Millions of Americans age 20 to 24 fall into the NEET category: “Not in Employment, Education or Training.”

The COVID-19 pandemic has exposed some interesting fault-lines in the socio-economic fabric of the United States. One of these relates to young adults — those between the ages of 20 and 25. What we find paints a potentially disturbing picture of an economic and employment situation that may not be easily fixable.

A recently issued economic report published by the Center for Economic and Policy Research (CEPR) focuses on the so-called “NEET rate“– young Americans who are not employed, not in school, and not in training.

As of the First Quarter of 2021, the NEET category represented nearly 4 million Americans between the ages of 20 and 24. This eye-popping statistic goes well beyond the particular circumstances of the pandemic and may turn out to be an economically devastating trend with a myriad of adverse ripple effects related to it.

Look at any business newspaper or website these days and you’ll see reports regularly about worker shortages across many sectors — including unfilled jobs at the lower end of the pay scale which offer employment opportunities that fit well with the capabilities of lower skilled workers newly coming into the workplace.

At this moment, pretty much anyone who is willing to look around can easily find employment, schooling, or training of various kinds. But for millions of Americans in the 20-24 age cohort, the job opportunities appear to be falling on deaf ears. Bloomberg/Quint‘s reaction to the CEPT study certainly hits home:

“Inactive youth is a worrying sign for the future of the [U.S.] economy, as they don’t gain critical job skills to help realize their future earnings potential. Further, high NEET rates may foster environments that are fertile for social unrest.”

… Daily urban strife in Portland, Minneapolis and Seattle, anyone?

It doesn’t much help that younger Americans appear to be less enamored with the basic economic foundations of the country than are their older compatriots. A recent poll by Axios/Momentive has found that while nearly 60% of Americans hold positive views of capitalism, those sentiments are share by a only little more than 40% of those in the 18-24 age category.

Moreover, more than 50% of the younger group view socialism positively compared to only around 40% of all Americans that feel the same way.

The coronavirus pandemic may have laid bare these trends, but it would be foolish to think that the issues weren’t percolating well before the first U.S. businesses began to lock down in March 2020.

And more fundamentally, one could question just how much government can do to reverse the trend; perhaps the best thing to do is to stop “helping” so much … ?

More information about the CEPR report can be viewed here. What are your thoughts on this issue? Please share your views with other readers here.

The first-ever in-flight magazine has now become the latest one to fold. American Airlines debuted its seatback publication back in 1966, establishing a precedent that would soon be followed by all the other U.S.-based passenger airlines as well as many foreign carriers.

The American Way (later shortened to American Way) started out as a slender booklet of fewer than 25 pages that focused on educational and safety information about American Airlines, its equipment and staff. Initially an annual publication, American Way soon became a monthly magazine.

Its early success was due to the captive audience that were airline passengers “back in the day.” Unless you brought your own book or periodicals on board, the in-flight magazine was a welcome way to pass the time in lieu of conversing with your seatmates or simply dozing.

As all other American passenger carriers launched their own in-flight magazines, many of them grew to more than 100 pages in length. In their heyday, it’s very likely that the readership levels of these publications outstripped those of many consumer magazine titles.

But as with so much else that’s happened in publishing, they were destined to become a casualty of changing consumer behaviors. Interest in leafing through in-flight magazines dropped off when travelers started uploading books, movies and TV shows onto their electronic devices – or tapping into the airlines’ own electronic entertainment options. And when that happened, advertiser interest – the lifeblood of any commercial publication – fell off as well.

… and the last issue (June 2021).

American Way’s last issue is this month. Proud to the last, its cover story is about “America’s hippest LGBTQ neighborhoods.” But after June, the magazine will join the in-flight publications that were dropped by Delta and Southwest Airlines during the COVID-19 pandemic and won’t be returning.

To be sure, several of them continue to hang on. United Airlines’ Hemispheres magazine is due back on planes in July, and Virgin Atlantic has plans to relaunch its magazine Vera in September. But these would seem to be in the minority as the other in-flight magazines have disappeared into the ether.

Will they be missed? Travel analyst Henry Harteveldt doesn’t seem to think so, stating recently to USA Today:

“I don’t think frequent travelers – or infrequent travelers – will notice or really care to any great degree if the magazine[s] disappear. Certainly, nobody ever chose an airline because of the in-flight magazine.”

