When it comes to online retailing in the United States, Amazon’s been cleaning up for years. And now we have new data from comScore that reveals that Amazon is as dominant online today as it’s ever been.

This chart illustrates it well:

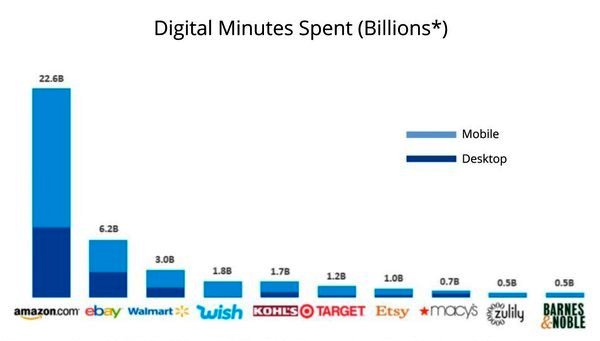

The chart shows that when comparing actual time spent by Americans at each of the Top 10 online retailers, Amazon attracts more viewing time than the other nine entities combined.

Even when considering only mobile minutes, where so much of the growth is happening for digital retailers, Amazon’s mobile viewing time exceeds the combined total digital traffic across eBay, Walmart, Wish, Kohl’s and Etsy.

Pertaining to the mobile sphere, there is an interesting twist that comScore has found in consumer behavior. It turns out, there’s a considerable disparity between the amount of time spent with mobile compared to its share of dollars spent – to the tune of a 40% gap:

In essence, the data show that whereas mobile represents nearly two-thirds of the time spent with online retail, it accounts for only one-fourth of the dollars spent on goods and services.

But this difference is easy to explain: As the largest player in the field, Amazon fulfills a role similar to what Expedia or Trivago do in the travel industry.

Amazon gives consumers a way to scan the marketplace not only for product details but also for prevailing prices, giving them a sense of the expected price ranges for products or services — even if they ultimately choose to purchase elsewhere.