One of the many ripple-effects of the COVID-19 pandemic is the effect it’s had on the demand for commercial office space.

In a word, it’s been pretty devastating.

The numbers are stark. According to an estimate published by Dallas-based commercial real estate services and investment firm CBRE Group, Inc., as of the end of 2020, nearly 140 million sq. ft. of office space was available for sublease across America.

That’s a 40% jump from the previous year. Not only that, it’s the highest sublease availability figure since 2003, which means the situation is worse than even during the Great Recession of 2008.

Of course, it isn’t surprising to expect that more sublet space would become available during periods of economic downturn, when many businesses naturally look for ways to cut costs. But those dynamics typically reverse when the economy picks up again. This time around, it’s very possible – even probable – that the changes are permanent.

The reason? Many companies that reduced their office space footprint in 2020 didn’t doing so because they we’re suffering financially. It was because of government-mandated lockdowns. And now they’re expecting many of those employees to continue working from home, either part-time or full-time, after the pandemic subsides.

Employee surveys have shown that many workers prefer to work from home where they can avoid the hassle and expense of daily commuting. It’s understandable that they don’t want that to change back again. In many business sectors which don’t actually need their workforce be onsite to produce revenue, companies are simply ratifying a reality that’s already happened. Accordingly, they’ve changed their expectations about employee attendance at the office going forward.

Commercial landlords are now feeling the long-term effects of this shift in thinking. Rents for prime office space fell an average of 13% across the United States over the past year. In places like New York and San Francisco the drop has been even steeper — as much as a 20% contraction.

For many of the lessees, it’s less onerous to sublease space to others rather than attempt to undertake the messy business of renegotiating long-term lease contracts with landlords. Still, there’s pain involved; sublease space historically comes with a significant discount — around 25% — but with the amount of sublet space that’s been coming onstream, those discounts may well go even deeper due to the lack of demand.

The cumulative effect of these leasing dynamics is to put even more downward pressure on broader rental rates, as the deeply discounted space that’s available to sublet puts more pressure on the price of “regular” office space. It’s a classic downward spiral.

Is there a natural bottom? Most likely, yes. But we haven’t reached it yet, and it’ll be interesting to see when — and at what level — things finally even out. In the meantime, it isn’t a very pretty picture.

What are you witnessing with regards to office space dynamics within your own firm, or other companies in your business community? Please share your thoughts below.

The triumvirate of Amazon, Facebook and Google surge to even bigger dominance in the field.

Fueled by their ability to target audiences by attitudinal and intentional factors in addition to demographic characteristics, the “Big Three” platforms of Facebook, Amazon and Google were already heavy hitters in the advertising realm well-before COVID-19 burst on the scene.

To wit, they accounted for nearly 50% of all advertising expenditures in the United States in 2019.

Then the coronavirus pandemic hit, resulting in changes overnight in how people work and live. Thanks to lockdowns — and with more people than ever glued to digital platforms for everything from business communications to entertainment and online shopping — advertisers found the audience-targeting capabilities of the Big Three platform too irresistible.

So in 2020, even as every other kind of ad spending shrank – including double-digit drops seen in newspaper, TV and billboard advertising – online advertising continued to grow. Even more significantly, the biggest gains in online advertising accrued to the Big Three tech giants rather than to digital media sites and publishers that sell online ads.

When the dust settled, 2020 turned out to be the first year the Big Three swept up more than half of all ad dollars spent in the United States, according to an analysis by ad agency GroupM.

… And in online advertising specifically, the Big Three’s share jumped from an already dominant ~80% in 2019 to nearly 90% in 2020. Ad industry veteran Tim Armstrong (formerly in executive positions at AOL and Google), puts it succinctly:

“[The] companies that are data science-driven get stronger and faster with a tailwind of usage — and COVID was a hurricane.”

The coronavirus environment proved to be fertile ground for the Big Three even in areas previously inhospitable to them — including such categories as store promotions, catalogues and couponing.