I’m in agreement with Mr. Harteveldt on this. But how about you? Will you be missing in-flight magazines at all?

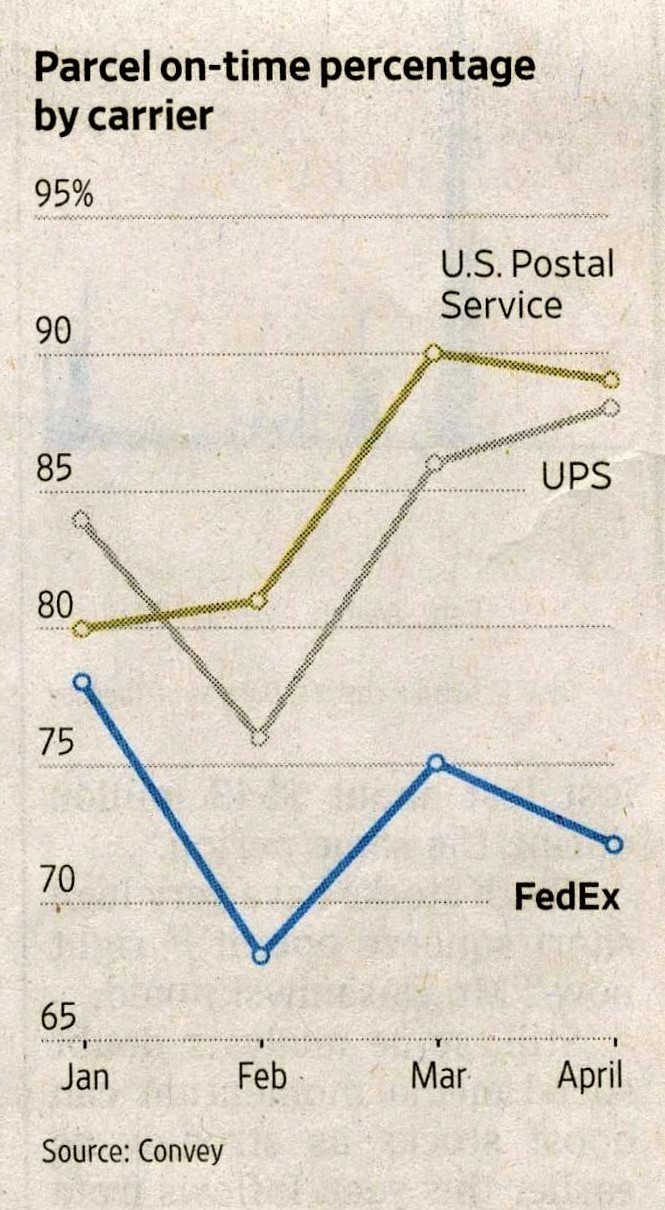

Recently, it’s fallen behind even the USPS in on-time delivery performance.

FedEx’s 2021 YTD delivery performance hasn’t exactly been stellar.

The pandemic-fueled increase of online product ordering hasn’t let up in recent months. And the tale it tells is FedEx struggling to keep up with its rivals when it comes to on-time parcel deliveries.

The most recent statistics covering March through mid-April show a significant difference in delivery performance – 87% on-time deliveries for FedEx Ground shipments compared to 95% in the case of UPS. Those figures come from ShipMatrix, Inc., a company that tracks shipping and delivery performance.

According to The Wall Street Journal, the comparatively weak performance by FedEx elicited this anodyne statement from a company spokesperson:

“FedEx continues to experience a peak-like surge in package volume due to the explosive growth of e-commerce. As always, we are working closely with our customers to manage their volume and identify opportunities to help ensure the best possible service.”

… As if the other delivery companies aren’t facing the same dynamics regarding the growth in online ordering volume.

Delivery tracking software company Convey has released figures that are even more problematic for FedEx. In April, only around 70% of FedEx shipments were on-time, which means the company’s performance was weaker than UPS and even the U.S. Postal Service.

In response, FedEx claims that Convey’s data haven’t aligned with its own internal stats, but the company hasn’t released figures of its own to illustrate the difference.

At the same time, FedEx reports that it’s doubling down on plans to increase its network capacity, along with recruiting additional workers. Even so, it acknowledges that FedEx Ground capacity will continue to be constrained until the end of 2021.

