Millions of Americans age 20 to 24 fall into the NEET category: “Not in Employment, Education or Training.”

The COVID-19 pandemic has exposed some interesting fault-lines in the socio-economic fabric of the United States. One of these relates to young adults — those between the ages of 20 and 25. What we find paints a potentially disturbing picture of an economic and employment situation that may not be easily fixable.

A recently issued economic report published by the Center for Economic and Policy Research (CEPR) focuses on the so-called “NEET rate“– young Americans who are not employed, not in school, and not in training.

As of the First Quarter of 2021, the NEET category represented nearly 4 million Americans between the ages of 20 and 24. This eye-popping statistic goes well beyond the particular circumstances of the pandemic and may turn out to be an economically devastating trend with a myriad of adverse ripple effects related to it.

Look at any business newspaper or website these days and you’ll see reports regularly about worker shortages across many sectors — including unfilled jobs at the lower end of the pay scale which offer employment opportunities that fit well with the capabilities of lower skilled workers newly coming into the workplace.

At this moment, pretty much anyone who is willing to look around can easily find employment, schooling, or training of various kinds. But for millions of Americans in the 20-24 age cohort, the job opportunities appear to be falling on deaf ears. Bloomberg/Quint‘s reaction to the CEPT study certainly hits home:

“Inactive youth is a worrying sign for the future of the [U.S.] economy, as they don’t gain critical job skills to help realize their future earnings potential. Further, high NEET rates may foster environments that are fertile for social unrest.”

… Daily urban strife in Portland, Minneapolis and Seattle, anyone?

It doesn’t much help that younger Americans appear to be less enamored with the basic economic foundations of the country than are their older compatriots. A recent poll by Axios/Momentive has found that while nearly 60% of Americans hold positive views of capitalism, those sentiments are share by a only little more than 40% of those in the 18-24 age category.

Moreover, more than 50% of the younger group view socialism positively compared to only around 40% of all Americans that feel the same way.

The coronavirus pandemic may have laid bare these trends, but it would be foolish to think that the issues weren’t percolating well before the first U.S. businesses began to lock down in March 2020.

And more fundamentally, one could question just how much government can do to reverse the trend; perhaps the best thing to do is to stop “helping” so much … ?

More information about the CEPR report can be viewed here. What are your thoughts on this issue? Please share your views with other readers here.

One of the lessons that the COVID-19 pandemic has taught us is that the advent of an unexpected medical danger can have ripple effects that go well-beyond just the specific health matters at hand.

