During the Great Recession of 2008-10, it was no surprise to see an increase in private label product sales – not just in food products but also in apparel, cosmetics and other consumer categories.

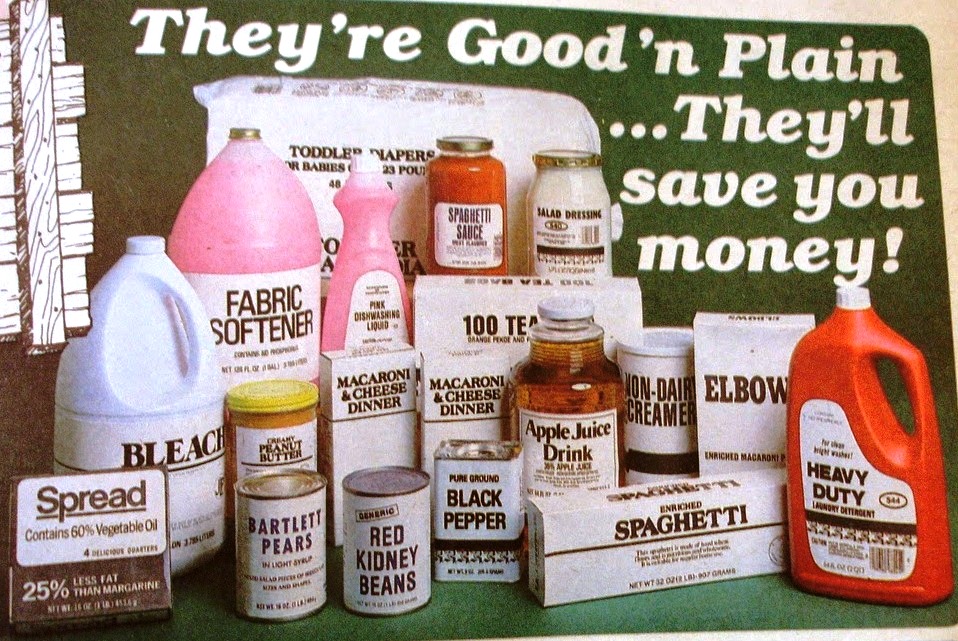

It was much like a similar recessionary time in the United States history — back in the 1970s — when some supermarkets began selling “generic” packaged and canned goods. Those offerings celebrated their generic status by emphasizing their lack of branding – ostensibly to demonstrate that by cutting back on marketing and advertising costs, product pricing to the consumer could be kept lower.

The generic movement didn’t last. When the economic go-go times returned in the mid-1980s, consumers were more than happy to forego the cheaper offerings and go back to their favorite brands.

But the situation is different today. The Great Recession may now be a decade in the rearview mirror, but the private label brands they spawned are going strong. In fact, they’re thriving as never before – and in some ways are eating the legacy brands’ lunch.

Several factors are fundamentally different from before. For one, products that compete on price are no longer being marketed as “generics” but rather as brands in their own right. Brand names like Kirkland, Archer Farms and Essential Everyday look and feel like Kraft, Kellogg’s and other longstanding brands – and for the most part their quality is indistinguishable as well.

Equally important is that fact that there’s no longer any particular stigma associated with shopping “cheap” private label brands. It turns out that consumers in every income category appreciate a bargain; no one wants to feel like they’re being ripped off when there are good quality “best-value” alternatives available.

The usually prescient Warren Buffet appears to have been caught a little off-guard by the changing landscape, recently expressing surprise (and alarm) about this development. His Berkshire Hathaway enterprise took a $3 billion hit in the face of disappointing earnings as Kraft-Heinz share prices dropped more than 25%, thanks to strong competition from the private label alternatives.

Consider these eyebrow-raising statistics: Costco’s Kirkland house brand notched sales of $39 billion in 2018, which is substantially higher than Kraft-Heinz’s total brand sales of $26 billion.

Indeed, the consumer foods industry is witnessing this happening all over the place. Amazon may not be developing its own private brands like Costco or Target have done, but it is working diligently with food and beverage manufacturers to develop private label offerings to sell exclusively on Amazon’s own website.

Looking at the macro environment, the United States is running at historically low unemployment rates today, but that hasn’t stunted the phenomenal growth of discount grocery chains like Aldi and Lidl. Aldi has come from practically nowhere several years ago to threaten becoming America’s 3rd place grocery retailer, behind only Walmart and Kroger. Aldi has done so by pursuing an über-aggressive private label strategy that’s targeting younger, middle-income shoppers in particular.

Note that Aldi is training their sights on more than just budget-conscious consumers, which have traditionally been the narrower audience for private label brands. It turns out that the “stigma” some might have attributed to the “cheap” image of private label foods isn’t there any longer.

For younger consumers especially, such “status” concerns are of no pertinence at all. Whereas the typical grocery cart today contains ~25% private label products, among millennials the proportion is more like one-third.

Based on these trends, it’s little wonder that a recently released Thomas Index Report reports that sourcing activity for private label foods is up more than 150% year over year.

And while the growth of private label products is most pronounced in the food, paper goods and household supplies sectors — and has had the most disruptive consequences there — other sectors like apparel and cosmetics are seeing similar developments.

[Let’s not forget private label pharmaceuticals, too, where price differences are often dramatically lower than just the 15-20% differential we see in the food sector.]

The bottom line is this: Recession or no, cheap has become chic. It’s a trend that’s here to stay. The legacy brands won’t be able to wait this one out and expect better days to come along again.