Up to now, the unimpressive record on parcel deliveries hasn’t appeared to hurt FedEx’s financials, which recently hit their highest-ever monthly revenue and operating profit levels. The question is, can that performance hold long-term if businesses and their customers continue to experience slower deliveries? It isn’t as if there aren’t alternative suppliers in the parcel delivery business.

Have you experienced issues with FedEx’s delivery performance recently? If so, are they significant enough to make you open to considering alternative shippers? Please share your thoughts with other readers here.

Responses from two people in particular are worth highlighting for the “countervailing views” that they espouse. I think both have merit.

The first response came from my brother, Nelson Nones, who has lived and worked outside the United States for decades. His perspectives are interesting because, while fully understanding domestic events and policies, he also brings an international orientation to the discussion due to his own personal circumstances. Nelson is looking to history for his perspectives on the inflation issue, offering these comments:

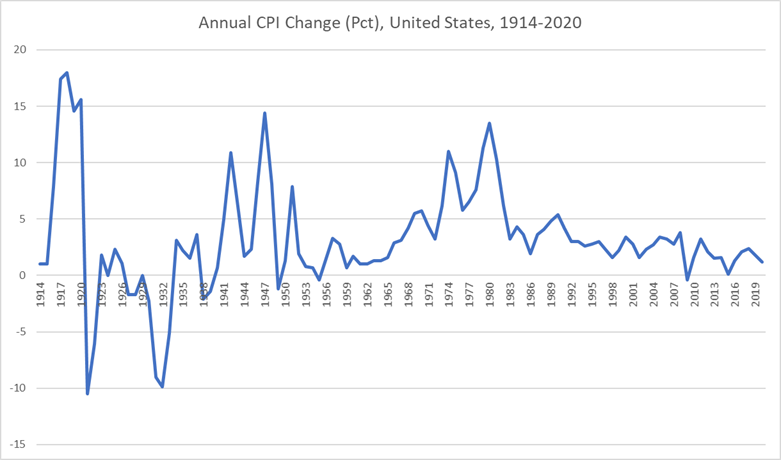

The chart below shows annual U.S. CPI percentage change for the past 106 years:

Projecting the latest (April 2021) Consumer Price Index forward to an entire year suggests that the U.S. will experience a 3.1% inflation rate in 2021. That would be higher than in any year since 2011, which was a bounce-back year following the Great Recession. Otherwise, the generic inflation trend has been consistently down since 1982 (nearly 40 years).

If the historical trends are any guide, and if we are indeed entering a persistent inflationary phase, it would take another decade before inflation growth approaches the levels seen during the 1970s.

But I think the likeliest scenario is experiencing a sharp uptick this year due to pent-up demand following the COVID-19 pandemic that will causie spot shortages, followed by resumption of a downward trend over the following ten years or so.

That’s similar to the pattern you can observe in the chart [above] during the years following the end of World War II, which had also created massive pent-up consumer demand.

Consider that the coronavirus pandemic hasn’t really altered the underlying economic fundamentals. The past 40 years has witnessed an explosion of manufacturing capacity in China and other developing countries, and that hasn’t gone away. Meanwhile, dependency on oil — a key driver of inflation in the 1970s — has shrunk due to improved energy efficiency and aggressive exploitation of renewable energy resources, which for all practical purposes are in infinite supply.

Another factor, which doesn’t get as much attention as it probably should, is declining birth rates and aging of the population on a global scale, leading to a slower rate of population growth in the future that may constrain demand for consumer products in comparison to the past century. Let’s face it — we old farts just don’t consume as much as growing families do!

So yes, we should keep an eye on inflation — but I don’t think we’re in for a repeat performance of the horrible 1970s.

Echoing Nelson’s thoughts are the perspectives of another business veteran — an editor and publisher who has been intimately involved in the commercial/B-to-B field for decades. Here is what he wrote to me:

I don’t want to get into a public debate with the inflationistas because I will never convince them that this is likely not a replay of the 1970s and early 80s inflationary period pre-[Paul] Volcker. (Speaking personally, I didn’t own a house until I was 42 for the very reasons you cited in your blog post, and I was just a lowly editor back then.)

What we’re seeing today is simply the price shock of suddenly soaring demand, aggravated in the case of some commodities such as steel by Trump-era tariffs.