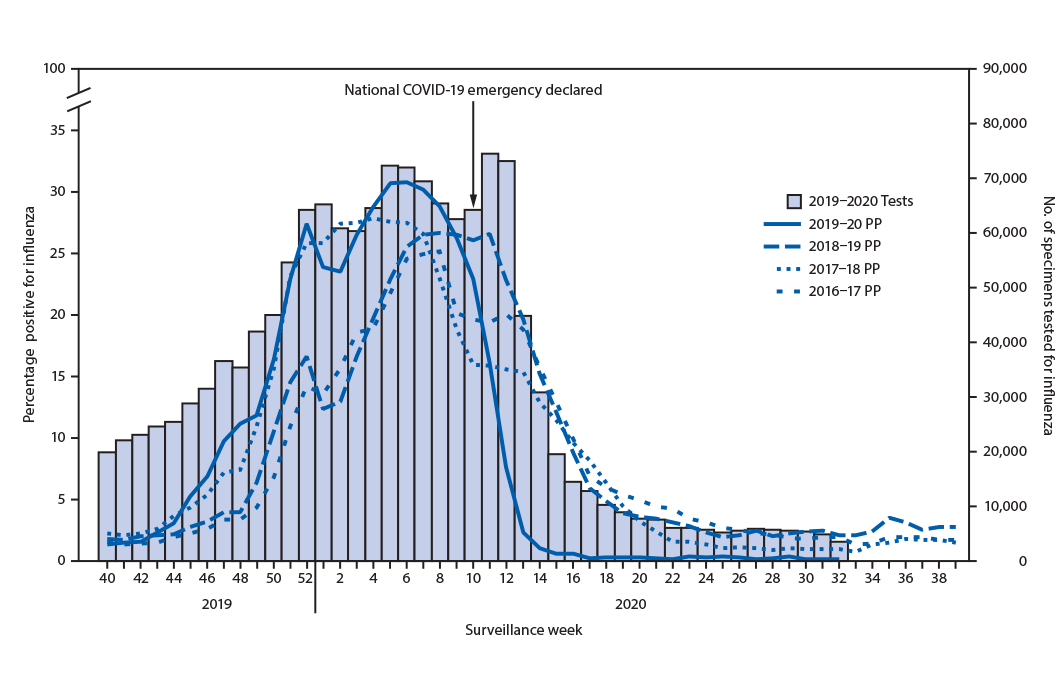

One that has been well-covered in the news is how the precautions most people are taking to avoid contracting the coronavirus are driving flu cases down to levels never before seen. This chart pretty much says it all:But as it turns out, there are some other, perhaps more unanticipated consequences — ones that have positive and negative aspects.

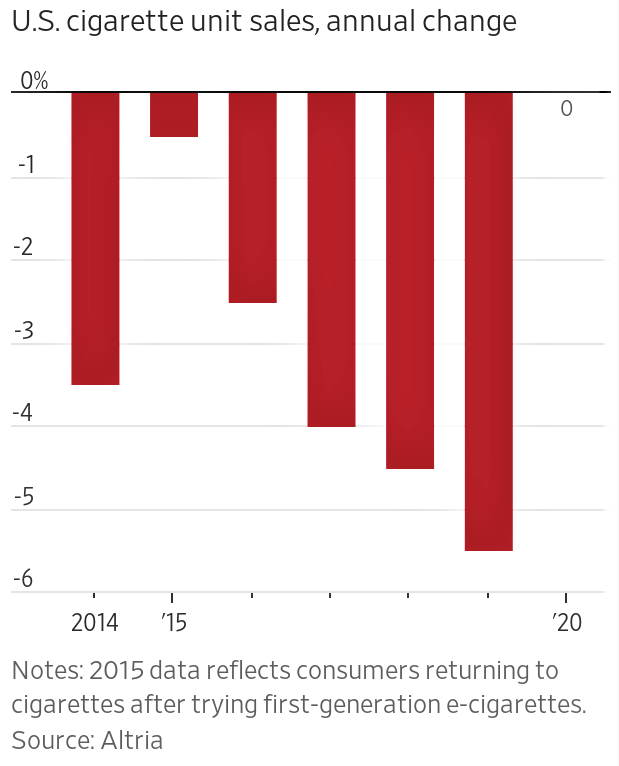

We’re reminded of this in the form of several newly published reports. One report comes from Altria, the largest U.S. producer of tobacco products. According to Altria, the onset of the COVID-19 pandemic appears to be responsible — at least in part — to halting a decades-long steady decline in cigarette usage among Americans.

While the trend hasn’t actually gone in reverse, Altria does report that in 2020, the cigarette industry’s unit sales in the U.S. were flat as compared to 2019.

That’s a big shift from the 5.5% annual decline in usage that was observed between 2018 and 2019.

As for the reasons behind such a sudden shift in consumer behavior, the Altria report touches on several probable factors, including:

People had more opportunities to smoke because of spending more time at home rather than the office.

More disposable income available for smokes because of less money being spent on commuting, travel and entertainment expenses.

The heretofore-robust growth of substitute products (e-cigarettes) was reversed in response to reports about unexplained lung illnesses among e-cigarette users, the ban on flavored vaping products, plus increased taxes on e-cigarette products.

A more acute sense of personal stress and anxiety in the wake of the coronavirus pandemic.

The newest trends in cigarette usage can’t be good for seeing a return to the decline in death rates that are tied to smoking. Unfortunately, those rates remain high: The effects of smoking account for more than 480,000 deaths in the United States each year.

On the other hand, there are positive ripple effects related to the coronavirus pandemic, too. As it turns out, the medical innovations that have been part of the worldwide response to the pandemic are delivering parallel positive benefits in the broader war on cancer.

One piece of evidence is the success of newly developed mRNA vaccines for combating the COVID-19 virus. Those same vaccines are now being repurposed to battle various forms of cancerous tumors.

