Researchers from the Harvard and Tilburg Business Schools think they’ve found a method to do just that.

One of the research techniques that has sprung up in the era of online engagement and interactivity is “mining” reader comments — then analyzing the granular data to discern their wider implications for companies and brands.

One way this happens is by analyzing the words that employees use to describe their own companies on review sites. Doing so can provide clues as to what’s going on inside these companies that others can’t discovers based on forward-facing reporting about the organizations in the business or news press.

Underscoring this point, a study conducted jointly by researchers at Harvard Business School and the Tilburg School of Economics and Management in The Netherlands has found that such information extracted from employee-review websites like Glassdoor.com is helpful in being able to predict potential misconduct beyond other observable factors such as a firm’s financial performance and industry risk analysis.

The correlating factors revolve around employee observations concerning the environments in which they work – factors like:

Company culture

Company operations

Control practices

Performance pressures

Negative or critical comments made within these broad categories contribute to weighing the risk for corporate misconduct. Business management professor Dennis Campbell of the Harvard Business School notes that the “tone at the bottom” revealed by such comments can be a good early-warning signal of potential misconduct.

“Our theory is that what leads people to commit misconduct is actually the environment they are in,” adds Ruidi Shang, the Tilburg professor heading up the research team.

The Harvard/Tilburg study sifted through information from anonymous reviews of publicly traded U.S. companies that had been posted on Glassdoor.com over a nine-year period between 2008 and 2017. Focusing on nearly 1,500 companies that had been the subject of ten or more review entries each over the period, by comparing keywords in the comments to actual corporate misconduct cases brought against public U.S. firms over the same period, direct correlations were found between the statements and the companies that were later found guilty of misconduct.

The researchers discovered that certain terms and phrases used by employees in their comments correlate highly to misconduct cases – terms like bureaucracy, compliance, favoritism, harassment, hostile and strict. Such terms came up disproportionately more frequently in the discussions and comments.

Of course, such analyses are rough measures at best. Because the researchers drew comparisons between the comments and the corporate misconduct based only on cases that the U.S. government pursued, the methodology would have missed misconduct wasn’t known (or pursued) by the government. But as for providing “directional indicators,” the methodology seems to be a valid approach. I think we could see it being employed by Wall Street analysts as part of efforts to predict threats to future financial performance – and other potential problems — based on what the granular data reveals.

More details on the study and its findings can be read in this report.

Looking around most every community, it doesn’t take long to realize just how many businesses are looking to hire workers. “Help Wanted” signs are everywhere, and various signing incentives are being offered to entice new employees as never before.

But in many cases the offers of employment are falling on pretty deaf ears. A recent survey of workers conducted by the Indeed employment website reveals that although many people are ostensibly in the market for new jobs, oftentimes the sense of urgency about landing a position simply isn’t there.

The Indeed survey was administered to ~5,000 Americans age 18 to 64 during the summer of 2021. The sample encompassed individuals in and out of the labor force.

The results of the survey revealed that many of the unemployed respondents don’t feel that they need to land a job right away — but they do express an interest in returning to work at some future point. The three main factors that appear to be holding people back from returning to work are these:

Concerns about the COVID-19 virus and its variants

Financial cushions, including employed spouses and the continued availability of enhanced unemployment insurance benefits

Care responsibilities at home — particularly involving school-age children

The net effect is that while many employers are making a major push to hire workers in order to take advantage of the reopened economy, many would-be employees simply don’t feel the same sense of urgency.

With the continuing questions surrounding the spread of Delta and other variants of COVID, what was once considered the near-certainty of a “return to normalcy” in the latter part of 2021 hasn’t quite turned out that way.

At this point, it would seem that the employment dynamics aren’t going to change dramatically until the unemployment compensation safety net reverts to its pre-pandemic structure … kids are back in school without the risk of future quarantines or class closures … and no new variants emerge that cause the number of COVID cases to spike again.

Considering what the past 18 months have been like, getting these three factors to neatly align may be a tall order.

For detailed survey results, you can access the Indeed research via this link.