All commodities are tied to the price of crude oil, the most volatile of all commodities, which is long-denominated in U.S. dollars. WTI crude pricing is now at around $63 per bbl. — about where it was in early 2020 before the pandemic hit. It went negative for a time during the worst period of the crash in worldwide demand that was brought about by the pandemic. Tanks couldn’t be found into which to put the excess crude coming out of the ground from U.S. fracking. Traders freaked out, as they sometimes do.

So naturally, the percentage changes today look jaw-dropping. I can go through all the other commodities mentioned in your post and provide simple explanations as to why each is currently on the rise. Logistical bottlenecks are a big problem with everything — but as with oil, most of the issue is the sudden surge in demand as the pandemic winds down even as production and logistics aren’t yet prepared to fulfill the need.

In other words, the situation has very little to do with government spending — especially since most of the infrastructure money isn’t even allocated, let alone spent. Also, the Biden administration has yet to raise a single tax. It can’t. Only the House Ways and Means Committee can initiate tax changes, and those must then go through the Senate to become law. Senate Minority Leader McConnell and his allies have made sure nothing has gotten through.

Of course, it never hurts to keep an eye on things — especially with structural inflation as you noted in your article. But it’s important to look also at other, broader data. The Producer Price Index in April did reflect the increase in commodities prices, but the Consumer Price Index, even though it had a month of robust increases, remains below 3% annualized. And the Personal Consumption Expenditure Price Index, which is what the Fed pays attention to the most, is still tracking under 2% on an annualized basis. (A little inflation can be a good thing, actually.)

On the income side, average wage rates aren’t rising; they’re more likely to be falling in the future as low-wage service workers, including those in foodservice, re-enter the market.

So in my view the things people see with inflation are most likely short-term issues. Let’s look at it again in six months to a year. I’d also suggest that people read economist Paul Krugman’s columns in the New York Times for a bit of perspective that’s counter to the views of the inflationistas, if only for balance. The monetarists have been wrong since Volcker squeezed out the inflationary spiral. It was painful, though — so we’ll want to keep an eye on things.

Considering the views put forward above, I think it’s fair to conclude that “the jury’s out” on whether we’re actually entering a prolonged inflationary period. If you have additional thoughts or perspectives to share on either side of the issue, I’m sure other readers would be interested to hear them. Feel free to leave a comment below.

The rise in lumber prices has received a certain degree of coverage in the news in recent weeks and months. For anyone who used the “pandemic period” to engage in home remodeling or renovation projects – perhaps moving away from “open concept everything” to reintroduce the designated spaces of yesteryear – the eye-popping price of lumber has come as something of a shock.

As for explaining the sharp increase, it’s logical to think that prices are directly correlated to the increased demand for the product. But this explanation is incomplete; the steep price rise in a wide range of commodities well beyond just lumber tells us that inflation isn’t relegated to just a few high-demand product categories. It’s the closest thing to “across the board” that we’ve seen in over 40 years — and the issue seemed to come out of nowhere.

Price inflation has been such a non-factor for so many decades, most consumers don’t even have personal memories of it. But those of us “of a certain age” remember well how difficult it was to navigate an “inflation-everywhere” environment where annual salary increases could never keep pace with rising prices.

It was difficult on people with fixed incomes, of course, but perhaps worse for young consumers who found that struggling to save for a down payment on a house purchase was a losing proposition as the gap widened rather than narrowed year over year. Living like a monk while scrimping and saving for a house gets old when you realize that your efforts aren’t getting you anywhere near where you’re attempting to go …

As for the situation now, the inflation warning signs are all around us if we dare to look. According to a report published in the May 21, 2021 issue of The Wall Street Journal, lumber may exhibit the most visible spike in prices, but consider what futures prices are showing for a whole range of commodities when compared to just one year ago:

Gold: +7%

Platinum: +29%

Wheat: +31%

Cotton: +40%

Coffee: +42%

Sugar: +52%

Silver: +56%

Natural gas: +65%

Soybeans: +81%

Crude oil: +85%

Cooper: +86%

Gasoline: +96%

Corn: +108%

Lumber: +278%

It doesn’t take a degree in economics to know that these sorts of trends are pretty alarming. Whenever it has an opportunity to take hold, inflation is one of the most insidious of economic problems – and one that’s extremely difficult to reverse. Inflation is also very debilitating for the personal budgets of the large majority of consumers, and it causes the most harm to those on the lower rungs of the economic ladder.