Naturally, any such development on the cancer treatment front won’t be a quick “silver bullet” solution in the decades-long battle to defeat cancer. But a report released in January 2021 by the American Cancer Society points to the promising success that such new initiatives are having.

The key stats are telling: American cancer death rates have dropped steadily since 1991 – with an overall decrease of ~31% in the death rate through 2018 that was capped by a one-year decline of ~2.5% observed in 2017-18 alone.

The ACS report summarizes:

“An estimated 3.2 million cancer deaths have been averted from 1991 through 2018 due to reductions in smoking, earlier [cancer] detection, and improvements in treatment, which are reflected in long-term declines in mortality for the four leading cancers: lung, breast, colorectal and prostate.”

Not surprisingly, lung cancer is the biggest driver of the death rate decline. Whereas a dozen years ago the overall survival rate for non-small cell lung cancer was just 34%, in 2015 it was 42% (and it’s higher today).

Looking forward, even as we eagerly anticipated the large-scale rollout of COVID-19 vaccinations which can’t come soon enough, we can also be happy in the hope that the emerging science will deliver a parallel positive impact on cancer treatments – so long as we can convince people not to regress in their smoking habits.

What lifestyle adjustments – positive or negative – have you or people you know made over the past year? Beyond the risks of the coronavirus itself, what other new health challenges have you or they faced in its wake? Please share your perspectives with other readers here.

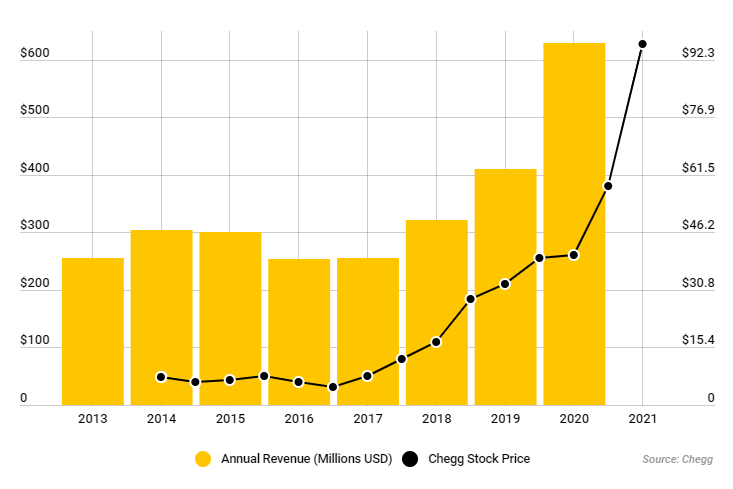

This past week, Forbes magazine published a feature article authored by its senior education editor, Susan Adams, concerning a $12 billion company that’s benefited mightily from the distance learning measures hastily put in place for secondary and college-level students in the wave of the coronavirus pandemic lockdowns.

The company in question is Chegg, an education technology firm which offers a $14.95 monthly subscription that provides a lifeline for students who are looking for answers to exam questions.

Headquartered in California, Chegg actually looks more like a company based in India, where it accesses a stable of more than 70,000 people with advanced science, math, engineering and IT degrees. These freelancers are available online continuously, supplying subscribers from around the world with step-by-step answers to their test-related questions. And the answers are typically provided in a matter of mere minutes.

Reportedly, Chegg’s database contains answers on some 46 million textbook and exam question topics, and it’s the driving force behind the company’s Chegg Study subscription service.

Of course everyone knows where the real action is …

Chegg Study is also the main revenue stream of the company — by far. Other services such as resources for improving writing and math skills as well as bibliography-creation software seem more like window-dressing.

It brings to mind certain video shops of yesteryear which would display a small selection of benign movie “standards” for sale at the front of the premises, fig-leafing the store’s true purpose.

The Forbes article interviewed more than 50 college students who are subscribers to Chegg Study. The students interviewed represent a cross-section of institutions ranging from small state schools to top private universities.

Nearly every one of the students interviewed admitted that they use Chegg Study to cheat on tests.

To view Chegg’s financial numbers is to notice a direct correlation between the onset of the COVID-19 pandemic — when education went virtual practically overnight — and a spike in revenue growth at the company. Quarterly revenues over 2019 have leapt 70% or more, and Chegg’s shares are up nearly 350% since the education lockdowns began in mid-March.