As the nation emerges from the COVID environment in the coming months, one wonders if the newly dominant position of the Big Three will retrench in any meaningful way. Speaking personally, I wouldn’t bet money on it. But what are your thoughts?

Likely not in crude oil consumption, but the IEA is now projecting that demand for gasoline will never return to its pre-COVID level.

This past week the International Energy Agency (IEA) issued an intriguing forecast about future of gasoline consumption. If true, it means that the world will have reached its peak demand for gasoline back in 2019, and won’t ever again return to that level.

Of course, with the advent of electric vehicles, the day when gasoline demand would begin to decline was bound to come sooner or later. But the COVID-19 pandemic has hastened the event.

During the widespread restrictions on work and travel imposed by most governments in 2020, daily gasoline demand dropped by more than 10%. Some of that demand is expected to return, but the global shift towards electric vehicles — not to mention continuing improvements in fuel efficiency in conventional gasoline-powered vehicles themselves — means that any growth in demand for gasoline within developing countries will be more than offset by these other forces.

In 2019, only around 7 million electric vehicles were sold worldwide, but that number is expected to grow steadily, reaching 60 million annually just five years from now. Several major car manufacturers have committed to selling electric vehicles exclusively in future years, including Volvo (committed to all-electric vehicle sales by 2030) and GM (by 2035).

As for the demand for crude oil, it is expected to rebound from 2020’s dip to reach as much as 104 million barrels per day by 2026, which would be around 4% higher than the usage that was recorded in 2019. Asian countries – particularly China and India – will be responsible for all of that increase and more, even as some developed nations are expected to see a drop in their demand for crude.

The implications of these forecasts are far-reaching – as are the questions they raise. How well will the legacy car companies perform in comparison to the new all-electric car company upstarts? Can they remake themselves quickly enough to preserve their market position vitality?

What will the effects of lower demand for gasoline – and a lower pace of growth in demand for crude – be on global climate change? Dramatic? … or only minimal?

What do the prospects of lessening demand for crude do to the economies (and politics) of countries like Saudi Arabia, Iran, Venezuela and other key OPEC nations? Will lowered demand lessen geopolitical tensions? … or contribute to even bigger ones?

If you have thoughts or perspectives on these points, please share them in the comment section below.

This past Sunday a major milestone was reached in U.S. air travel. The Transportation Security Administration reported that 1.34 million people passed through checkpoints at U.S. airports on that day.

This was slightly more passengers than the TSA had screened on the comparable Sunday a year ago. But what makes the figure particularly newsworthy is this: It’s the first time that the number of people flying in the United States has eclipsed the year-ago figure since the onset of the coronavirus pandemic in this country.

Even more encouraging, Sunday was the fourth straight day that the TSA had reported more than 1 million people passing through its checkpoints.

The TSA’s seven-day moving average of passenger traffic has now reached its highest level since March 2020, when air travel essentially collapsed in the wake of the spread of COVID-19.

Of course, this doesn’t mean that the amount of air travel is anything near the levels that were typically seen in 2019, the year before the pandemic struck. Indeed, daily traffic is still off by 45% to 55% compared to two years ago.

Ed Bastian

Looking back over the past year, there have been a few occasions where air traffic has edged higher, only to recede again. But those brief upticks were charted during the holidays. This time, the recovery seems real, according to Ed Bastian, the CEO of Delta Air Lines.

Southwest Airlines reports the same dynamics, citing increased leisure trip bookings.

On the other hand, business travel continues to lag — big time. But taken as a whole, the market is looking up. And that’s the best news the U.S. airline industry has had seemingly in eons.

What about you? How have your feelings evolved regarding air travel, and are you making plans for air travel in the coming weeks or months?

Just before the first lockdowns began in April 2020, fewer than 10% of the U.S. labor force worked remotely full-time. But barely a month later, around half of the labor was working remotely. And now, even after the slow easing of workplace restrictions that began to take effect in the summer of 2020, most of the workers who were working remotely have continued to do so.

The longer-term forecast is that perhaps 25% of the labor force will continue to work fully remote, even after life returns to “normal” in the post-COVID era.