The next few months will tell us if this particular inflation is going to be a temporary phenomenon or not. How much of the commodity price increases are attributable to transitory events that will ease as the world’s economies move further from lockdown?

But if this inflation turns out to be something more structural or more directly correlated to the massive increase in government spending paid for by the expanded money supply, expect the economic (and political) climate to begin to look vastly different in the coming months.

Inflation will be uncharted territory for most people. But a few of us veterans will be around to provide context and counsel — and perhaps engage in a bit of “Sister Toldja” commentary while we’re at it …

Quoting Dr. Mark Ritson, is social media “the greatest act of mis-selling in the history of marketing?”

For people who might have wondered if the coronavirus pandemic and the resulting “lockdown culture” that followed would bring more clarity to the debate about the effectiveness of social media, I think it’s safe to conclude that very little has changed in its wake. Many marketing folks continue to suspect that social media may be closer to “all hat, no cattle” than they’d like it to be.

In analyses and evaluations going as far back as a decade, most big companies’ followers on social media have never exceeded 2% to 3% of their brands’ customer base. But the true numbers are even more discouraging, because many brand followers on social media are actually “sleepers” who might have liked a brand in order to participate in a competition, receive a giveaway, or for some other “instant gratification” reason they can’t even recall now.

Mark Ritson

A more realistic metric is how many people choose to interact with a brand on social media. On that basis, the figures nosedive. Mark Ritson, a brand specialist and professor of marketing who has worked at the London Business School and the University of Minnesota, pegs true engagement at around 0.02% of the people who “like” brands.

Other research points to similarly disappointing metrics regarding social media’s impact on purchasing activities. Adobe finds that only about 1% of its social media interactions end up in a purchase, whereas search marketing, direct website traffic and referrals from other websites are the real drivers in terms of the decision to purchase.

So the dynamics haven’t really budged in recent times. At its core, social media channels enable people to communicate with one another, not with brands. For the kind of brand marketing we routinely see happening on social media, it’s little more than an advertising medium offering inventory like any other advertising business. But those aren’t the reasons why people are on social media in the first place – hence the disconnect.

Contrast those dynamics with organic search and paid search marketing, which come into play when people are searching for answers to questions – often about products and what’s available to purchase. In that regard, any investment in search marketing is money better-spent because it helps keep websites aligned with Google search bots’ way of thinking and judging what content gets shown “first and best” on search engine results pages. Marketers can see the results and judge the customer acquisition costs accordingly.

Over in the social media world, it’s true that the biggest brands can show some “success” in their audience engagement, but it’s likely because they have such a huge brand presence to begin with. That simply isn’t the case with vast majority of companies. For them, the road to commercial success likely doesn’t run through Social Mediaville.

What are your own personal experiences with marketing via social media? Has the reality lived up to the promise? Please share your thoughts and observations with other readers here.

As the United States emerges from the COVID crisis, the shape of the American economy is coming into clearer view. Part of that picture is the growing realization that lockdown policies, vaccination rollouts and government stimulus actions have created imbalances in many sectors — imbalances that will time to return to equilibrium.

Everyone knows the business sectors that have been hammered “thanks” to COVID: hospitality and foodservice, travel and tourism, the performing arts, sports and recreation, commercial real estate.

At the same time, other corners of the economy have blossomed — home remodeling, consumer electronics … and the public sector. This last one isn’t a function of any kind of increased demand, but rather pandemic-long guaranteed continuing income to workers on the public payroll.

As we emerge, factories and the building trades are finding it difficult to ramp up their operations to meet growing demand, hampered in part by supply chain issues and shortages of raw materials and parts sourced from offshore suppliers. As of now, most economists believe that such shortages won’t turn out to be long-term problems — but we shall see over time if this is actually the case.

Another imbalance is what’s been happening to the labor force. Government stimulus checks and unemployment benefits have been sufficiently robust so as to depress the number of workers seeking a return to employment in certain sectors — particularly in the service industries. As just one example, restaurants everywhere are finding it more than a little difficult to staff their reopened locations.

The latest forecasts are for the U.S. economy to grow at a blistering pace during the balance of 2021 — perhaps as high as an 8% or 9% seasonally adjusted rate of growth. That would be historic. But not everyone is going to benefit.