The company is now valued at a cool $12 billion.

Corporate spokespeople deny that Chegg is taking advantage of the current situation to juice its sales and profits. Company president Dan Rosensweig contends that Chegg is the equivalent of an “asynchronous, always-on tutor,” ready to help students with detailed answers to problems.

On-demand education, if you will. Or a student version of the GE Answer Center.

But the “new reality” of virtual education and Chegg’s role within it brings up a number of concerns. As cheating becomes easier to do and hence more prevalent (human nature being what it is), what happens to the value of a high school or college degree? Can degree credentials mean as much as they did before?

It depends. For some jobs where the ability to find accurate information quickly is important, finding someone who mastered the function of “chegging” while as a student might actually be the better candidate for the position. On the other hand, if the position requires a person who will uphold the highest ethical standards at all times, that same candidate would be the wrong one for the job.

Ultimately, it’s the students themselves who will likely be the victims long-term, because if they “skated on through” during their school years and didn’t actually learn the material, that will soon become evident when they go into the workforce. “Find out now … or find out later,” one might say.

Looking at the other side of the coin, how can schools make sure that they’re monitoring and mitigating cheating effectively, such that employers can be confident of the comparative value of a degree from one school versus that of another?

There are a variety of “remote proctoring” surveillance tools like Examity and Honorlock that can lock students’ web browsers and observe them visually through their laptop cameras. While on paper these look like effective (albeit costly) ways to crack down on online cheating, the degree of their actual success is debatable.

Some respondents in the Forbes student interviews reported that they “chegg” their online tests regardless of whether or not they’re being proctored, citing the belief that if they aren’t using the school’s own Wi-Fi connection, it’s impossible to detect the cheating activity.

Furthermore, anecdotal reports from teachers in my home state of Maryland state that on test-taking days, often there are large spikes in the number of students who mysteriously run into “problems” with their Zoom connections – and hence are unable to be observed while taking their tests.

But the issue goes even further – to the very heart of the notion of virtual learning itself and whether distance learning is ill-serving young people. Some students have found it hugely challenging to be skillful learners in the “virtual” world. A business colleague of mine shared one such example with me:

“Someone who I respect greatly and consider to be an honorable man has accepted his son’s cheating, since he went from being an ‘A’-student to failing because he couldn’t handle online learning. He was a visual and auditory learner and without those two things, the information wouldn’t stick.

The student and his dad talked about the 12 consecutive chapters he was supposed to be reading. When the father was satisfied with his son’s understanding of the material, he allowed his son to do whatever was necessary to get through the tests.”

When the situation gets to the point that students’ own parents are going along with the cheating, it means that we have an issue that goes way beyond one particular company that’s taking advantage of the dislocations in the educational arena while laughing all the way to the bank. At its root, the problem is virtual learning and the way it’s being structured.

Of course, the coronavirus crisis built quickly and took many colleges and school systems by surprise — so the fact that jury-rigged ways to deal with the virtual learning have fallen well-short expectations is completely understandable. But the shortcomings have become so glaringly obvious so quickly, new creative thinking is obviously needed – and fast.

If you have thoughts or ideas about steps the educational field could be taking to solve this dilemma, please share them with other readers here.

For those of us in marketing and sales – particularly involved in the commercial market segments – the COVID-19 pandemic brought the function of trade show marketing to a screeching halt, as one event after another in 2020 was either canceled outright or “re-imagined” as a digital-only program.

The impact on the convention business has been severe — and it’s had ripple effects throughout the wider market as well. As Tori Barnes, head of public affairs and policy at the U.S. Travel Association, has noted:

“When a large convention or event is happening, the entire city is involved. Whole downtowns have been revitalized due to the meeting and events business, and they’ve really struggled this past year.”

But now that COVID vaccines have been approved and are beginning to be distributed, the question is, “What’s the road back for trade shows?” Will they return to the “old normal,” or are they forever changed?

Those issues were studied recently by the Center for Exhibition Industry Research (CEIR), which posed a group of questions to ~350 executives of exhibition-organizing companies. The results of the CEIR research suggest that the future of trade shows will likely be a hybrid model of digital and in-person event activities — often as part of the same program.