There’s no question that search engines have made the process of gaining knowledge, and researching products and services, extremely easy — often nearly effortless. The search bots do the work for us, helping us find the answers we’re seeking in the blink of an eye.

So what’s not to love about search?

The thing about search engines is that the algorithms “reward” the purported wisdom of crowds – particularly since there’s more social interaction on websites than ever these days. It’s one thing for developers to optimize their websites for search – but there’s also the behaviors of those doing the searching and interacting with those same websites and pages.

Whether it’s tracking how much time visitors spend on a page as a proxy for relevance, or how visitors may interact with a page by rating products or services, the bots are continually refining the search results they serve up in an effort to deliver the highest degree of “relevance” to the greatest number of people.

But therein lies the rub. Popularity and algorithms drive search rankings. If people confine viewing of search results to just the first page – which is what so many viewers do — it limits their exposure to what might actually be more valuable information.

Over time, viewers have been “trained” to not to look beyond the first page of online results – and often not beyond the top five entries. That’s very convenient and time-efficient, but it means that better information, which is sometimes going to be found in the middle of search results rather than at the top, is completely missed.

As we rely more on ever-improving software, it’s tempting to assume that the search algorithms are going to be more and more airtight – and hence more effective than human-powered expertise.

But that isn’t the case – at least not yet. And a lot of things can slip through the gap that exists between the perception and the reality.

Text messaging has been with us for a long time now. It’s only natural that its popularity would grow in tandem with the increased adoption of smartphones.

But as late as 2019, field studies conducted by research companies like Lunar and Twilio showed that email communications continued to be the preferred way for consumers to receive communications from businesses or sales personnel.

Of course, both text and email had already eclipsed voicemail in popularity long ago – not to mention hanging on the phone for minutes (or hours) at a time to interface with companies in real-time.

Then COVID came along — and with it came stay-at-home orders from governments and employers. Its impact on consumer communications behavior was huge. New research reveals that the majority of people surveyed have increased their cellphone usage since the onset of the coronavirus – in most cases dramatically so.

In fact, nine out of ten consumers surveyed now report that they prefer receiving text communications over email when it comes to interfacing with businesses — and such text messages are also more likely to be read than email communications.

Moreover, consumers prefer texting with customer support reps more than real-time phone calls. They expect quick and accurate responses to their text inquiries — and don’t seem particularly concerned about the “digital paper trail” that might be less easy to document and preserve with text messaging than with email.

This shift in attitudes is actually pretty intuitive: Texting with customer support personnel allows anyone with a mobile device to get answers and resolve issues quickly, without enduring long hold times and transfers. The shorter resolution times that texting can deliver also encourage brand trust.

Chalk it up as yet another trend that was already happening — but COVID’s given it a big boost.

This past February I ordered an 18,000 BTU window air conditioning unit through the local GE dealer in the town where I live. It’s the largest such window unit you can buy, and there aren’t very many alternative options available from competitors.

Not surprisingly, the particular unit I ordered is manufactured in China (I am not aware of any similar models that are made in the United States). At the time I placed my order, I was informed that due to COVID-related disruptions of global deliveries, the earliest I could expect my unit to be received and installed was in April.

I wasn’t very surprised at this news, and figured that the delay would be perfectly fine for getting the AC unit installed and working in our home before the onset of the notoriously hot and humid summer months where we live here on Maryland’s Eastern Shore.

Since then, we’ve had several more pushbacks in the anticipated product delivery – first June … then August. And now the latest schedule I’m being told is for an October delivery – and even that date is “iffy.”

I think my situation isn’t unusual in these COVID-crazy times. Considering that the pandemic began towards the end of 2020, we are now 20 months later and the ripple effects are still being felt all throughout the global movement of products.

In fact, the recent coronavirus outbreaks that have occurred in Chinese port cities just this past month have caused even greater shipping delays than what had been encountered during 2020; they’re actually the worst shipping delays seen in 20 years. It means that the impacts will likely be felt all the way to the holiday shopping season at the end of this year — at a minimum.

