The efforts to craft a new trade agreement with the People’s Republic of China have run into some pretty major roadblocks in recent weeks and months.

Things came to another inflection point this week when President Trump announced that new tariffs would be imposed on more Chinese goods imported into the United States. As of September 1, pretty much all categories of Chinese imports will now be subject to tariffs.

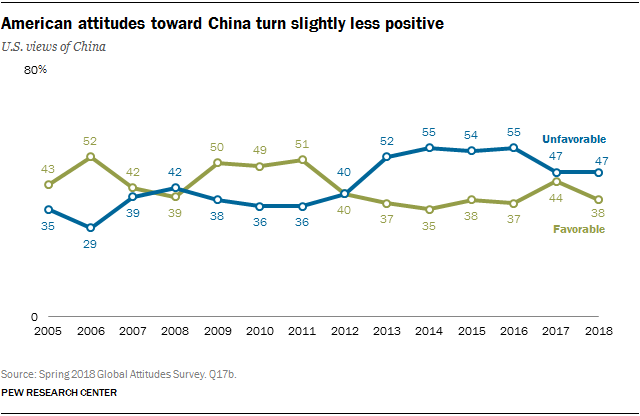

If we look at the impact the protracted impasse has had on markets, the repercussions are plain to see. One result we’ve seen is that China has dipped from making up the largest portion of trade with the United States to being in third place now, behind Mexico and Canada:

But what’s the long-term prognosis for a trade deal with China? Recent world (and USA) statistics point to softening of the economy, which could have negative consequences across the board.

When it comes to perspectives on economic and business matters involving China and the Pacific Rim, I like to check in with my brother, Nelson Nones, who has lived and worked in the Far East for more than 20 years. He has first-hand experience working in the Chinese market and is keenly aware of the issues of intellectual property protection, which is a major bone of contention between the United States and China and is one of the factors in the trade negotiations. (Nelson runs a software company which has chosen to forego the Chinese market because of regulations requiring software firms that set up a joint ventures with Chinese companies to disclose their source code — something his firm will never do.)

I asked Nelson to share his thoughts about what he sees happening in the coming months. Here are his observations:

Chinese President Xi has a lot on his plate right now. It isn’t just the U.S. trade war but also the Hong Kong disturbances, U.S. arms sales to Taiwan, the U.S. sending warships through the Taiwan Strait and the South China Sea, and China’s domestic banking sector weakness, to name just some. Trump has also put President Xi in a tight spot by demanding (or getting) Xi’s assurances that China will buy more U.S. agricultural products and will enact legislation protecting foreign intellectual property.

In spite of his very substantial power, I predict that Xi will have a very tough time ramming Trump’s conditions down the throats of his countrymen.

I should mention that the biggest issue here is intellectual property protection. The draft agreement that China “almost” signed had assurances that IP protection laws will be enacted, but Xi apparently nixed that draft whereupon the Chinese government stated that no government can promise, when negotiating a treaty with a foreign country, to change its domestic laws.

Technically, they’re right. For example, President Trump can’t commit to changing U.S. laws because only the Congress can do that under the constitutional separation of powers. Similarly, on paper, only China’s National People’s Congress (the national legislature) can change Chinese laws, and President Xi is not a member of the National People’s Congress. (Of course, this explanation conveniently overlooks the fact that both the Presidency and the National People’s Congress are subservient to the Communist Party of China, and that Xi is the General Secretary of the Communist Party, but still it’s technically correct.)

In view of all this, the natural Chinese instinct is to wait … and in this case, wait until the 2020 U.S. election and see what happens. If Trump is defeated for re-election, then perhaps many of Xi’s problems will disappear magically. On the other hand, if Trump stays in office maybe the pain that Trump’s China trade policy is inflicting on U.S. businesses and consumers will force Trump to lighten up a bit.

In other words, President Xi has much to gain and relatively little to lose by playing the waiting game for a while.

As for U.S. tariffs, those are causing Chinese businesses to adapt their supply chains by routing them through other East and Southeast Asian countries which are not subject to the tariffs. For instance, instead of sending products straight to the U.S., Chinese manufacturers are sending products to Vietnam or Thailand where a tiny bit of additional work is done – just enough to qualify for a “Made in Vietnam” or “Made in Thailand” label. (This adaptation partially explains Thailand’s large trade surplus which has made the Thai Baht one of the world’s best-performing currencies this year.)

These maneuvers actually provide a safety valve for both Xi and Trump. For Xi, it cushions the reduction in demand for Chinese exports. At the same time it puts some additional pressure on Trump because this type of safety valve does not really exist for U.S. exporters trying to evade reciprocal Chinese tariffs. But on the plus side for Trump, it tends to dampen the impact of higher tariffs pushing up U.S. producer and consumer prices.

If you ask me to bottom-line this, the trade problems look more like a protracted siege than an episode of brinksmanship.

How the siege is resolved depends on how strong Trump’s position will be after the 2020 election. If the Democrats continue with their leftward lurch, then Xi will eventually have to cave because Trump’s position will be strong (I’d say a 65% probability of re-election). But if the Democrats come to their senses and Trump continues shooting himself in the foot, then he’s in real danger of losing the election and Xi will come up the big winner (I’d give this a 35% probability as of today).

So there you have it: the prognosis from someone who is “on the ground” in East Asia. What are your thoughts? Are you in broad agreement or do you see things differently? Please share your observations with other readers here.