In a recent Wall Street Journal article, David Lefkowitz of UBS Global Wealth Management points out that “the very sudden stop to the economy and then the very quick restart has created a lot of havoc — a lot of businesses have gotten caught flat-footed.” But beyond this is the very real likelihood that inflation will emerge as a key factor in the economy, for the first time in more than 40 years.

Viewed holistically, the situation in which we find ourselves is one where many new and unusual “ingredients” have gone into the economy over the past year, resulting in an economic brew that is just as unusual — and perhaps even unique in our history.

An artificially depressed economy due to government fiat … followed by massive economic stimulus paid for by expanding the money supply … coupled with sudden demand propelling certain industries over others due to government-driven dictates: for sure it’s a new mix of factors. Considering this, I’m not at all sure that very many people inside or outside of government have a clear handle on what the next 18 months will actually bring.

But that doesn’t mean we can’t speculate about it, right? In the comment section below, please share your perspectives on what’s in store for the U.S. economy. I’m sure others will be interested in reading your thoughts.

Corporate promotional products and branded swag have been a big part of business for decades. The Advertising Specialty Institute reports that in 2019, promo products expenditures in North America amounted to nearly $26 billion, amazing as that figure might seem.

But that was before the coronavirus pandemic hit, shutting down trade shows and forcing the cancellation of events (or migrating them online). All of a sudden, demand for branded tchotchkes, hats, t-shirts, tote bags and the like pretty much disappeared.

However, just because corporate swag fell off the radar screen in 2020 doesn’t mean that corporate freebies for customers and prospects are a thing of the past. But COVID seems to have changed how some marketers feel about these items — and given them reason to rethink how branded merchandise can do a better job of actually nurturing customer relationships.

Because of this introspection, the days of ubiquitous, unlimited “homogenous” corporate swag may well be numbered — and that wouldn’t be such a bad thing. For those of us who have participated in industry trade shows, corporate events and the like over the years, when you consider how much stuff is given out to people who promptly discard the items because they aren’t something they either needed or wanted to have, coming up with a different approach was bound to fall on fertile ground.

Enter “gifting-as-a-service” firms. Several of these such as Snappy App, Kitchen Stadium and Alyce have sprung up in recent times. They operate under business models that are as simple as they are elegant. Think of them as “choose your own swag” concepts wherein recipients are given the opportunity to pick which items they prefer – and in some cases the size and color, too. Then those items are shipped directly to the recipient’s home or office.

Being given a card to check off their item of choice it may not pack the same impact as being given the item right there on the spot, but it actually makes life easier for everyone. No longer does a trade show attendee have to lug the item around the exhibit floor and back to his or her hotel room — nor pack it for the flight home. The exhibitor doesn’t need to ship swag merchandise to the show – hoping that the quantity shipped isn’t substantially higher or lower than the number of items actually needed.

Such “gifting-as-a-service” programs provide a better experience for recipients, too, because people can select something they actually want from among a selection of items. And for companies, it could actually turn out to be less costly in the end because they wouldn’t need to be pay for gift items that aren’t redeemed.

Such programs are versatile enough to work across all types of activities – including online as well as in-person events. They can also be offered as rewards to loyal customers completely apart from any particular show or event.

One final plus – or at least a hope – is that less swag will end up in the trash before it’s even had the chance to be worn or used. In a world where there’s increasing focus on environmental sustainability, that has to count for something, too.

Nearly everyone dislikes “office politics.” But does day-to-day employee gossip rise to that level? And have we lost something actually beneficial in the wake of remote work limiting our in-person interactions?

Ever since we were children, most of us have been conditioned to regard gossiping as a negative trait that any caring person should avoid doing.

At its core, the definition of the term is “people speaking evaluatively about someone who isn’t there.” But gossip can also relate to talking about rumors and conjecture regarding topics that go beyond just people.

Historically, gossip or the rumor mill in the office often served as a means by which anodyne-sounding corporate announcements would be subjected to a healthy degree of “whispered conversation and conjecture.” Or, as one DC-area employee put it in a recent Wall Street Journal article, ”You hear the surface story, and then you learn what the real story was – and that’s the gossip.”