According to the CEIR findings, “education” was the biggest driver of virtual events run during 2020 – and by a big margin. When asked to cite the most important reason organizers think that professionals attended their virtual events, the top three responses were:

Education for professional or personal development: ~33%

To keep up-to-date with industry trends: ~11%

To fulfill professional certification requirements: ~10%

Collectively representing ~54% of the responses, it would seem that all three of these reasons lend themselves equally well to digital events as to in-person meetings. Indeed, in some cases virtual events might be preferable in the sense that digital presentations can be viewed multiple times, if desired, for educational purposes.

By contrast, three other reasons were cited that are generally better-realized through in-person trade shows or conferences. But collectively they were mentioned far less frequently by the respondents:

To see or experience new technology and/or new products: ~9%

Professional networking: ~8%

The ability to engage with experts: 4%

From the vantage point of their experience in 2020, only a small minority of the exhibiting-organizing company respondents in the CEIR survey research reported that they plan to discontinue virtual-event efforts once the pandemic subsides (just 22%).

A much larger percentage – nearly 70% — anticipate that virtual/digital activities will remain (or become) a bigger component of their events going forward — in other words, hybrid events.

That would seem to be the best solution all-around for future trade show success. Offering more digital options within a larger event program will enable people who aren’t able to participate in-person due to schedule conflicts, or simply because of the unease or hassle of traveling, to actually do so.

The experience of 2020’s virtual events also suggest that there are some notable differences in terms of event size and duration — namely, virtual events tend to be smaller in size and shorter in duration than similar in-person events:

The average session length of an in-person education event was 70 minutes, compared to under 60 minutes for a like digital event.

The average number of hours per day for an in-person event was eight, versus just six for a virtual gathering.

Another finding of interest from the CEIR research pertains to which industry segments the exhibition-organizing personnel consider most open to embracing digital event tools. More than four in five respondents felt that virtual offerings in the finance/insurance/real estate segments will become an ever-increasing component of physical events in the future. It was nearly as high – 74% — for events happening in the field of education.

No doubt, we’ll be learning more about the changing dynamics of trade shows over the coming 12- to 24-month period. As we await the “larger perspective” to emerge, what are your thoughts about how your own personal participation in trade shows will change? Will those changes be temporary or permanent? Please share your perspectives with other readers here.

The Coronavirus pandemic has certainly made its mark on many markets and industries – some more than others, of course. But one consequence of the events of 2020 appears to cross all industry lines.

Because of the rapid adjustments organizations have been required to make in the way jobs are performed – borne out of necessity because of health fears, not to mention government edicts – workers have been forced to come up the digital learning curve in a big hurry in order to do their jobs properly.

This “digital upskilling” dynamic isn’t affecting only office workers. It’s happening across the board – in the private and public sector alike.

Simply put, digital upskilling isn’t a matter of choice. If workers want to remain relevant — and to keep their jobs — they’re having to ramp up their digital skill-sets without delay.

Moreover, the new skills aren’t limited to the efficient use of mobile devices, digital meeting/presentation functions, cloud applications and the like. According to LinkedIn’s recruitment data, highly in-demand skills over the past few months encompass wide-ranging and comprehensive knowledge sets such as data science, data storage, and tech support.

Not so long ago, there were “tech jobs” and “non-tech jobs.” Now there are just “jobs” – and nearly every one of them require the people doing them to possess a high comfort level with technology.

Will things revert back to older norms with the anticipated arrival of coronavirus vaccines in 2021? I think the chances of that are “less than zero.” But what are your thoughts? Please share your perspectives with other readers.

What with the inexorable march of technology – which sometimes seems more like a relay race – it’s interesting to speculate on which occupations will be most in demand five years or ten years from now.

That seems pretty reasonable. But what about 20 years on?

Is it even possible to predict which jobs will be most in demand by then – particularly in the tech sphere? Or is that a fool’s errand, destined to elicit howls of laughter should anyone deign to look back at 2020 predictions when 2040 rolls around?

As it happens, the prognosticators at British multinational defense, security and aerospace company BAE Systems are willing to stick their necks out on the topic. They asked their own futurists to tell the what the top jobs in tech might be in 2040.

In broad terms, the answer is that future jobs will be in professions that bridge technology. More significantly, it will be the technology that is the primary job generator, not the profession itself.