For clues as to why the “new normal” will be so different from the “old” one, we can start with worker productivity data. Stanford University economist Nicholas Bloom has studied such productivity trends in the wake of the coronavirus and finds evidence that the productivity boost from remote work could be as high as 2.5%.

Sure, there may be more instances of personal work being done on company time, but counterbalancing that is the decline of commuting time, as well as the end of time-suck distractions that characterized daily life at the office.

As Florida and Ozimek explain further in their WSJ article:

“Major companies … have already announced that employees working from home may continue to do so permanently. They have embraced remote work not only because it saves them money on office space, but because it gives them greater access to talent, since they don’t have to relocate new hires.”

The shift to remote working severs the traditional connection between where people live and where they work. The impact of that change promises to be significant for quite a few cities, towns and regions. For smaller urban areas especially, they can now build their local economies based on remote workers and thus compete more easily against the big-city, high-tech coastal business centers that have dominated the employment landscape for so long.

Whereas metro areas like Boston, San Francisco, Washington DC and New York had become prohibitively expensive from a cost-of-living standpoint, today smaller metro areas such as Austin, Charlotte, Nashville and Denver are able to use their more attractive cost-of-living characteristics to attract newly mobile professionals who wish to keep more of their hard-earned incomes.

For smaller urban areas and regions such as Tulsa, OK, Bozeman, MT, Door County, WI and the Hudson Valley of New York it’s a similar scenario, as they become magnets for newly mobile workers whose work relies on digital tools, not physical location.

Pew Research has found that the number of people moving spiked in the months following the onset of the coronavirus pandemic – who suddenly were relocating at double the pre-pandemic rate. As for the reasons why, more than half of newly remote workers who are looking to relocate say that they would like a significantly less expensive house. The locational choices they have are far more numerous than before, because they can select a place that best meets their own personal or family needs without worrying about how much they can earn in the local business market.

For many cities and regions, economic development initiatives are likely to morph from luring companies with special tax incentives or other financial perks, and more towards luring a workforce through civic services and amenities: better schools, safer streets, and more parks and green spaces.

There’s no question that the “big city” will continue to hold attraction for certain segments of the populace. Younger workers without children will be drawn to the excitement and edginess of urban living without having to regard for things like quality schools. Those with a love for the arts will continue to value the kind of convenient access to museums, theatres and the symphony that only a large city can provide. And sports fanatics will never want to be too far away from attending the games of their favorite teams.

But for families with children, or for people who wish to have a less “city” environment, their options are broader than ever before. Those people will likely be attracted to small cities, high-end suburbs, exurban environments or rural regions that offer attractive amenities including recreation.

Getting the short end of the stick will be older suburbs or other run-of-the-mill localities with little to offer but tract housing – or anything else that’s even remotely “unique.”

They’re interesting future prospects we’re looking at – and on balance probably a good one for the country and our society as it’s enabling us to smooth out some of the stark regional disparities that had developed over the past several decades.

What are your thoughts on these trends? Please share your perspectives with other readers.

How did the pandemic drive consumers to purchase reams and reams of toilet paper?

Just after coronavirus cases started appearing in Europe and North America, two things began to happen. One was restrictions on people’s movements — soon leading to lockdowns nearly everywhere.

The other was a run on toilet paper that seemed to go on for months and months.

While other necessities suffered temporary product shortages as well, toilet paper in particular seemed to be affected the most. And as its disappearance from the store shelves became widely reported, the shortage began to take on near mythic proportions.

Photos of barren shelves were plastered all over the news and shared on social media – even giving the rise to a flourishing resale market in which the price of TP skyrocketed.

It’s little wonder that at the same time, thefts of toilet paper began to be reported across the globe.

Surveys conducted among consumers in North America and Europe found more than a few people admitting that they had begun hoarding toilet paper – more than 17% of North Americans and nearly 14% of Europeans acknowledging so.

Just what is the correlation between a health crisis like COVID-19 and the sudden unavailability of a product like TP, of all things?

