructive to make a comparison between the current pandemic, and the 1918 H1N1 (influenza) pandemic, colloquially known as the “Spanish Flu,” that happened a little over a century ago.