Among the myriad of products and supplies that have been seriously affected are:

Appliances

Batteries

Food products

Furniture

Hospital, dental and surgical equipment/supplies

Measuring instruments

Plastic materials

Printed circuit boards

Semiconductor processing equipment

… and these are just some of the most notable examples.

With the Delta variant apparently causing a COVID-pandemic redux, it’s pretty impossible to gauge just how long it will take to work through the product shortages that have with us for so long already.

But what’s quite clear is that all of the initial estimates were woefully off the mark … so why would we expect anything different now?

What sort of product shortages have you experienced in the past few months, “thanks” to COVID – either in your business or at home? Please share your experiences (surprisingly good or unsurprisingly bad) with other readers here.

Remote work has turned each new hire into a national competition.

Historically, one of the challenges faced by smaller urban markets was their ability to hang on to talent. Younger workers often found it more financially lucrative following their education to relocate to major metropolitan areas in order to snag higher paying positions with the companies based there.

In time, however, the high cost of living in the large metro markets, coupled with the desire to ditch the unbearable congestion in those areas, led to the formation of new businesses outside the major tech centers that found it easier to compete with the major urban areas for talent.

Established companies found the same dynamics at work, too. The rise of markets like Charlotte, Salt Lake City, Pittsburgh and Boise underscored that the spread of the “new economy” had migrated to places beyond the traditional hubs of Boston, Washington, New York City, San Francisco/Silicon Valley, Los Angeles and others.

Then the COVID pandemic came along. Suddenly, it didn’t matter where employees lived as companies quickly figured out ways to have, in some cases, nearly their entire workforce working remotely.

It didn’t take long for employees in some of the market hardest-hit by COVID to flee to far-flung regions. New York City residents moved to the Hudson River Valley, South Florida and other locations. For California residents it was off to Nevada, Montana or Idaho. Boston-based workers decamped for Vermont or Maine.

It soon became apparent that for many tech jobs, the need to be clustered together in offices simply wasn’t that critical. And in an ironic twist, smaller-city startups and other firms are now starting to feel the effects of the establishment biggies poaching their own employees.

It’s particularly ironic; whereas before, companies that couldn’t compete with Silicon Valley heavyweights on salary could offer a whole lot of lifestyle to even the playing field. Now they’re finding that “work from anywhere” policies have nullified whatever advantages they had.

Those big-city salaries can be used to purchase a lot of house in whatever kind of environment desired — even if it’s a lakeside cabin in the middle of nowhere.

It also means that, all of a sudden, everyone’s competing with companies all over the country for talent — and hanging on to the existing talent is that much more difficult. When people are being offered 20% higher salary with no requirement to relocate, that’s a proposition many people are going to consider.

Another interesting consequence is that tech labor force is probably geographically more evenly distributed than it’s ever been — and the workers residing outside the traditional tech hubs are benefiting accordingly — At least in the short-term.

In the longer term, companies based in the smaller markets hope that they’ll have access to those same new tech migrants if work-from-home policies change yet again. But that’s a big “if” …