It’s the kind of question that no doubt intrigues researchers in the field of consumer behavior. In January, a team of five analysts in Spain published a review of the available research on the topic. Their reporting suggests that several factors were likely at work – some more significant than others. Here is a synopsis of what they reported:

Potential Factor #1: Diarrhea

As coronavirus cases began to rise, more people were experiencing increased gastrointestinal symptoms and diarrhea — either induced by stress or by the COVID-19 itself. However, medical studies suggest that only about 13% of people who contract COVID have significant diarrhea as one of the symptoms or side effects. That 13% is actually a relatively low proportion of COVID patients, and therefore can’t explain much of the global surge in toilet paper purchases. Verdict: Unlikely factor.

Potential Factor #2: Actual Product Shortages

A more likely explanation for the run on toilet paper is that the product was merely one of numerous necessities that consumers went out to purchase in abundance as lockdowns began to take effect around the world. But whereas items like canned foods were able to be more readily restocked, toilet paper wasn’t. In this scenario, supply chains weren’t prepared for the sudden the shift in demand from commercial-quality to residential-quality toilet paper, paper towels and such. As a result, it took longer for production to retool and meet the increased demand. Verdict: Somewhat more likely factor.

Potential Factor #3: Fear — Magnified by the Media

As the news media began to report on empty shelves, toilet paper buying patterns that had initially been in line with those seen for other sought-after goods now reached frenzied proportions. The “FOMO factor” (fear of missing out) increased bulk buying and hoarding behaviors even more.

“Stocking up on toilet paper is … a relatively cheap action, and people like to think that they are ‘doing something’ when they feel at risk.”

The TP buying craze has been seen before. Toilet paper shortages were recorded during the political crisis in Venezuela in 2013 … following the terror attacks on the Twin Towers in New York City 2001 … and even as far back as the 1973 OPEC oil crisis.

I guess the bottom line is this: When the sh*t hits the fan, it’s the toilet paper that wipes out …

Research from Duke University suggests that people who are dressed up buy more and spend more than their casually dressed counterparts.

Ever since the COVID-19 pandemic hit, people have been “dressing down” more than ever. But recent consumer research suggests that for buying more and spending more, retailers do much better when their customers are dressing sharp.

Researchers at Duke University’s Fuqua School of Business analyzed the shopping habits of two different groups of consumers. Smartly dressed shoppers — as in wearing dresses or blazers — put more items in their carts and spent more money compared to casual dressers (as in wearing T-shirts and flip-flops).

The difference among the two groups’ shopping behaviors were significant, too: 18% more items purchased and 6% more money spent by the sharp dressers.

According to Keisha Cutright, a Duke University professor of marketing and a co-author of the report, when people are dressed up they tend to have more social confidence, which in turn reduces the anxiety people may feel about making certain purchasing decisions:

“We focus on how your dress affects your own perceptions. When you’re dressed formally, you believe that people are looking at you more favorably and they believe you are more competent. If you feel competent, you can buy whatever you want without worrying what other people think, or whether they will be judging you negatively.”

Parallel Duke research also found that retailers can actually prompt would-be shoppers to wear nicer outfits when shopping at their stores by featuring nicely dressed models in their advertising. “So, there are some practical implications from the research for retailers,” Cutright says.

How about you? What sort of dynamics are in play regarding how you’re dressed and what you buy as a result? Is there a correlation between what you’re wearing and how you’re shopping? Please share your observations with other readers here.

One of the lessons that the COVID-19 pandemic has taught us is that the advent of an unexpected medical danger can have ripple effects that go well-beyond just the specific health matters at hand.