But it you really want to bottom-line it, anyone who focuses on artificial intelligence, virtual reality or robotics should be able to future-proof his or her career. At least, that’s the unmistakable takeaway from the jobs that have been earmarked as the “hottest” ones looking ahead 20 years.

And … here they are:

AI Translator – People in these jobs will train other humans as well as their artificial intelligence assistants or robot counterparts, tailoring AI to meet workers’ needs and tune it to acknowledge and correct human errors. Smart-aleck machinery – it’s just what the world’s been waiting for …

Recommended educational background: IT studies, cybersecurity, mechanical engineering

Automation Advisor – As companies become more reliant on automation and robotics, people in these jobs will make sure that the automated workforce is in line with regulations. Compliance officers for machines – why not?

VR Architect – As AI models are used to predict maintenance, people in these jobs will use virtual and augmented reality to monitor components and manage maintenance activities. That’s OK – plant maintenance has always been a responsibility with a lot of downsides …

Recommended educational background: IT studies, graphic design

Human e-Sources Manager – Differing from today’s human resources managers, people in these jobs will analyze data collected from exoskeletons, smart textiles, wearables and the like to perform predictive and preventive maintenance on human workers. Isn’t that nice; sensors will now send alerts to your manager when you’re overworked, overstressed, overweight or otherwise unwell — brilliant!

Systems Farmer – people in these jobs will help companies grow large multifunction parts with nanoscale features, which will sense, process, harvest energy and perform self-repairs. It’s otherwise known as “chemputing” – and it’s likely as unappealing as it sounds.

Recommended educational background: Biology, chemical engineering, chemistry

AI Ethicist – As autonomous systems are assigned more responsibility, people in these positions will make sure AI devices and robots don’t show bias, and will make decisions that best serve the business. I wonder how well that initiative will turn out?

Kidding or snark aside, it is worthwhile to “navel-gaze” along these lines and think of the “what if” scenarios that could very likely paint an employment picture unlike anything we’ve ever contemplated before.

And indeed, BAE Systems fielded research that found that nearly half of people between the ages of 16 and 24 who were surveyed think that they’ll end up having a career in a job that doesn’t even exist yet.

The only problem is – practically no one surveyed had any sort of clue what that future job will be — or how to prepare for it.

What do you think about which jobs will have the most job security in 2040? Does the list above ring true, or are there others that deserve a place on it as well? Please share your thoughts with other readers here.

Debris field from the Ethiopian Airlines plane crash (March 10, 2019).

It’s been exactly two months since the crash of the Ethiopian Airlines 737 Max 8 Boeing plane that killed all 157 passengers and crew on board. But as far as Boeing’s PR response is concerned, it might as well never ever happened.

Of course, sticking one’s corporate head in the sand doesn’t make problems go away — and in the case of Boeing, clearly the markets have been listening.

Since the crash, Boeing stock has lost more than $27 billion in market value — or nearly 15% — from its top value of $446 per share.

The problem is, the Ethiopian incident has laid bare stories of whistle blowers and ongoing maintenance issues regarding Boeing planes. But the company seems content to let these stories just hang out there, suspended in the air.

With no focused corporate response of any real coherence, it’s casting even greater doubt in the minds of the air traveling public about the quality and viability of the 737 planes — and Boeing aircraft in general.

Even if just 20% or 25% of the air traveling public ends up having bigger doubts, that would have (and is having) a big impact on the share price of Boeing stock.

And so the cycle of mistrust and reputational damage continues. What has Boeing actually done in the past few months to reverse the significant market value decline of the company? Whatever the company may or may not be undertaking isn’t having much of an impact on the “narrative” that’s taken shape about Boeing being a company that doesn’t “sweat the small stuff” with proper focus.

For an enterprise of the size and visibility of Boeing, being reactive isn’t a winning PR strategy. Waiting for the next shoe to drop before you develop and launch your response narrative doesn’t cut it, either.

Far from flying below radar, Boeing’s “non-response response” is actually saying something loud and clear. But in its case, “loud and clear” doesn’t seem to be ending up anyplace particularly good for the Boeing brand and the company’s

What are your thoughts about the way Boeing has handled the recent news about its mode 737 aircraft? What do you think could have done better? Please share your thoughts with other readers here.