In the months since mandatory office workplace lockdowns have been imposed, the gossip mill has fallen on hard times. Instead of serendipitous conversations happening in the lunchroom, in hallways or following group meetings, many workers are spending their days with just one person – themselves. Or they might be interfacing via Zoom meetings with the same handful of people from their core work team, where it’s always the same information being recycled among the same group of people.

Even for employees who have returned to working at their corporate offices, hybrid schedules often mean that there are far fewer daily interactions happening with other employees.

On one level, the reduction in gossiping may be reducing workplace “drama” and helping people focus better on their actual work tasks. Although the evidence is murky, productivity studies do appear to show an uptick in employee productivity since the onset of the COVID-19 pandemic.

On the other hand, in a recent survey of ~500 employees and business owners conducted by international legal consulting firm Seyfarth Shaw, the item that respondents missed the most after a year of remote working was “in-person and grown-up workplace conversations.”

For senior leadership, office gossip has been one way to rely on a kind of “early-warning system” about corporate initiatives or directives. In every office there seem to be a few people who have the pulse of the organization – it might be an executive assistant or some other staff support functionary – who other people feel comfortable confiding in and who in turn can communicate “the upshot” to the top brass. While difficult to quantify, that sort of dynamic really counts for something.

Of course, human nature being what it is, office gossip is never going to go away completely. But Skype or Zoom calls feel forced, and typing out thoughts or conjecture on IMs or e-mails is borderline-weird and feels inherently risky.

On balance, do you welcome the decline of face-to-face “gossip conversations” with colleagues — or do you suspect that a useful guerilla communications conduit has been lost? Please share your perspectives with other readers.

It had to happen: New state laws are now classifying robots as humans – specifically when it comes to traffic laws.

With the proliferation of delivery robots in quite a few urban areas, the issue was bound to arise. Car and Driver magazine reports that the state of Pennsylvania now defines delivery robots as “pedestrians” under a newly implemented law.

More specifically, the Pennsylvania legislative measures stipulate that “autonomous delivery robots” can lawfully maneuver on sidewalks, roadways and pathways. They’re allowed to carry cargo loads as heavy as 550 lbs. at speeds up to 25 mph. on roadways. (On pedestrian pathways and sidewalks, their speeds are capped at 12 mph.)

Pennsylvania is just the latest state to pass new laws regulating autonomous driving and flying technologies. Indeed, there are now a dozen states that allow delivery robots access to roads as well as pedestrian pathways.

A gita and its owner out for a stroll.

The new laws raise some interesting questions. Undeniably, delivery robots are a popular option for businesses and logistics companies; in a relatively short period of time their deployment has evolved well-past that of being merely a “novelty factor.” “The sidewalk is the new hot debated space that the aerial drones were maybe three or five years ago,” reports Greg Lynn, CEO of Piaggio Fast Forward, a robotics design firm that offers a suitcase-sized robot called gita that follows its owner around.

But deploying robots onto street- and sidewalk-grids that were mapped out decades ago – when there were no expectations of the sci-fi scenarios of autonomous vehicles – can be quite problematic from a safety standpoint.

Of course, we’ve faced this issue before – and not so very long ago – with the emergence of the Segway “people mover.” Those contraptions have caused more than a few problems (accidents and injuries) in urban centers around the world, leading some European center-cities to effectively ban their use — such as in Budapest and Barcelona.

And in the city of San Francisco – no technology backwater – delivery robots have been prohibited from operating on most city streets. Municipal leaders have cited potential safety concerns. Moreover, the National Association of City Transportation Officials (NACTO) has gone on record stating that robots “should be severely restricted, if not banned outright.”

One thing’s for sure: With the fast-growing phenomenon of delivery robots and other autonomous vehicles, the whole notion of “sharing the road” has taken on an additional dimension.

Do you have any interesting reports to share from what you may have encountered in your own town or region? Please share your observations with other readers.

The COVID-19 pandemic has exposed some interesting fault-lines in the socio-economic fabric of the United States. One of these relates to young adults — those between the ages of 20 and 25. What we find paints a potentially disturbing picture of an economic and employment situation that may not be easily fixable.

The COVID-19 pandemic has exposed some interesting fault-lines in the socio-economic fabric of the United States. One of these relates to young adults — those between the ages of 20 and 25. What we find paints a potentially disturbing picture of an economic and employment situation that may not be easily fixable.