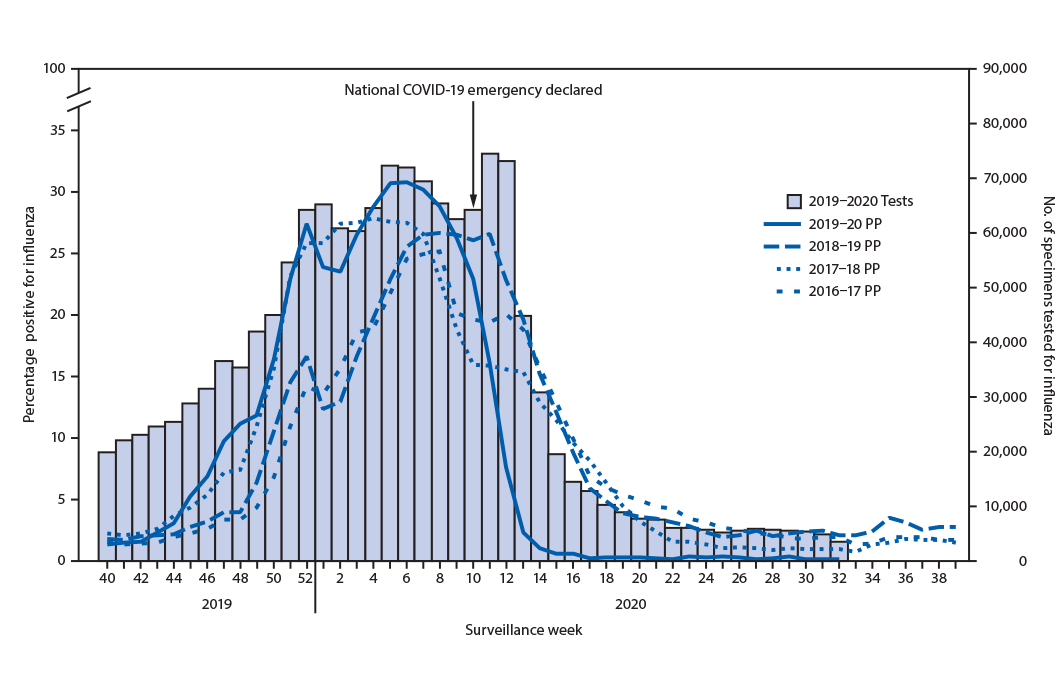

One that has been well-covered in the news is how the precautions most people are taking to avoid contracting the coronavirus are driving flu cases down to levels never before seen. This chart pretty much says it all:But as it turns out, there are some other, perhaps more unanticipated consequences — ones that have positive and negative aspects.

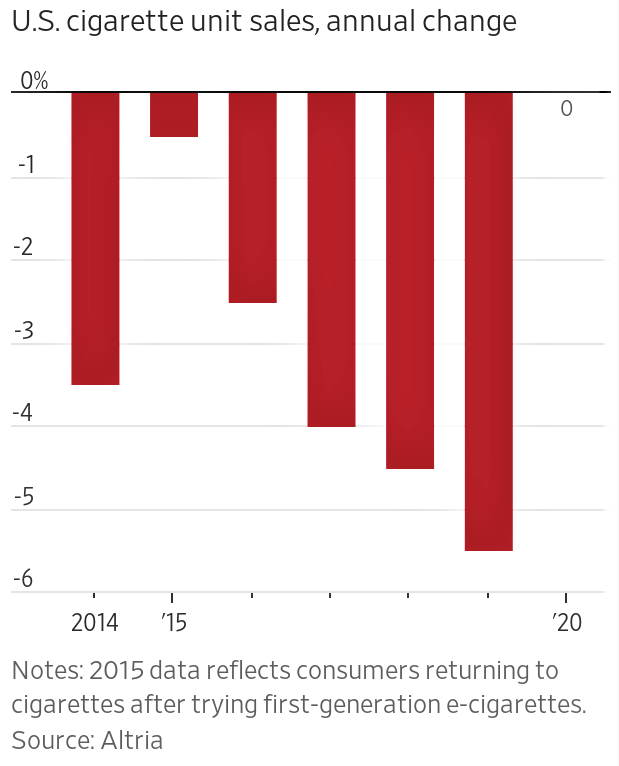

We’re reminded of this in the form of several newly published reports. One report comes from Altria, the largest U.S. producer of tobacco products. According to Altria, the onset of the COVID-19 pandemic appears to be responsible — at least in part — to halting a decades-long steady decline in cigarette usage among Americans.