With artificial intelligence seemingly affecting everything it touches, one might wonder what AI’s impact will be on the employment picture in the years ahead.

Recently, Lee published a column in which he described ten job categories that he feels are “safe” for human workers – regardless of how the AI world may develop around us.

His list is predicated on several fundamental weaknesses Lee sees with AI in handling certain aspects of job performance. Those weaknesses include:

An inability to create, conceptualize or manage complex strategic thinking

Difficulty handling complex work that requires precise hand-eye coordination

An inability to deal with unknown or unstructured spaces

The inability to feel empathy and compassion … and to react accordingly

Kai-Fu Lee

In short, Lee discerns a particular weakness in AI’s ability to perform “humanistic” tasks – ones that are personal, creative and compassionate. Hence, the type of jobs that rely on such qualities will be safer from disruption, he believes.

As for career categories that Lee singles out as generally safe from AI disruption, he cites these ten in particular:

Computer Science – Lee predicts that a substantial portion of computer engineers, IT administrators and technology consultants will continue operate in job functions that aren’t automated by technology.

Criminal Law – The legal profession won’t be adversely affected, considering the persuasive powers that are needed to sway juries with legal arguments. However, some paralegal tasks such as document review will likely migrate to AI applications.

Management – Simply put, there are too many “moving parts” to management – and aspects that require human interaction, values and decision-making – to make it a field that’s amenable to AI. Of course, if a manager is more along the lines of a bureaucrat carrying out set orders, that type of job may be more susceptible to AI disruption.

Medical Care – Lee envisions a symbiotic relationship between humans and AI — the latter of which can help with the analytical and administrative aspects of healthcare but cannot handle most other healthcare responsibilities.

Physical Therapy – Dexterity is a challenge for AI, which makes it unlikely for AI to replace jobs in this field (also including massage therapy).

Psychiatry – Positions in this category, which encompass social work and marriage counseling in addition to strict psychiatry, require keen emotional intelligence which is the domain of humans.

R&D (particularly in AI-related field) – While some entry-level R&D positions will become automated, increased demand for R&D talent will likely outnumber the jobs replaced by AI.

Science – According to Lee, while AI will be of tremendous benefit to scientists in terms of testing hypotheses, it will be an amplification of the discipline rather than taking the place of human creativity in the sciences.

Teaching – While AI will be a valuable tool for teachers and schools, instruction will still be oriented around helping students figure out their interests and providing mentorship – qualities that AI lacks.

Writing – Specifically fiction and other creative writing, because “storytelling” is an aspect of writing that AI has difficulty emulating.

So, there you have it – Kai-Fu-Lee’s fearless predictions about the job categories that will remain safe in an increasingly AI world. Can you think of some other categories? Please share your thoughts and perspectives with other readers.

What differentiates B-to-B companies who carry out successful content marketing initiatives compared to those whose efforts are less impactful?

It isn’t an easy question to answer in a very quantitative way, but the Content Marketing Institute, working in conjunction with MarketingProfs, has reached some conclusions based on a survey it conducted in June and July of 2018 with nearly 800 North American content marketers. (This was the 9th year that the annual survey has been fielded.)

Beginning with a “self-graded” question, respondents were asked to rate the success of their company’s content marketing endeavors. A total of 27% of respondents rated their efforts as either very or extremely successful, compared to 22% who rated their results at the other end of the scale (minimally successful or not successful at all).

The balance of the CMI survey questions focused on this subset of ~380 respondents on both ends of the spectrum, in order to determine how content marketing efforts and results were happening differently between the two groups of marketers.

… And there were some fundamental differences discovered. To begin with, more than 90% of the self-described “successful” group of B-to-B content marketers reported that they prioritize their audience’s informational needs more highly than sales and promotional messaging.

By comparison, just 56% of the other group prioritize in this manner — instead favoring company-focused messaging in greater proportions.

Other disparities determined between the two groups of marketers relate to the extent of activities undertaken in three key analytical areas:

The use of primary research

The use of customer conversations and panels

Database analysis

Also importantly, ~93% of the respondents in the “successful” group described their organization as being “highly committed” to content marketing, compared to just ~35% of the respondents in the second group who feel this way.

