In the United States it seems hardly news that poultry is the most-consumed protein. In recent years poultry consumption in America has grown while beef consumption has stagnated, weighed down by high prices at the consumer level.

At the same time, the National Pork Board committed an unforced error earlier in this decade when it abandoned its longstanding (and doubtless highly effective) tagline “The Other White Meat” in favor of the mealy-mouthed platitude “Pork: Be inspired” – a slogan that convinces no one of anything.

Persistent reports from the medical community that red meat is less healthy than consuming poultry and fish products haven’t helped, either.

But poultry’s prominence in the American market hasn’t necessarily extended to many parts of the rest of the world. But that’s now changing.

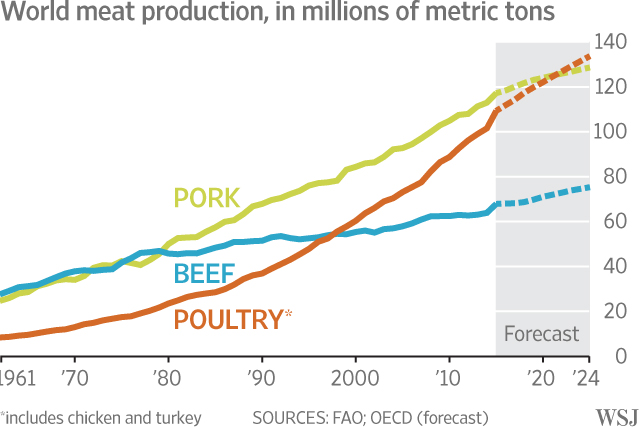

In fact, according to reporting from a recently-concluded International Poultry Council meeting in the Netherlands, poultry is poised to become the most consumed meat protein in 2019.

In fact, according to reporting from a recently-concluded International Poultry Council meeting in the Netherlands, poultry is poised to become the most consumed meat protein in 2019.

The precipitating factor is African swine fever, which is now affecting pig herds in 15 countries on three continents. Pork production losses this year are expected to represent ~14% of the world’s pork supply – and that’s just the minimum forecast; the losses could go higher.

Interestingly, African swine fever’s most significant initial outbreaks were in Russia and Eastern Europe, but now East Asia is being affected most significantly. The first cases were found in China beginning in August 2018 but now have spread rapidly throughout the country. For a country that is responsible for nearly half of the world’s supply of pigs, that’s a very big deal.

The swine fever is spreading to the nearby country of Viet Nam as well – which is the world’s fifth largest producer of pork.

The problem for pig growers is that African swine fever is the quintessential death sentence: The disease has a 100% mortality rate, and no vaccine has been developed to guard against its spread.

According to global food and agriculture financing firm Rabobank, China is expected to experience a ~30% drop in pork supplies this year, which in turn will mean a decline in total world protein supplies. The twin results of these development: an increase in prices for all proteins … and poultry will overtake pork this year as the world’s most consumed protein.

Until such time when an effective vaccine against African swine fever is developed, we can expect that production of other proteins like poultry, eggs, beef and seafood will rise. So, it seems as though poultry’s presence as the world’s most-consumed protein will likely endure. Poultry’s position as the protein leader may have stemmed from a different impetus in the United States than in the rest of the world, but everyone has ended up in the same place.