While the trend hasn’t actually gone in reverse, Altria does report that in 2020, the cigarette industry’s unit sales in the U.S. were flat as compared to 2019.

That’s a big shift from the 5.5% annual decline in usage that was observed between 2018 and 2019.

As for the reasons behind such a sudden shift in consumer behavior, the Altria report touches on several probable factors, including:

People had more opportunities to smoke because of spending more time at home rather than the office.

More disposable income available for smokes because of less money being spent on commuting, travel and entertainment expenses.

The heretofore-robust growth of substitute products (e-cigarettes) was reversed in response to reports about unexplained lung illnesses among e-cigarette users, the ban on flavored vaping products, plus increased taxes on e-cigarette products.

A more acute sense of personal stress and anxiety in the wake of the coronavirus pandemic.

The newest trends in cigarette usage can’t be good for seeing a return to the decline in death rates that are tied to smoking. Unfortunately, those rates remain high: The effects of smoking account for more than 480,000 deaths in the United States each year.

On the other hand, there are positive ripple effects related to the coronavirus pandemic, too. As it turns out, the medical innovations that have been part of the worldwide response to the pandemic are delivering parallel positive benefits in the broader war on cancer.

One piece of evidence is the success of newly developed mRNA vaccines for combating the COVID-19 virus. Those same vaccines are now being repurposed to battle various forms of cancerous tumors.

Naturally, any such development on the cancer treatment front won’t be a quick “silver bullet” solution in the decades-long battle to defeat cancer. But a report released in January 2021 by the American Cancer Society points to the promising success that such new initiatives are having.

The key stats are telling: American cancer death rates have dropped steadily since 1991 – with an overall decrease of ~31% in the death rate through 2018 that was capped by a one-year decline of ~2.5% observed in 2017-18 alone.

The ACS report summarizes:

“An estimated 3.2 million cancer deaths have been averted from 1991 through 2018 due to reductions in smoking, earlier [cancer] detection, and improvements in treatment, which are reflected in long-term declines in mortality for the four leading cancers: lung, breast, colorectal and prostate.”

Not surprisingly, lung cancer is the biggest driver of the death rate decline. Whereas a dozen years ago the overall survival rate for non-small cell lung cancer was just 34%, in 2015 it was 42% (and it’s higher today).

Looking forward, even as we eagerly anticipated the large-scale rollout of COVID-19 vaccinations which can’t come soon enough, we can also be happy in the hope that the emerging science will deliver a parallel positive impact on cancer treatments – so long as we can convince people not to regress in their smoking habits.

What lifestyle adjustments – positive or negative – have you or people you know made over the past year? Beyond the risks of the coronavirus itself, what other new health challenges have you or they faced in its wake? Please share your perspectives with other readers here.

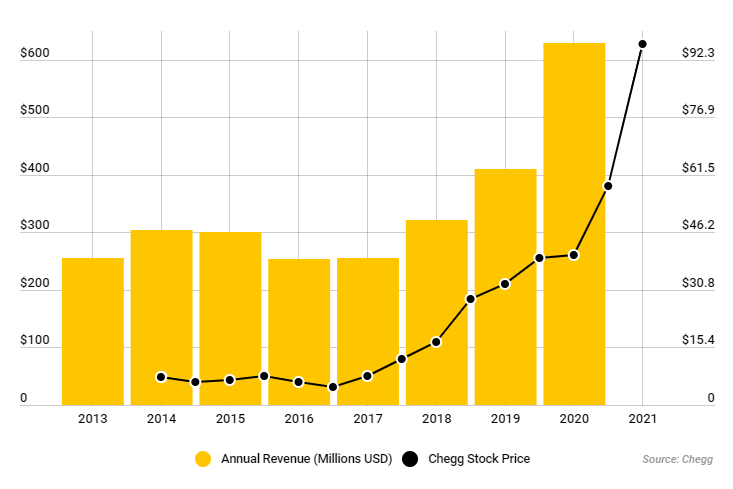

This past week, Forbes magazine published a feature article authored by its senior education editor, Susan Adams, concerning a $12 billion company that’s benefited mightily from the distance learning measures hastily put in place for secondary and college-level students in the wave of the coronavirus pandemic lockdowns.