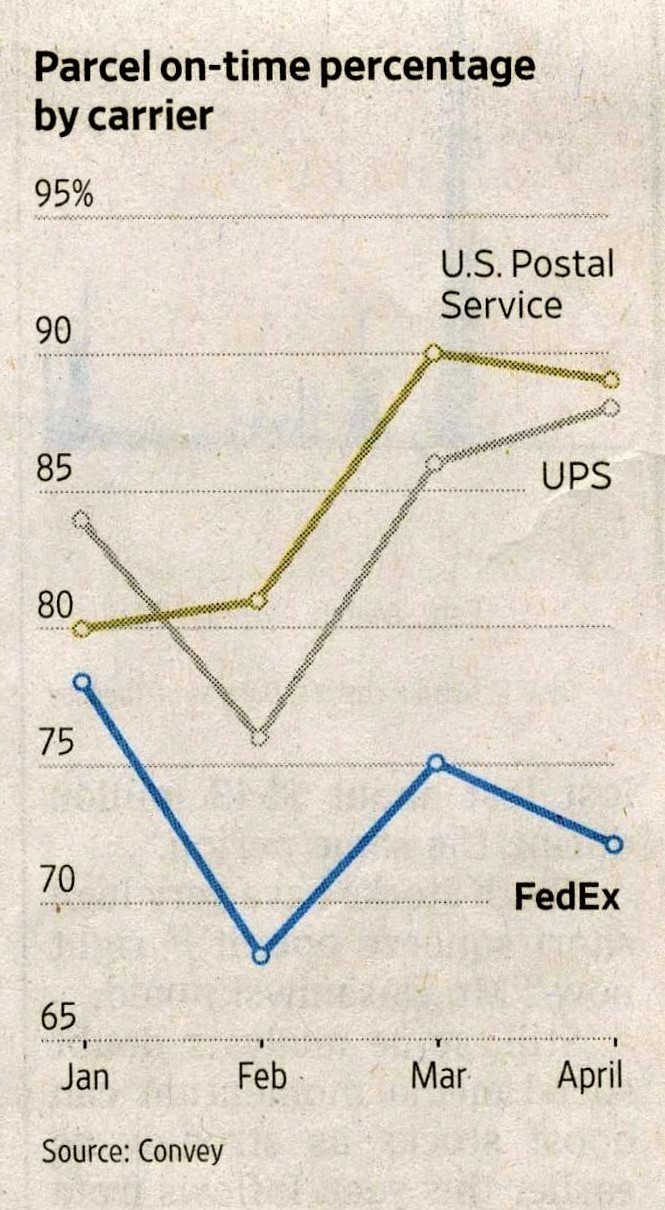

Recently, it’s fallen behind even the USPS in on-time delivery performance.

FedEx’s 2021 YTD delivery performance hasn’t exactly been stellar.

The pandemic-fueled increase of online product ordering hasn’t let up in recent months. And the tale it tells is FedEx struggling to keep up with its rivals when it comes to on-time parcel deliveries.

The most recent statistics covering March through mid-April show a significant difference in delivery performance – 87% on-time deliveries for FedEx Ground shipments compared to 95% in the case of UPS. Those figures come from ShipMatrix, Inc., a company that tracks shipping and delivery performance.

According to The Wall Street Journal, the comparatively weak performance by FedEx elicited this anodyne statement from a company spokesperson:

“FedEx continues to experience a peak-like surge in package volume due to the explosive growth of e-commerce. As always, we are working closely with our customers to manage their volume and identify opportunities to help ensure the best possible service.”

… As if the other delivery companies aren’t facing the same dynamics regarding the growth in online ordering volume.

Delivery tracking software company Convey has released figures that are even more problematic for FedEx. In April, only around 70% of FedEx shipments were on-time, which means the company’s performance was weaker than UPS and even the U.S. Postal Service.

In response, FedEx claims that Convey’s data haven’t aligned with its own internal stats, but the company hasn’t released figures of its own to illustrate the difference.

At the same time, FedEx reports that it’s doubling down on plans to increase its network capacity, along with recruiting additional workers. Even so, it acknowledges that FedEx Ground capacity will continue to be constrained until the end of 2021.

Up to now, the unimpressive record on parcel deliveries hasn’t appeared to hurt FedEx’s financials, which recently hit their highest-ever monthly revenue and operating profit levels. The question is, can that performance hold long-term if businesses and their customers continue to experience slower deliveries? It isn’t as if there aren’t alternative suppliers in the parcel delivery business.

Have you experienced issues with FedEx’s delivery performance recently? If so, are they significant enough to make you open to considering alternative shippers? Please share your thoughts with other readers here.

Responses from two people in particular are worth highlighting for the “countervailing views” that they espouse. I think both have merit.

