Recently I read a column in MediaPost by contributing writer Ted McConnell (The Block Chain [sic] Gang, 3/8/18) that seemed pretty wide of the mark in terms of some of its (negative) pronouncements about blockchain technology.

Recently I read a column in MediaPost by contributing writer Ted McConnell (The Block Chain [sic] Gang, 3/8/18) that seemed pretty wide of the mark in terms of some of its (negative) pronouncements about blockchain technology.

Not being an expert on the subject, I shared the column with my brother, Nelson Nones, who is a blockchain technology specialist, to get his “read” on the article’s POV.

Nelson cited four key areas where he disagreed with the positions of the column’s author – particularly in the fallacy of conflating blockchain technology – the system of keeping records which are impossible to falsify – with cryptocurrencies (systems for trading assets).

Nelson cited four key areas where he disagreed with the positions of the column’s author – particularly in the fallacy of conflating blockchain technology – the system of keeping records which are impossible to falsify – with cryptocurrencies (systems for trading assets).

But the bigger aspect, Nelson pointed out, is that the MediaPost column reflects a general degree of negativity that has crept into the press recently about blockchain technology and its potential for solving business security challenges. He noted that blockchain technology is in the midst of going through the various stages of Gartner’s well-known “hype cycle” – a model that charts the maturity, adoption and social application of emerging technologies.

Interested in learning more about this larger issue, I asked Nelson to expand on this aspect. Presented below is what he reported back to me. His perspectives are interesting enough, I think, to share with others in the world of business.

Hyperbole All Over Again?

Most folks in the technology world – and many business professionals outside of it – are familiar with the “hype cycle.” It’s a branded, graphic representation of the maturity, adoption and social application of technologies from Gartner, Inc., a leading IT research outfit.

According to Gartner, the hype cycle progresses through five phases, starting with the Technology Trigger:

“A potential technology breakthrough kicks things off. Early proof-of-concept stories and media interest trigger significant publicity. Often no usable products exist and commercial viability is unproven.”

Next comes the Peak of Inflated Expectations, which implies that everyone is jumping on the bandwagon. But Gartner is a bit less sanguine:

“Early publicity produces a number of success stories — often accompanied by scores of failures. Some companies take action; most don’t.”

There follows a precipitous plunge into the Trough of Disillusionment. Gartner says:

“Interest wanes as experiments and implementations fail to deliver. Producers of the technology shake out or fail. Investment continues only if the surviving providers improve their products to the satisfaction of early adopters.”

If the hype cycle is to be believed, the Trough of Disillusionment cannot be avoided; but from a technology provider’s perspective it seems a dreadful place to be.

With nowhere to go but up, emerging technologies begin to climb the Slope of Enlightenment. Gartner explains:

“More instances of how the technology can benefit the enterprise start to crystallize and become more widely understood. Second- and third-generation products appear from technology providers. More enterprises fund pilots; conservative companies remain cautious.”

Finally, we ascend to the Plateau of Productivity. Gartner portrays a state of “nirvana” in which:

“Mainstream adoption starts to take off. Criteria for assessing provider viability are more clearly defined. The technology’s broad market applicability and relevance are clearly paying off. If the technology has more than a niche market, then it will continue to grow.”

Gartner publishes dozens of these “hype cycles,” refreshing them every July or August. They mark the progression of specific technologies along the curve – as well as predicting the number of years to mainstream adoption.

Below is an infographic I’ve created which plots Gartner’s view for cloud computing overlaid by a plot of global public cloud computing revenues during that time, as reported by Forrester Research, another prominent industry observer.

This infographic provides several interesting insights. For starters, cloud computing first appeared on Gartner’s radar in 2008. In hindsight that seems a little late — especially considering that Salesforce.com launched its first product all the way back in 2000. Amazon Web Services (AWS) first launched in 2002 and re-launched in 2006.

Perhaps Gartner was paying more attention to Microsoft, which announced Azure in 2008 but didn’t release it until 2010. Microsoft, Amazon, IBM and Salesforce are the top four providers today, holding ~57% of the public cloud computing market between them.

Cloud computing hit the peak of Gartner’s hype cycle just one year later, in 2009, but it lingered at or near the Peak of Inflated Expectations for three full years. All the while, Gartner was predicting mainstream adoption within 2 to 5 years. Indeed, they have made the same prediction for ten years in a row (although I would argue that cloud computing has already gained mainstream market adoption).

It also turns out that the Trough of Disillusionment isn’t quite the valley of despair that Gartner would have us believe. In fact, global public cloud revenues grew from $26 billion during 2011 to $114 billion during 2016 — roughly half the 64% compound annual growth rate (CAGR) during the Peak of Inflated Expectations, but a respectable 35% CAGR nonetheless.

Indeed, there’s no evidence here of waning market interest – nor did an industry shakeout occur. With the exception of IBM, the leading producers in 2008 remain the leading producers today.

All in all, it seems the hype curve significantly lagged the revenue curve during the plunge into the Trough of Disillusionment.

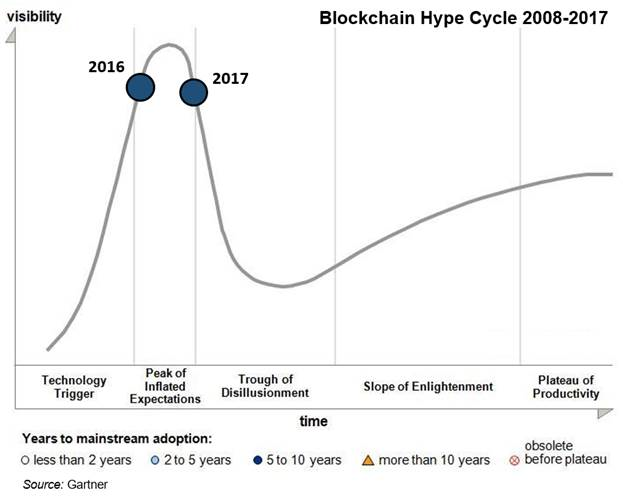

… Which brings us to blockchain technology. Just last month (February 2018), Gartner Analyst John Lovelock stated, “We are in the first phase of blockchain use, what I call the ‘irrational exuberance’ phase.” The chart below illustrates shows how Gartner sees the “lay of the land” currently:

This suggests that blockchain is at the Peak of Inflated Expectations, though it appeared ready to jump off a cliff into the Trough of Disillusionment in Gartner’s 2017 report for emerging technologies. (It wasn’t anywhere on Gartner’s radar before 2016.)

Notably, cryptocurrencies first appeared in 2014, just past the peak of the cycle, even though the first Bitcoin network was established in 2009. Blockchain is the distributed ledger which underpins cryptocurrencies and was invented at the same time.

It’s also interesting that Gartner doesn’t foresee mainstream adoption of blockchain for another 5 to 10 years. Lovelock reiterated that point in February, reporting that “Gartner does not expect large returns on blockchain until 2025.”

All the same, blockchain seems to be progressing through the curve at three times the pace of cloud computing. If cloud computing’s history is any guide, blockchain provider revenues are poised to outperform the hype curve and multiply into some truly serious money during the next five years.

It’s reasonable to think that blockchain has been passing through a phase of “irrational exuberance” lately, but it’s equally reasonable to believe that industry experts are overly cautious and a bit late to the table.

________________________

So that’s one specialist’s view. What are your thoughts on where we are with blockchain technology? Please share your perspectives with other readers here.