The company in question is Chegg, an education technology firm which offers a $14.95 monthly subscription that provides a lifeline for students who are looking for answers to exam questions.

Headquartered in California, Chegg actually looks more like a company based in India, where it accesses a stable of more than 70,000 people with advanced science, math, engineering and IT degrees. These freelancers are available online continuously, supplying subscribers from around the world with step-by-step answers to their test-related questions. And the answers are typically provided in a matter of mere minutes.

Reportedly, Chegg’s database contains answers on some 46 million textbook and exam question topics, and it’s the driving force behind the company’s Chegg Study subscription service.

Of course everyone knows where the real action is …

Chegg Study is also the main revenue stream of the company — by far. Other services such as resources for improving writing and math skills as well as bibliography-creation software seem more like window-dressing.

It brings to mind certain video shops of yesteryear which would display a small selection of benign movie “standards” for sale at the front of the premises, fig-leafing the store’s true purpose.

The Forbes article interviewed more than 50 college students who are subscribers to Chegg Study. The students interviewed represent a cross-section of institutions ranging from small state schools to top private universities.

Nearly every one of the students interviewed admitted that they use Chegg Study to cheat on tests.

To view Chegg’s financial numbers is to notice a direct correlation between the onset of the COVID-19 pandemic — when education went virtual practically overnight — and a spike in revenue growth at the company. Quarterly revenues over 2019 have leapt 70% or more, and Chegg’s shares are up nearly 350% since the education lockdowns began in mid-March.

The company is now valued at a cool $12 billion.

Corporate spokespeople deny that Chegg is taking advantage of the current situation to juice its sales and profits. Company president Dan Rosensweig contends that Chegg is the equivalent of an “asynchronous, always-on tutor,” ready to help students with detailed answers to problems.

On-demand education, if you will. Or a student version of the GE Answer Center.

But the “new reality” of virtual education and Chegg’s role within it brings up a number of concerns. As cheating becomes easier to do and hence more prevalent (human nature being what it is), what happens to the value of a high school or college degree? Can degree credentials mean as much as they did before?

It depends. For some jobs where the ability to find accurate information quickly is important, finding someone who mastered the function of “chegging” while as a student might actually be the better candidate for the position. On the other hand, if the position requires a person who will uphold the highest ethical standards at all times, that same candidate would be the wrong one for the job.

Ultimately, it’s the students themselves who will likely be the victims long-term, because if they “skated on through” during their school years and didn’t actually learn the material, that will soon become evident when they go into the workforce. “Find out now … or find out later,” one might say.

Looking at the other side of the coin, how can schools make sure that they’re monitoring and mitigating cheating effectively, such that employers can be confident of the comparative value of a degree from one school versus that of another?

There are a variety of “remote proctoring” surveillance tools like Examity and Honorlock that can lock students’ web browsers and observe them visually through their laptop cameras. While on paper these look like effective (albeit costly) ways to crack down on online cheating, the degree of their actual success is debatable.

Some respondents in the Forbes student interviews reported that they “chegg” their online tests regardless of whether or not they’re being proctored, citing the belief that if they aren’t using the school’s own Wi-Fi connection, it’s impossible to detect the cheating activity.

Furthermore, anecdotal reports from teachers in my home state of Maryland state that on test-taking days, often there are large spikes in the number of students who mysteriously run into “problems” with their Zoom connections – and hence are unable to be observed while taking their tests.

But the issue goes even further – to the very heart of the notion of virtual learning itself and whether distance learning is ill-serving young people. Some students have found it hugely challenging to be skillful learners in the “virtual” world. A business colleague of mine shared one such example with me:

“Someone who I respect greatly and consider to be an honorable man has accepted his son’s cheating, since he went from being an ‘A’-student to failing because he couldn’t handle online learning. He was a visual and auditory learner and without those two things, the information wouldn’t stick.