The first response came from my brother, Nelson Nones, who has lived and worked outside the United States for decades. His perspectives are interesting because, while fully understanding domestic events and policies, he also brings an international orientation to the discussion due to his own personal circumstances. Nelson is looking to history for his perspectives on the inflation issue, offering these comments:

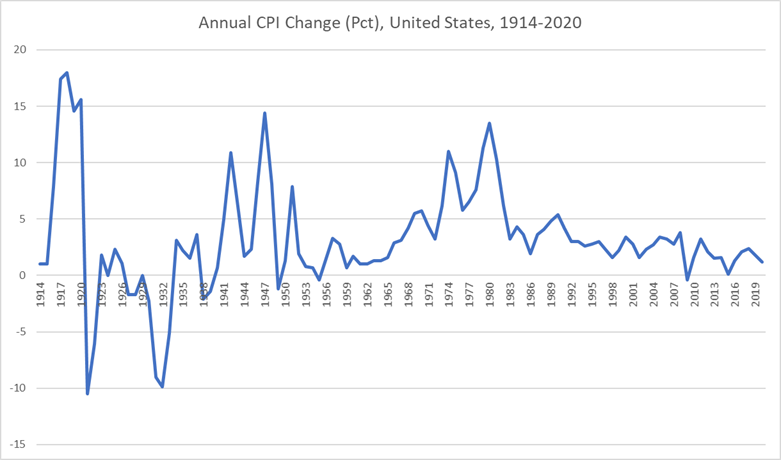

The chart below shows annual U.S. CPI percentage change for the past 106 years:

Projecting the latest (April 2021) Consumer Price Index forward to an entire year suggests that the U.S. will experience a 3.1% inflation rate in 2021. That would be higher than in any year since 2011, which was a bounce-back year following the Great Recession. Otherwise, the generic inflation trend has been consistently down since 1982 (nearly 40 years).

If the historical trends are any guide, and if we are indeed entering a persistent inflationary phase, it would take another decade before inflation growth approaches the levels seen during the 1970s.

But I think the likeliest scenario is experiencing a sharp uptick this year due to pent-up demand following the COVID-19 pandemic that will causie spot shortages, followed by resumption of a downward trend over the following ten years or so.

That’s similar to the pattern you can observe in the chart [above] during the years following the end of World War II, which had also created massive pent-up consumer demand.

Consider that the coronavirus pandemic hasn’t really altered the underlying economic fundamentals. The past 40 years has witnessed an explosion of manufacturing capacity in China and other developing countries, and that hasn’t gone away. Meanwhile, dependency on oil — a key driver of inflation in the 1970s — has shrunk due to improved energy efficiency and aggressive exploitation of renewable energy resources, which for all practical purposes are in infinite supply.

Another factor, which doesn’t get as much attention as it probably should, is declining birth rates and aging of the population on a global scale, leading to a slower rate of population growth in the future that may constrain demand for consumer products in comparison to the past century. Let’s face it — we old farts just don’t consume as much as growing families do!

So yes, we should keep an eye on inflation — but I don’t think we’re in for a repeat performance of the horrible 1970s.

Echoing Nelson’s thoughts are the perspectives of another business veteran — an editor and publisher who has been intimately involved in the commercial/B-to-B field for decades. Here is what he wrote to me:

I don’t want to get into a public debate with the inflationistas because I will never convince them that this is likely not a replay of the 1970s and early 80s inflationary period pre-[Paul] Volcker. (Speaking personally, I didn’t own a house until I was 42 for the very reasons you cited in your blog post, and I was just a lowly editor back then.)

What we’re seeing today is simply the price shock of suddenly soaring demand, aggravated in the case of some commodities such as steel by Trump-era tariffs.

All commodities are tied to the price of crude oil, the most volatile of all commodities, which is long-denominated in U.S. dollars. WTI crude pricing is now at around $63 per bbl. — about where it was in early 2020 before the pandemic hit. It went negative for a time during the worst period of the crash in worldwide demand that was brought about by the pandemic. Tanks couldn’t be found into which to put the excess crude coming out of the ground from U.S. fracking. Traders freaked out, as they sometimes do.

