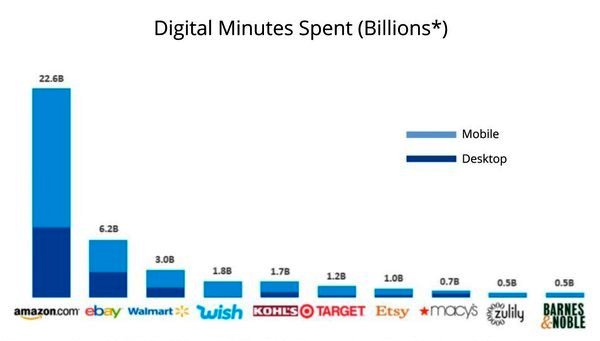

In the era of e-commerce, year after year the growth and financial success of Amazon continues to be noteworthy — seemingly impervious to economic downturns or volatility.

In the era of e-commerce, year after year the growth and financial success of Amazon continues to be noteworthy — seemingly impervious to economic downturns or volatility.

What’s the secret sauce?

The answer is interesting. It isn’t that Amazon dominates any particular product category. Rather, it’s the kind of product — “utilitarian” — that cuts across many categories.

Utilitarian products tend to be practical, generally inexpensive or downright cheap … and typically carry little risk associated with making a regretful purchase choice. They aren’t the type of products that inspire brand affinity, and they typically don’t require very much in the way of pre-purchase research on the part of buyers.

Moreover, on Amazon these utilitarian products have an equally utilitarian path to purchase. Purchase “journeys” — such as they are — are straightforward. Often they begin and end on Amazon’s site, with few or no deviations to conduct research or compare brands.

This is where Amazon excels — in nudging shoppers down the sales funnel while giving them no reason to go away from the website. Amazon makes the purchase steps quick, effortless and satisfying — and probably easier to complete than anyplace else online. If there is a more elegant purchase procedure out there in cyberspace, I have yet to find it.

And if some shoppers might wish to do a little more product evaluation, Amazon makes that possible as well, with consumer reviews offered right on the site for quick and easy evaluation and validation.

Of course, there are certainly product categories that aren’t particularly “utilitarian” in nature, and this is where Amazon’s model is a little less effective. A category such as women’s apparel is more brand-specific and brand-driven, and the purchase journeys in that realm are typically more longer, more circuitous, and more discovery-focused.

But Amazon has effectively carved out a niche in so-called “basic” products to the degree that it has become the “go-to” destination for thousands of products that are “common” in every sense of the word — resulting in some very uncommon business and financial results for the company.