Moreover, this disparity extends to self-described skill levels when it comes to implementing content marketing programs. More than nine in ten of the “successful” CMS group of respondents characterize themselves as “sophisticated” or “mature” in terms of their knowledge level.

For the other group of respondents, it’s just one in ten.

Despite these differences in perceived skills, it turns out that content marketing dissemination practices are pretty uniform across both groups of companies. Tactics used by both include sponsored content on social media platforms, search engine marketing, and web banner advertising. It’s in the messaging itself — as well as the analysis of performance — where the biggest differences appear to be.

For more information on findings from the 2018 Content Marketing Survey, click here.

Many full-time workers in the 25-35 age group with college training don’t need reminding that they’re struggling to balance paying for student loans while at the same time attempting to have decent housing and handling their day-to-day expenses.

I’m not in that age group, but our two children are – and I can see from their friends and work colleagues just how much of a challenge it is for many of them to balance these competing necessities.

One way to deal with the challenge is to settle for the sardine-like living arrangements one encounters in quite a few urban areas, with anywhere from three to six people residing in the same (medium-sized) apartment or (small) house.

Somehow, things just didn’t see so difficult for me “back in the day.” Of course, the entirety of my student loans following college amounted to a monthly payment of $31.28, with seven years to pay it off.

First apartment — a $185 per month rental.

And my first apartment – a one-bedroom flat in an elegant 1920’s building, complete with a beautiful lobby and old-fashioned glam elevator, cost me a mere $185 per month.

Not only that, it was only a five-minute bus ride to my downtown banking job.

Now, a newly released analysis published by the American Consumer’s Newsletter helps quantify the different reality for today’s younger workers.

What the data show is that a college degree does continue to provide higher earnings for younger workers compared to those without one.

But … it also reveals that adjusted for inflation, their earnings are lower than their college-educated counterparts in the past.

According to a National Center for Education Statistics analysis as published by the AC Newsletter, here’s a summary of the median earnings differences for male full-time workers in the 25-34 age cohort, comparing 2016 to the year 2000 in inflation-adjusted dollars:

Master’s or higher degree: $71,640 … down 6.4% from 2000

Bachelor’s degree: $56,960 … down 8.8%

Associate’s degree: $43,000 … down 11.8%

Some college, but no degree: $37,980 … down 14.3%

High school degree: $34,750 … down 13.6%

High school dropout: $28,560 … up 2.8%

Thus, among full-time male workers across all education levels, only high school dropouts have experienced a real increase in earnings between 2000 and 2016.

Among female workers, the trends are a little better, but still hardly impressive – and they also start from lower 2000 income levels to begin with:

Master’s or higher degree: $57,690 … down 0.5% from 2000

Bachelor’s degree: $44,990 … down 7.5%

Associate’s degree: $31,870 … down 12.0%

Some college, but no degree: $29,980 … down 13.8%

High school degree: $28,000 … down 7.2%

High school dropout: $21,900 … up 5.0%

What’s even more challenging for workers carrying student loan debt is that those debt levels are higher than ever – often substantially so.

According to a Brookings Institution comparative study, fewer than 5% of students leaving school in 2000 carried more than $50,000 in student loan debt. In inflation-adjusted terms, by 2014, that percentage had risen to ~17%.

Looked at another way, ~40% of borrowers are carrying student loan debt balances exceeding $25,000. It doesn’t take a finance whiz to figure out how big of a hit that is out of a worker’s paycheck.

It makes the some of today’s realities: people living at home longer following college; having frat- or sorority-like living arrangements; putting off plans to purchase a home, or even putting off marriage plans – all the more understandable.

And I’m not exactly sure what the remedy is, either. When it comes to overburdened education debt, it isn’t as if people can go back and rewrite the script very easily.

The COVID-19 pandemic has exposed some interesting fault-lines in the socio-economic fabric of the United States. One of these relates to young adults — those between the ages of 20 and 25. What we find paints a potentially disturbing picture of an economic and employment situation that may not be easily fixable.

The COVID-19 pandemic has exposed some interesting fault-lines in the socio-economic fabric of the United States. One of these relates to young adults — those between the ages of 20 and 25. What we find paints a potentially disturbing picture of an economic and employment situation that may not be easily fixable.