So naturally, the percentage changes today look jaw-dropping. I can go through all the other commodities mentioned in your post and provide simple explanations as to why each is currently on the rise. Logistical bottlenecks are a big problem with everything — but as with oil, most of the issue is the sudden surge in demand as the pandemic winds down even as production and logistics aren’t yet prepared to fulfill the need.

In other words, the situation has very little to do with government spending — especially since most of the infrastructure money isn’t even allocated, let alone spent. Also, the Biden administration has yet to raise a single tax. It can’t. Only the House Ways and Means Committee can initiate tax changes, and those must then go through the Senate to become law. Senate Minority Leader McConnell and his allies have made sure nothing has gotten through.

Of course, it never hurts to keep an eye on things — especially with structural inflation as you noted in your article. But it’s important to look also at other, broader data. The Producer Price Index in April did reflect the increase in commodities prices, but the Consumer Price Index, even though it had a month of robust increases, remains below 3% annualized. And the Personal Consumption Expenditure Price Index, which is what the Fed pays attention to the most, is still tracking under 2% on an annualized basis. (A little inflation can be a good thing, actually.)

On the income side, average wage rates aren’t rising; they’re more likely to be falling in the future as low-wage service workers, including those in foodservice, re-enter the market.

So in my view the things people see with inflation are most likely short-term issues. Let’s look at it again in six months to a year. I’d also suggest that people read economist Paul Krugman’s columns in the New York Times for a bit of perspective that’s counter to the views of the inflationistas, if only for balance. The monetarists have been wrong since Volcker squeezed out the inflationary spiral. It was painful, though — so we’ll want to keep an eye on things.

Considering the views put forward above, I think it’s fair to conclude that “the jury’s out” on whether we’re actually entering a prolonged inflationary period. If you have additional thoughts or perspectives to share on either side of the issue, I’m sure other readers would be interested to hear them. Feel free to leave a comment below.

The rise in lumber prices has received a certain degree of coverage in the news in recent weeks and months. For anyone who used the “pandemic period” to engage in home remodeling or renovation projects – perhaps moving away from “open concept everything” to reintroduce the designated spaces of yesteryear – the eye-popping price of lumber has come as something of a shock.

As for explaining the sharp increase, it’s logical to think that prices are directly correlated to the increased demand for the product. But this explanation is incomplete; the steep price rise in a wide range of commodities well beyond just lumber tells us that inflation isn’t relegated to just a few high-demand product categories. It’s the closest thing to “across the board” that we’ve seen in over 40 years — and the issue seemed to come out of nowhere.

Price inflation has been such a non-factor for so many decades, most consumers don’t even have personal memories of it. But those of us “of a certain age” remember well how difficult it was to navigate an “inflation-everywhere” environment where annual salary increases could never keep pace with rising prices.

It was difficult on people with fixed incomes, of course, but perhaps worse for young consumers who found that struggling to save for a down payment on a house purchase was a losing proposition as the gap widened rather than narrowed year over year. Living like a monk while scrimping and saving for a house gets old when you realize that your efforts aren’t getting you anywhere near where you’re attempting to go …

As for the situation now, the inflation warning signs are all around us if we dare to look. According to a report published in the May 21, 2021 issue of The Wall Street Journal, lumber may exhibit the most visible spike in prices, but consider what futures prices are showing for a whole range of commodities when compared to just one year ago:

Gold: +7%

Platinum: +29%

Wheat: +31%

Cotton: +40%

Coffee: +42%

Sugar: +52%

Silver: +56%

Natural gas: +65%

Soybeans: +81%

Crude oil: +85%

Cooper: +86%

Gasoline: +96%

Corn: +108%

Lumber: +278%

It doesn’t take a degree in economics to know that these sorts of trends are pretty alarming. Whenever it has an opportunity to take hold, inflation is one of the most insidious of economic problems – and one that’s extremely difficult to reverse. Inflation is also very debilitating for the personal budgets of the large majority of consumers, and it causes the most harm to those on the lower rungs of the economic ladder.