The student and his dad talked about the 12 consecutive chapters he was supposed to be reading. When the father was satisfied with his son’s understanding of the material, he allowed his son to do whatever was necessary to get through the tests.”

When the situation gets to the point that students’ own parents are going along with the cheating, it means that we have an issue that goes way beyond one particular company that’s taking advantage of the dislocations in the educational arena while laughing all the way to the bank. At its root, the problem is virtual learning and the way it’s being structured.

Of course, the coronavirus crisis built quickly and took many colleges and school systems by surprise — so the fact that jury-rigged ways to deal with the virtual learning have fallen well-short expectations is completely understandable. But the shortcomings have become so glaringly obvious so quickly, new creative thinking is obviously needed – and fast.

If you have thoughts or ideas about steps the educational field could be taking to solve this dilemma, please share them with other readers here.

For those of us in marketing and sales – particularly involved in the commercial market segments – the COVID-19 pandemic brought the function of trade show marketing to a screeching halt, as one event after another in 2020 was either canceled outright or “re-imagined” as a digital-only program.

The impact on the convention business has been severe — and it’s had ripple effects throughout the wider market as well. As Tori Barnes, head of public affairs and policy at the U.S. Travel Association, has noted:

“When a large convention or event is happening, the entire city is involved. Whole downtowns have been revitalized due to the meeting and events business, and they’ve really struggled this past year.”

But now that COVID vaccines have been approved and are beginning to be distributed, the question is, “What’s the road back for trade shows?” Will they return to the “old normal,” or are they forever changed?

Those issues were studied recently by the Center for Exhibition Industry Research (CEIR), which posed a group of questions to ~350 executives of exhibition-organizing companies. The results of the CEIR research suggest that the future of trade shows will likely be a hybrid model of digital and in-person event activities — often as part of the same program.

According to the CEIR findings, “education” was the biggest driver of virtual events run during 2020 – and by a big margin. When asked to cite the most important reason organizers think that professionals attended their virtual events, the top three responses were:

Education for professional or personal development: ~33%

To keep up-to-date with industry trends: ~11%

To fulfill professional certification requirements: ~10%

Collectively representing ~54% of the responses, it would seem that all three of these reasons lend themselves equally well to digital events as to in-person meetings. Indeed, in some cases virtual events might be preferable in the sense that digital presentations can be viewed multiple times, if desired, for educational purposes.

By contrast, three other reasons were cited that are generally better-realized through in-person trade shows or conferences. But collectively they were mentioned far less frequently by the respondents:

To see or experience new technology and/or new products: ~9%

Professional networking: ~8%

The ability to engage with experts: 4%

From the vantage point of their experience in 2020, only a small minority of the exhibiting-organizing company respondents in the CEIR survey research reported that they plan to discontinue virtual-event efforts once the pandemic subsides (just 22%).

A much larger percentage – nearly 70% — anticipate that virtual/digital activities will remain (or become) a bigger component of their events going forward — in other words, hybrid events.

That would seem to be the best solution all-around for future trade show success. Offering more digital options within a larger event program will enable people who aren’t able to participate in-person due to schedule conflicts, or simply because of the unease or hassle of traveling, to actually do so.

The experience of 2020’s virtual events also suggest that there are some notable differences in terms of event size and duration — namely, virtual events tend to be smaller in size and shorter in duration than similar in-person events:

The average session length of an in-person education event was 70 minutes, compared to under 60 minutes for a like digital event.

The average number of hours per day for an in-person event was eight, versus just six for a virtual gathering.

Another finding of interest from the CEIR research pertains to which industry segments the exhibition-organizing personnel consider most open to embracing digital event tools. More than four in five respondents felt that virtual offerings in the finance/insurance/real estate segments will become an ever-increasing component of physical events in the future. It was nearly as high – 74% — for events happening in the field of education.

No doubt, we’ll be learning more about the changing dynamics of trade shows over the coming 12- to 24-month period. As we await the “larger perspective” to emerge, what are your thoughts about how your own personal participation in trade shows will change? Will those changes be temporary or permanent? Please share your perspectives with other readers here.