The next few months will tell us if this particular inflation is going to be a temporary phenomenon or not. How much of the commodity price increases are attributable to transitory events that will ease as the world’s economies move further from lockdown?

But if this inflation turns out to be something more structural or more directly correlated to the massive increase in government spending paid for by the expanded money supply, expect the economic (and political) climate to begin to look vastly different in the coming months.

Inflation will be uncharted territory for most people. But a few of us veterans will be around to provide context and counsel — and perhaps engage in a bit of “Sister Toldja” commentary while we’re at it …

Corporate promotional products and branded swag have been a big part of business for decades. The Advertising Specialty Institute reports that in 2019, promo products expenditures in North America amounted to nearly $26 billion, amazing as that figure might seem.

But that was before the coronavirus pandemic hit, shutting down trade shows and forcing the cancellation of events (or migrating them online). All of a sudden, demand for branded tchotchkes, hats, t-shirts, tote bags and the like pretty much disappeared.

However, just because corporate swag fell off the radar screen in 2020 doesn’t mean that corporate freebies for customers and prospects are a thing of the past. But COVID seems to have changed how some marketers feel about these items — and given them reason to rethink how branded merchandise can do a better job of actually nurturing customer relationships.

Because of this introspection, the days of ubiquitous, unlimited “homogenous” corporate swag may well be numbered — and that wouldn’t be such a bad thing. For those of us who have participated in industry trade shows, corporate events and the like over the years, when you consider how much stuff is given out to people who promptly discard the items because they aren’t something they either needed or wanted to have, coming up with a different approach was bound to fall on fertile ground.

Enter “gifting-as-a-service” firms. Several of these such as Snappy App, Kitchen Stadium and Alyce have sprung up in recent times. They operate under business models that are as simple as they are elegant. Think of them as “choose your own swag” concepts wherein recipients are given the opportunity to pick which items they prefer – and in some cases the size and color, too. Then those items are shipped directly to the recipient’s home or office.

Being given a card to check off their item of choice it may not pack the same impact as being given the item right there on the spot, but it actually makes life easier for everyone. No longer does a trade show attendee have to lug the item around the exhibit floor and back to his or her hotel room — nor pack it for the flight home. The exhibitor doesn’t need to ship swag merchandise to the show – hoping that the quantity shipped isn’t substantially higher or lower than the number of items actually needed.

Such “gifting-as-a-service” programs provide a better experience for recipients, too, because people can select something they actually want from among a selection of items. And for companies, it could actually turn out to be less costly in the end because they wouldn’t need to be pay for gift items that aren’t redeemed.

Such programs are versatile enough to work across all types of activities – including online as well as in-person events. They can also be offered as rewards to loyal customers completely apart from any particular show or event.

One final plus – or at least a hope – is that less swag will end up in the trash before it’s even had the chance to be worn or used. In a world where there’s increasing focus on environmental sustainability, that has to count for something, too.

One of the research techniques that has sprung up in the era of online engagement and interactivity is “mining” reader comments — then analyzing the granular data to discern their wider implications for companies and brands.

One of the research techniques that has sprung up in the era of online engagement and interactivity is “mining” reader comments — then analyzing the granular data to discern their wider implications for companies and brands. The Harvard/Tilburg study sifted through information from anonymous reviews of publicly traded U.S. companies that had been posted on Glassdoor.com over a nine-year period between 2008 and 2017. Focusing on nearly 1,500 companies that had been the subject of ten or more review entries each over the period, by comparing keywords in the comments to actual corporate misconduct cases brought against public U.S. firms over the same period, direct correlations were found between the statements and the companies that were later found guilty of misconduct.

The Harvard/Tilburg study sifted through information from anonymous reviews of publicly traded U.S. companies that had been posted on Glassdoor.com over a nine-year period between 2008 and 2017. Focusing on nearly 1,500 companies that had been the subject of ten or more review entries each over the period, by comparing keywords in the comments to actual corporate misconduct cases brought against public U.S. firms over the same period, direct correlations were found between the statements and the companies that were later found guilty of misconduct.